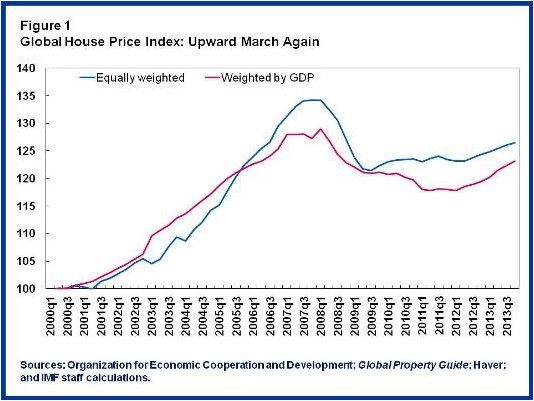

The International Monetary Fund (IMF) last night published a blog post warning of the reemergence of frothiness in the world’s housing markets, where values are once again rising at an accelerating rate (see next chart).

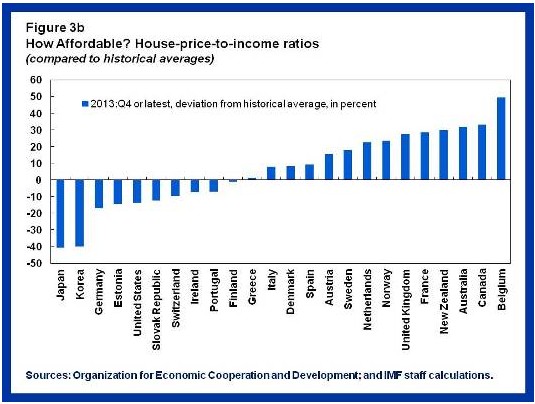

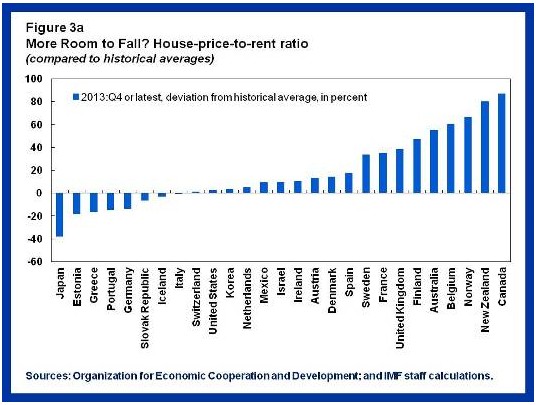

According to the IMF, “33 out of 52 countries in our Global House Price Index showed increases in house prices” last year, with values in “Australia, Belgium, Canada, Norway and Sweden” looking quite stretched when compared against both incomes and rents (see below charts).

As you can see above, Australia is ranked as having the third most expensive housing market in the developed world when measured against incomes and the fifth most expensive market when gauged against rents.

The IMF urges prudential regulators and central banks to adopt macro-prudential tools to mitigate banking sector risks:

…we also need macroprudential policies aimed at increasing the resilience of the system as a whole. The main macroprudential tools used to contain housing booms are limits on loan-to-value (LTV) ratios and debt-to-income (DTI) ratios and sectoral capital requirements…

Another macroprudential tool is to impose stricter capital requirements on loans to a specific sector such as real estate. This forces banks to hold more capital against these loans, discouraging heavy exposure to the sector.

It also fires a direct shot across the bow of regulators, like APRA and the RBA, who have shown an unwillingness to adopt such tools, calling for an end to their “benign neglect”:

The tools for containing housing booms are still being developed. The evidence on their effectiveness is only just starting to accumulate. The interactions of various policy tools can be complex. But all this should not be an excuse for inaction. The interlocking use of multiple tools might overcome the shortcomings of any single policy tool. We need to move from “benign neglect” to an “all of the above” approach when it comes to policy choices.

Couldn’t have said it better myself. But are APRA and the RBA listening?

unconventionaleconomist@hotmail.com