The two companies most responsible for the plunging iron ore price, FMG and RIO, have today launched a two-pronged assault on increasingly bearish investors. FMG’s chief financial officer, Stephen Pearce, is out claiming $110 is the new price floor, from The Australian:

…“What we’ve seen over the last six months, since September last year, is a lot of new supply come in from Rio, BHP and ourselves in particular…Infrastructure tends to come on in lumps and therefore you get supply flushed into the market in step changes and I think we’ve seen that in the last six months…I think it will take another month or two for the market to digest that and for the market to respond.

“But I think we’re perhaps already seeing early signs of that in the marketplace as we’ve just gradually crept off that $US90 level and potentially seeing some early drawdowns of stock at the ports, maybe subtly indicating we’re just stepping off that bottom.”

Possible but not the base case (see my morning post).

And on China:

“I think people sometimes look at short-term statistics from China and I think that’s a little bit dangerous…In my mind, (it’s) the six-month and 12-month trends that are really more important…When you step back and look at those, steel usage is up 6 per cent year-on-year, and that’s pretty healthy…In my view, we may well see the same sort of trend we saw last year, when there was a higher level of fixed-asset investment and steel utilisation in China in the second half of the calendar year than there was in the first.

Plain wrong on that one. From China’s NDRC, the most authoritative source on Chinese steel production in the world, for the January to May period output was 342 million tonnes (mt), 2.7% year on year. That’s 5.3% lower growth than the same period last year. Exports of steel are flying at 34mt, up 34%year on year. If you subtract the growth in exports, Chinese steel production has fallen year on year by somewhere around 1%. Moreover, any long term view, which one should take on FMG, would be 3-5 years, over which period the odds favour further slowing in Chinese growth and further shifting away from investment as the driver of growth.

Also, because H2 last year was unseasonably strong, it will very difficult to generate growth year over year in 2014. If H1’s 2.7% can be sustained it will be a triumph. Infrastructure will help, certainly, but it’s residential housing that’s the issue. There is no sign of a rebound there yet and without it FMG’s hope is forlorn.

On current prices, FMG reckons:

“I sleep very well at night,” Mr Pearce said. “Our cost position is 34 per cent down on where it was in 2012.

“We are now producing tonnes on to the ship at $US33-$US34 a tonne — that’s very different from where we were at $US50 a tonne two years ago.

“We generate very healthy margins at these … pricings.”

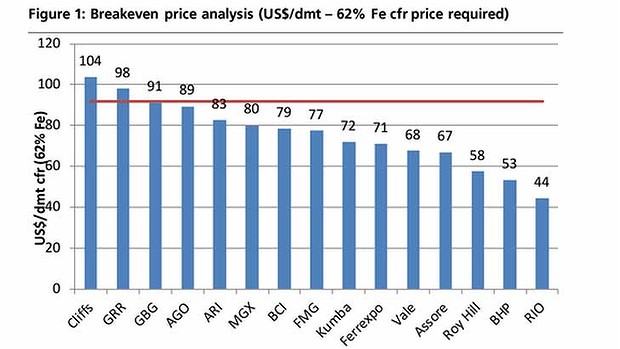

Judge for yourself if that’s true. And to be safe, assume prices go to $80 in the next 18 months, from UBS:

Over to RIO Tinto’s chief financial officer Chris Lynch. Also from The Australian:

The Broken Hill-raised Mr Lynch ruled out any prospect of Rio making an acquisition purely to rebalance the portfolio: “Any investment we make will always be based on value. If there happened to be a diversification benefit from it, then that’s great. But we’ll never target diversification as a primary objective.’’

…“If you go to China and you see what’s happening on the ground, you come away with a totally different perspective,” he said. “It’s all still happening.”

Do only the big miners travel to China? I’ve been several times. I’ve seen the forest of cranes, the endless construction pits, and the greatest dust cloud in history. What I see is an extraordinary one-off and catch-up building boom that is past its zenith.