Fortescue double downgrade: Morgan Stanley

by Chris Becker

From the bear fangs of Morgan Stanley comes a turnaround in the fortunes of Fortescue Metals (FMG):

We no longer project cash accumulation, debt reduction and increased dividends. This is the result of a sharp shift in the MS house view on iron ore prices. In fact, additional debt restructuring is required under our new outlook. We move to UW (underweight).

Oh dear.

Here is that change:

The seaborne iron ore market is moving from a pricing structure influenced by high-cost Chinese production to one dominated by market saturation.

The combination of a faster-than-expected supply surplus and greater insight into the Chinese supply structure prompted us to downgrade our price deck.

Our previous, more positive stance was predicated on two key conclusions: 1) the inevitable market surplus was further away then the market expected; and 2) prices would quickly rebound after dipping below levels of mining cost support.

However, the price decline since the end of 1Q has surprised us, particularly given firm demand from China. A deep dive into the roots of the current bout of price weakness and the availability of new cost data prompted us to change our view and price outlook.

It has surprised many.

The report goes on to explain why the market has changed this time around:

In past periods of weakness, prices quickly rebounded after dropping below marginal mining costs. This is because market participants

believed Chinese domestic iron ore operations would shut, forcing steel mills to increase imports.During these previous phases, the global seaborne market balance was already tight, meaning more imports would quickly send the market into deficit, provoking prices to rally.

However, two factors have prompted us to revise our prior conclusions:

1) faster-than-anticipated market saturation on the back of seaborne supply growth and stubbornly high inventory levels; and

2) with access to new cost data of the full Chinese domestic industry, we now believe lower prices will cause some output to shut, lowering mining cost support and thus prices.

Supply supply supply.

The specific case for FMG after these downgrades is stark: while BHP and RIO can obviously take on a lower iron ore price, FMG is literally more leveraged to it:

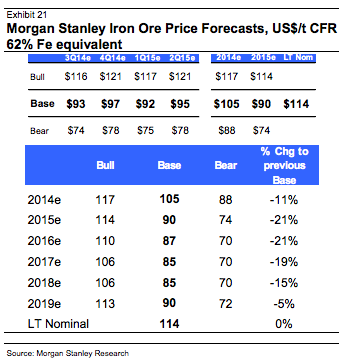

Price deck view swings on shift to oversupply. Our Commodities Team has revised the iron ore index price down by 5-21% to recognise the structural shift to market saturation.

The below-consensus price deck drags our TP and FY15/16 EPS forecasts (-53%/-65%) to the low end of the consensus range.

Focus returns to fiscal leverage for Fortescue. The new price deck compresses its margin to ~US$10/t after all cost obligations

Fortescue remains operationally viable but does not accumulate enough cash to meet future debt repayments; further debt

restructuring is required, in our view.

Alongside FMG, Atlas Iron (AGO) got re-rating with a target of $0.63 (closed at $0.64 yesterday) and although “cash-flow positive” will still make a loss for years to come.

FMG has gapped down on the open nearly 3% nearing support at $4.40 – a normal day of volatility for FMG, but this could get ugly.

Disclosure: I’m neither short or long iron ore stocks whilst blogging here at MacroBusiness.