by Chris Becker

The currency wars continue! Ever since the GFC, a host of other acronyms has entered the lexicon as global central banks put up various parts of a “Wall” to stave off the White Walkers of deflation.

This week ECB President Mario Draghi announced some more along with the tried and true method of cutting interest rates – now at 0.15% – plus a cut in marginal lending rates and for the first time ever, negative deposit rates!

Alongside these stimulus measures will also be a new series of TLTROs, or as a note from Citi explains:

The ECB announced it will conduct a series of targeted longer-term refinancing operations (TLTROs) to mature in Sep-2018. The initial two TLTROs (Sep-14 & Dec-14) will allow counterparties to borrow up to 7% of the total amount of their loans to the euro area non-financial private sector, excluding household mortgages, outstanding on 30-Apr-14.

The ECB estimates the combined initial take-up to be €400bn.

In the subsequent six TLTROs, to be conducted quarterly from Mar-15 to Jun-16, banks will be able to borrow additional amounts within a limit of 3x each counterparties’ net lending (new loans minus redemptions) in excess of the benchmark recorded in the 12-month period up to 30 April 2014.

The cost of the TLTRO will be fixed at the refi rate prevailing at the time of take-up, plus a fixed spread of 10bp (ie 25bp). An early repayment schedule is provided after 24 months, at a 6-month frequency.

The note goes on further to state “its not clear whether funds obtained through the TLTRO will allow banks to buy sovereign debt” although Draghi said as much in the post-rates decision Q&A. Wait and see.

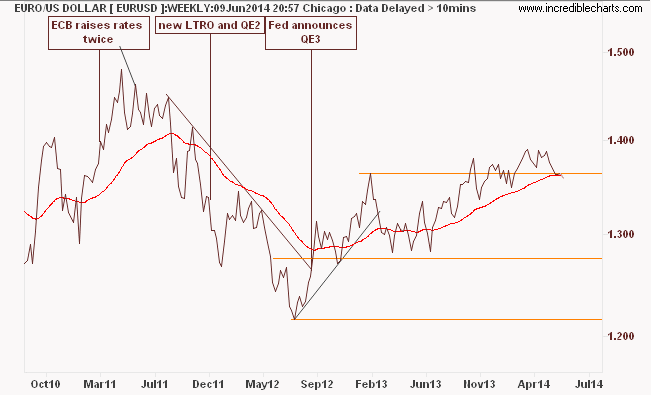

What does all this mean for the Euro? At the last LTRO from late 2011 through early 2012, the currency was in a freefall against the USD hitting 1.20 – nearer its real value – until a new round of QE by the Fed in August 2012 saw the bloc currency appreciate immensely (as USD crumbled) to near its current levels:

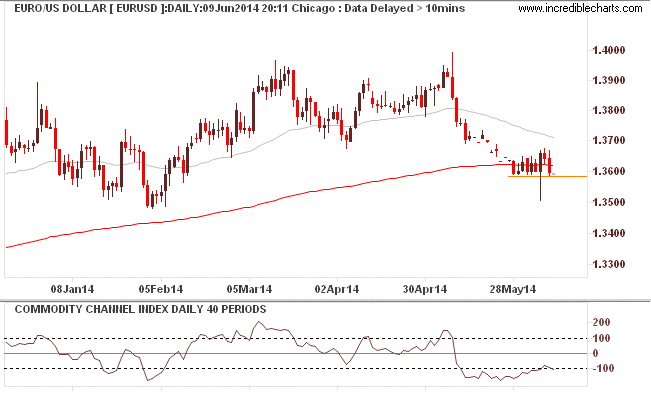

In recent weeks, the Euro has decelerated and overbought condition with a price decline from near 1.40 at the end of April, to just below 1.36, remaining under pressure with support at the 1.3580 level:

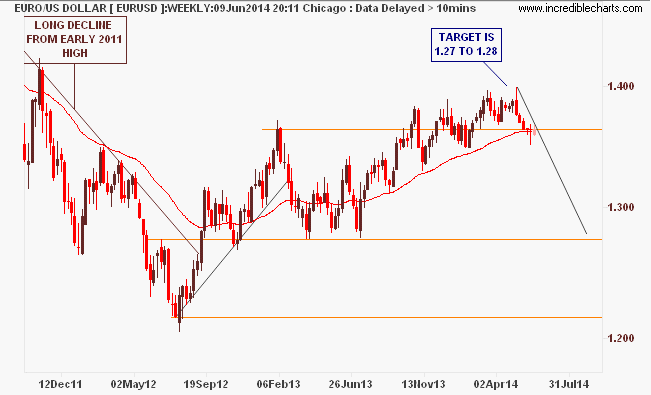

This is not oversold (momentum only at -100) and has the potential to rollover again given any catalyst. Indeed, the weekly chart suggests a rollover is already occurring with a distinct lack of upside momentum, with daylight below to the 1.28 handle:

Are speculators positioning themselves for the inevitable reversal in the Euro? Are the lower rates and negative deposit rates alongside the new TLTRO going to do it? A weaker currency is what all nations – apart from Australia apparently – want to juice domestic demand, but maybe the weapons of war are losing their edge, or is the ECB delaying the inevitable?

A final note from Citi:

We still expect the ECB to launch a fully-fledged QE, possibly in Dec-14.

That’ll do it.