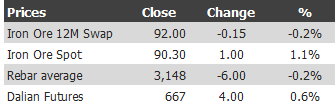

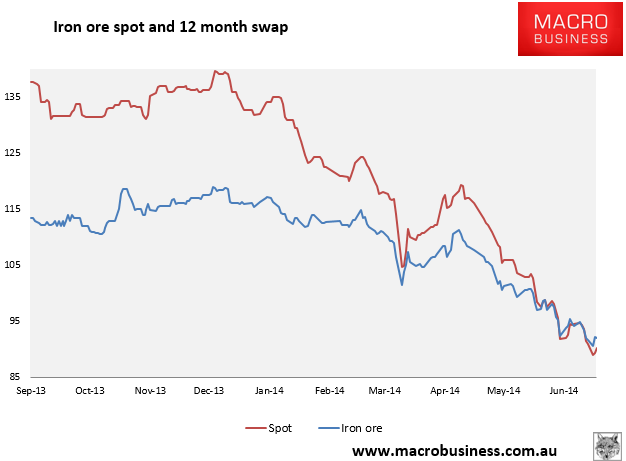

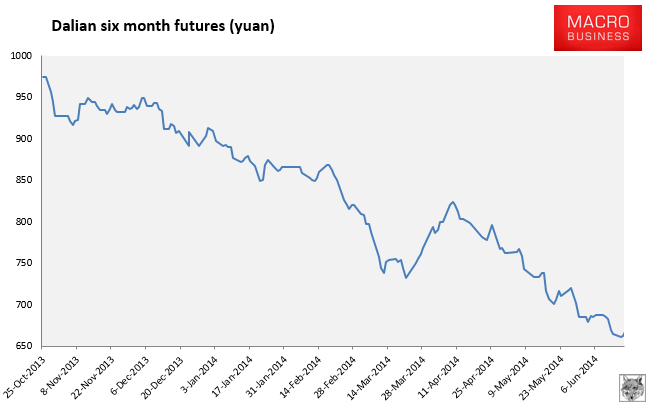

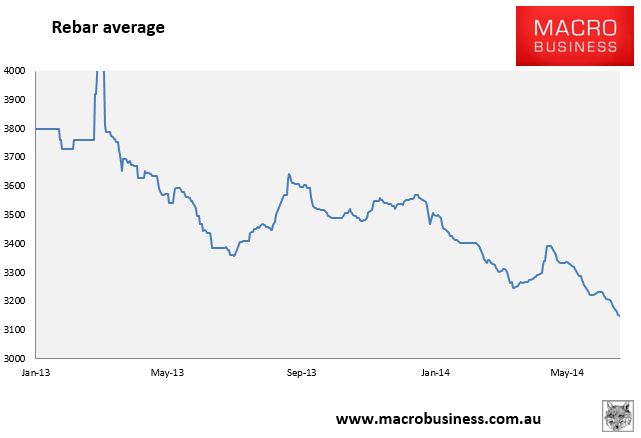

Here are the iron ore charts for June 18, 2014:

Better action again yesterday. Paper markets are going sideways, really. Physical is firmer with the Baltic Dry capesize component up 5%.

Also better news was a rise in Chinese steel output in early June with CISA’s crude steel output averaging 2.1563 million tonnes during the first 10 days of June, up 0.1% from late May. Cisa members reported a daily output of 1.7318 million tonnes in early June, up 1.3% from the preceding 10 days. Non-CISA output fell.

But there’ still no bottom here. Standard Chartered agrees:

The global iron ore market has confirmed a cyclical downtrend in the past two months, with the benchmark price dropping 22% between April and June. This cyclical downtrend is a result of excessive supply in China since the beginning of 2014 (Figure 1) due to rising new supply and a substantial slowdown in China’s underlying demand. We expect supply to remain ample, while demand is likely to weaken on seasonal factors in Q3. A mild improvement in China’s steel sector should absorb part of the surplus and provide momentum for a price rebound in Q4.

China’s iron ore inventory is larger than the market had previously thought. Port inventory has stayed consistently above 100 million tonnes (mt) since March; in addition, local mines have large stockpiles as steel mills increase the use of imported ore to substitute for domestic ore. China’s iron ore imports will likely see small declines in H2-2014 versus H1, but full-year 2014 imports are now likely to be higher than we had previously forecast. We revise up our forecast for China’s imports from the seaborne market in 2014. In the meantime, credit conditions for steel mills and iron ore traders have tightened further since April, and macro policy is unlikely to benefit the bulk industry.

We lower our price forecasts to USD 87/tonne (t) for Q3-2014 and USD 105/t for Q4. This reflects our concerns about possibly weaker-than-expected fundamentals in the coming months. We lower our annual average price forecast for 2014 to USD 105/t from USD 118/t. It is highly probable that prices will dip to USD 80/t in August. We recommend that investors sell July-2014 and August-2014 contracts because the forward curve at present suggests both contracts are overpriced.

It’s not cyclical, it’s structural. There’ll be a restocking bounce later in the year and then down we go again.