Here are the iron ore charts for June 17, 2014:

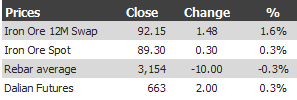

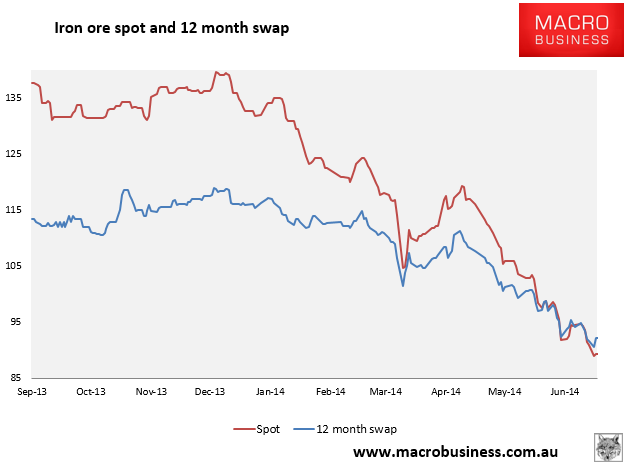

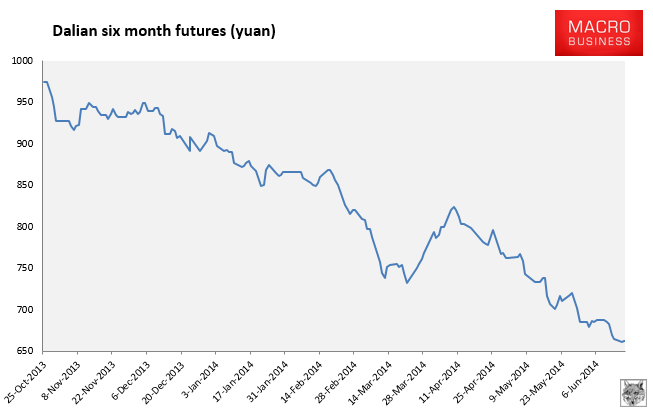

Better market action yesterday but still no cigar. Paper markets rallied late and the 12 month swap has opened a decent contango with spot. Rebar futures also bounced a touch.

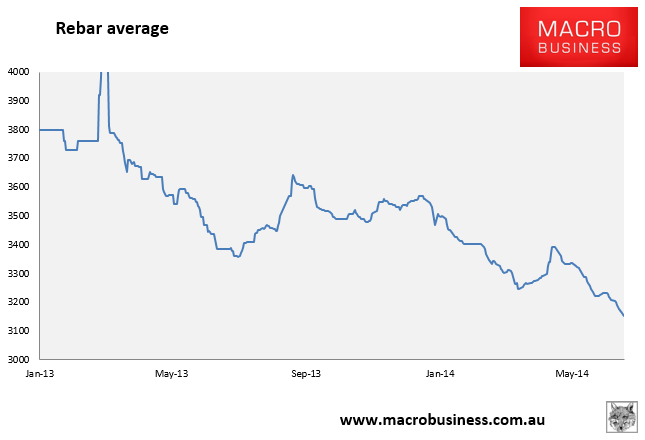

Physical is less encouraging. Spot went nowhere and rebar average continues to fade away indicating lousy fundamental demand. The Baltic Dry capesize component fell another 1%.

Texture from Reuters:

“There’s some short-covering after the sharp fall in prices. But the outlook is still bearish because of an oversupplied market,” said an iron ore trader in Singapore.

“We constantly receive offers from steel mills who are offloading their third-quarter allocation from their long-term contracts,” he said, adding he gets such offers of cargoes from about nine Chinese mills on average each day.

…The sharp fall in prices has reduced supply from smaller exporters such as Peru, Mexico, Venezuela as well as Iran, said another trader in Shanghai.

“Latin America, except Brazil, has gone off the market. That’s why I don’t see prices going below $85. Supply will be very tight below $85,” he said.

If mills are still selling third quarter contract cargoes then that tells you that they expect further deterioration in underlying demand. It’s good if supply from junior countries is falling already but even so most iron ore models expect 100 million tonnes of displaced production from these nations over the next three years so although it’s encouraging it’s expected.