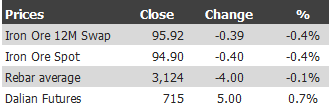

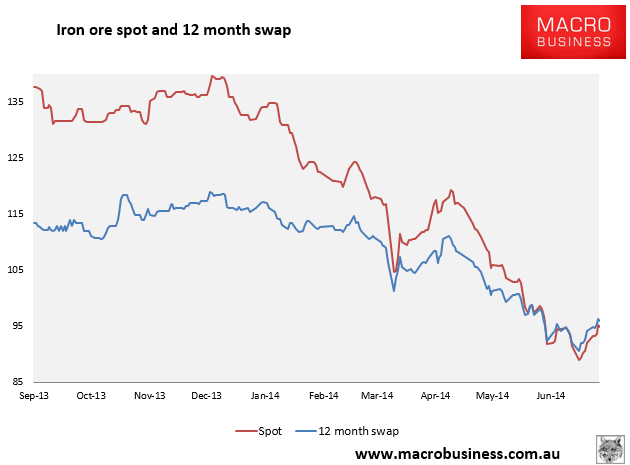

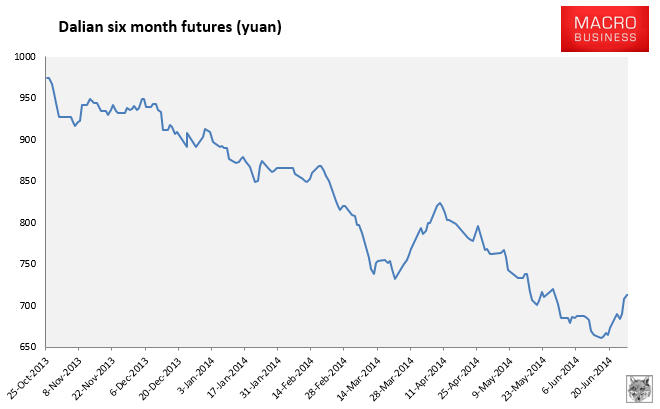

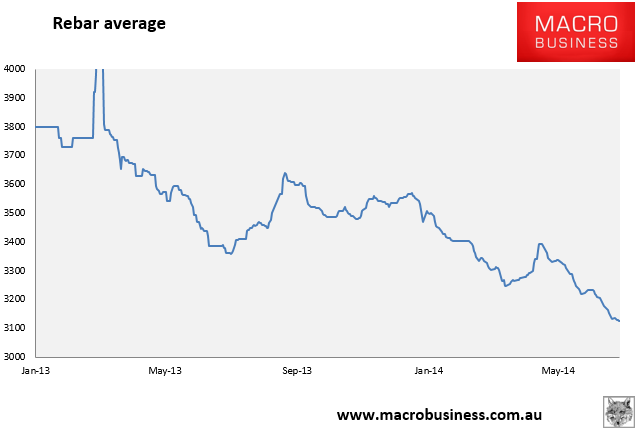

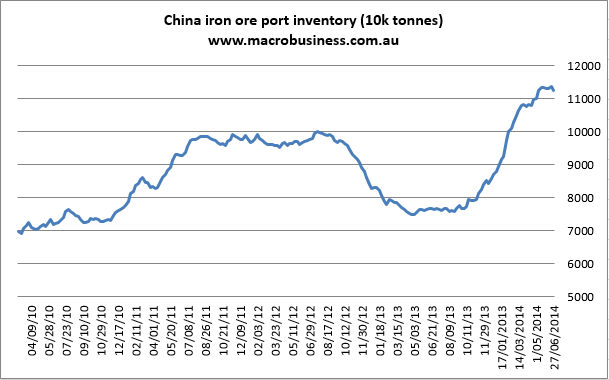

Here are the iron ore charts for June 27, 2014:

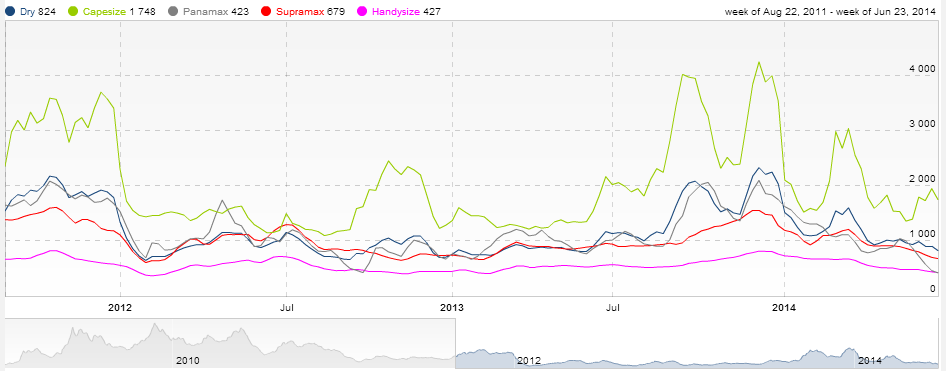

The paper market squeeze ran out of puff across all markets. Physical managed a little better including a 1.5% rise in the Baltic Dry capesize component. It’s off its early May lows but still very weak and signaling no restock:

A mixed performance in paper markets with Dalian off to the races but everything else easing back, including rebar futures.

Physical ignored Dalian and fell. So did rebar average. The Baltic Dry capesize put on 1.5% and port stocks fell one million tonnes or so.

The most important point to make is that so long as steel prices fall then iron ore can’t rebound very far. It’s really that simple.

Some will see the first decent draw down in port stocks as bullish and it will be if sustained but it’s far too early to tell. Texture from Reuters:

“I think we’ve passed the bottom,” said Mark Pervan, head of research at Australia and New Zealand Banking Group.

Most global miners have already hit their increased capacity so there is unlikely to be another substantial increase in supply, while Chinese mills that are running low on iron ore inventory may restock more in the second half of the year, he said.

“I think we’ll probably reach $100 in the near term. It’s not out of the question. We’re coming from an oversold position and $100 is still a cheap market,” said Pervan.

A decline in stocks of iron ore sitting at China’s ports may boost prices further, he said.

Mr Pervan recently cut his forecasts to levels still above those of the the fumblingly bullish BREE. There is more supply coming on. RIO will be in a position to keep ramping output in H2 by perhaps another 25 million tonnes. There is also Indian supply which will steadily return as well. This is going to ebb and flow, and BHP has scheduled maintenance to slow its output as well as other’s small mines coming under pressure, but the supply flood does not stop here. It slows a little then ramps up again next year, especially in H2 with the launch of Roy Hill.

Mills are not short of inventories, either. They are running leaner than they used to as supply frees up but could still destock for weeks to hit previous lows. Indeed, they’ve already restocked modestly in the past few weeks. Yes, the price could be the bottom for a while but that does not imply a rebound much past this point.

$100 may still be possible but that’s not “cheap” any more and the evidence points to this being a trader-induced short squeeze not any shift in market fundamentals or buying by steel mills.

Back to Reuters:

Prices for spot cargoes from Australia and Brazil rose this week in a flurry of deals with most of the shipments snapped up by traders, traders said.

“Some big trading companies in China need to pay their bank loans by the end of this month so they need to sell as much cargo as they can,” said a trader in Shanghai.

“For them to ensure good value for their cargo they also need to ensure that the price doesn’t go down, so they bid aggressively for cargoes on tender.”

…”If this rally has legs, we will know when July starts next week and my suspicion is the rally won’t sustain because market fundamentals haven’t really changed,” the Shanghai trader said.

That is my judgement as well. A classic short squeeze that is already outstripping real market appetite for cargoes at $95. Barring the Chinese releasing the brake on real estate it’s a new normal in which $100 will be hard to break.