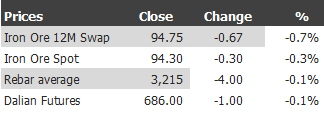

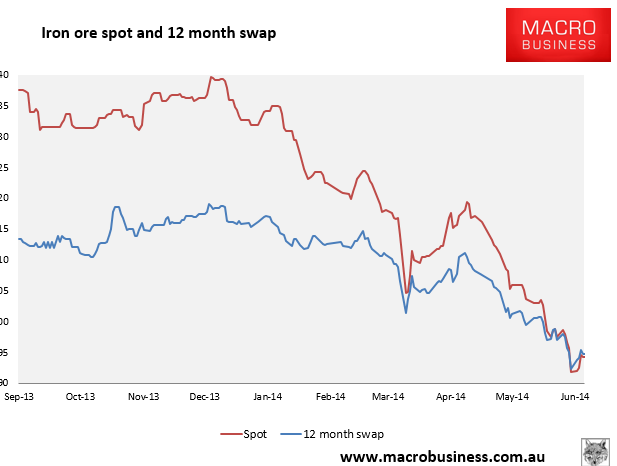

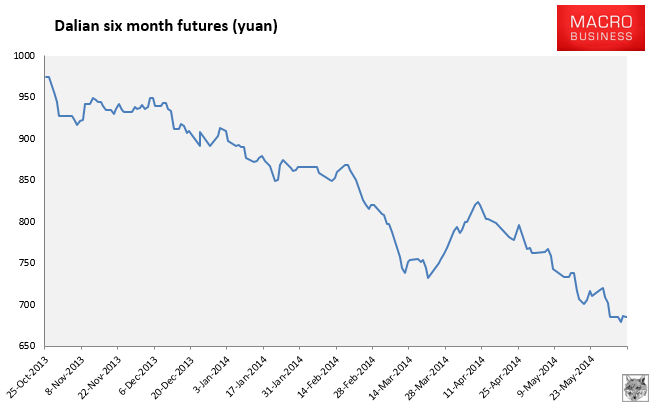

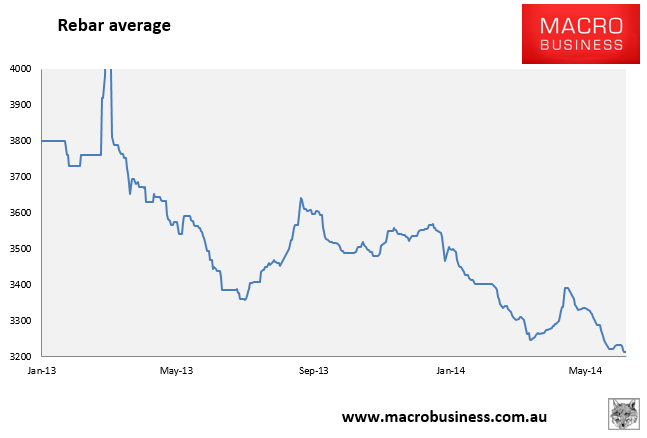

Here are the iron ore charts for June 5, 2014:

It’s sideways action mostly for paper and physical markets. Tipping the scale for further iron ore buying for me is another 5% jump in the BDI capesize component (although, as you can see above, it’s still very low). Also, the reaction to the bad news around the port stock investigations and tightening trader credit was muted suggesting the lure of low prices is still the dominant factor in the market. Texture from Reuters:

“The market remains oversupplied and the probe is putting further pressure on iron ore,” said the Singapore trader.

“I’m not sure demand is strong enough to push prices higher in a big way. No mills would buy in very large volumes at the moment because prices are most likely to fall again,” said a trader in Shanghai.

From more than 450,000 tonnes in January, the average iron ore inventory held by small and medium-sized Chinese mills has dropped to 325,000 tonnes, equivalent to 22 days of use, Goldman Sachs said in a report.

“Moreover, expectations of ample supply combined with ongoing liquidity issues should encourage mills to keep stocks at a mininum,” the investment bank said, adding that the high port inventory may “drive a destocking cycle” this year.

I still think we could run to $100 and expect that to be the new ceiling for prices for months yet to come.