From Credit Suisse comes some good news for iron ore as marginal Chinese iron mines stay closed after winter:

We expect further incremental closures to be forthcoming but do not believe there will be anything resembling a wholesale rush for the exit by domestic miners:

Not all production is at the top of the cost curve.

Some mines are captive to mills and, more broadly, mills gain a security of supply benefit from domestic production.

SOE miners have an incentive structure that rests on more than short-term commercial conditions.

Costs are flexible, Steelease has already reported that local governments have reduced taxes for some miners.

Some domestic expansions are still proceeding – FAI in domestic iron ore mining is up 15% ytd.

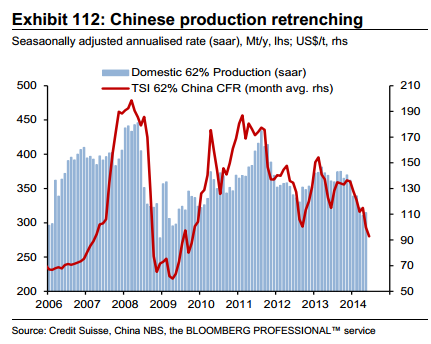

In 2009, when prices averaged $80/t, implied 62% Fe production was 326 Mt. Seaborne expansions will not therefore be substituted one-for-one into China and there will need to be both China and ex-China supply discipline, in our opinion.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.