Last week, Morgan Stanley finally broke the recent trend of broker upgrades to iron ore stocks. It has been equal parts amusing and disturbing watching the sell-side weathermen adjust their frail instruments before the building tempest. Little anemometers are spinning wildly off their axles. Plunging mercury has cracked the baubled reservoir at the thermometer’s base and is draining into the earth. Barometric needles are bent like gymnasts around the pin marking lowest ever readings. And still they don’t get it, blissfully recommending clients wade into the tumult.

A convergence of three storms is headed for the Pilbara and when it breaks a generation of miner’s hopes, dreams, shacks and towers will have been swept into an indifferent Indian Ocean. Only then will patient investors rescue the gems from under mounds of flotsam

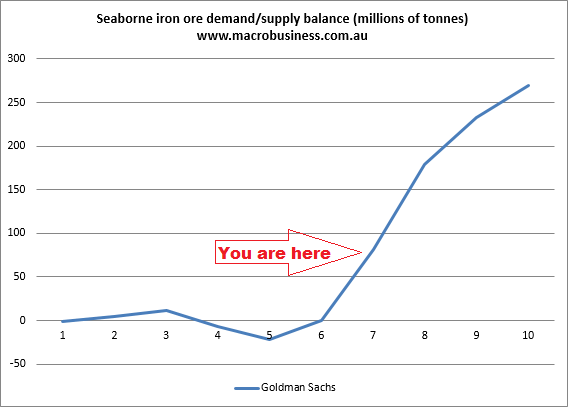

The first mountainous thunderhead is the demand and supply balance, the leading tip of which has only just made land fall:

The chart is based upon committed iron ore projects, ongoing Chinese steel demand growth and reasonable assumptions about Chinese iron ore mine closures. The current seaborne iron ore surplus is thought to be 6-7% of the market. A similar sized surplus knocked 70% off the price of coking coal. Iron ore is down 50% so far yet it is locked into a trajectory of surplus supply above 20% of the total market, a truly vast glut.

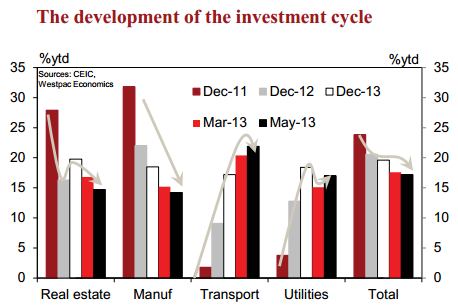

A second converging front is blowing in from China. Chinese authorities are managing their current circumstances nicely as their property bubble begins to deflate and they support the wider economy with infrastructure spending and productivity-based reform (a real lesson for Australia there!). Fixed-asset investment growth – the absolute driver of iron ore demand – has eased to 17% per annum in May as the balance of components shifts:

Still impressive growth and that’s the problem. Remember that real estate absorbs roughly half (estimates range between 40-70%) of steel output. The compositional change in investment is weighing on steel demand even before rebalancing proper takes place. If China is serious about shifting from investment-led to consumption-led growth – so that it can dodge the kind of middle income trap that has swallowed most developing economy miracles – then investment will have to fall much further. Needless to say, over the medium term, that will shrink iron ore demand at a pace that the rest of the world will be unable to offset.

Which brings us to the third converging wall cloud. A construction boom that creates a steel boom exaggerates its own demand. It takes vast amounts of steel to build the furnaces, mines, railways and ships that drive steel production growth. When the underlying construction pulse eases, the virtuous cycle of steel industry expansion reverses and huge overcapacity emerges, such as the hundreds of millions of tonnes of potential steel output currently idle in China. Steel prices sink to paralytic lows and mills jam those collapsed margins into their supply chains. As steel margins improve each time and production rises, oversupply hits again and prices tumble once more, forcing further deflation into the supply chain. The entire price deck of the steel and iron ore industries shunts repeatedly lower to the marginal cost producer in both.

This deflationary dynamic is well underway but the cycle is being held in check by China dumping its excess steel on the world market. That is not going to last either. Steel is a strategic commodity and before very long nations will begin to lock out Chinese steel to protect local production capacity. That will force-feed the deflationary cycle over the medium term.

These three storms are converging into an enduring once-per-century cyclonic event for the Pilbara. It will seethe for years to come and before the gale passes inland, iron ore juniors will be wiped off the map, Fortescue Metals will be blasted to driftwood, Roy Hill will be a stranded curio, Rio Tinto will be fending itself from the rocks and BHP will be de-masted.

The coming torrent will sweep away the peremptory and the patient will inherit the red earth.