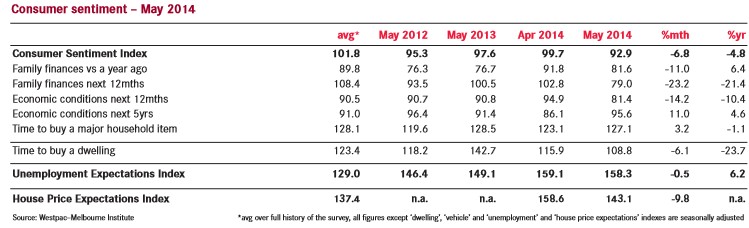

The Westpac-Melbourne Institute has released its consumer sentiment index for May, which confirms that the mood of the Australian consumer has turned sour on the back of the Budget, with the index plummeting 6.8% in May to 92.9 – the lowest reading since August 2011.

Here’s Westpac’s Bill Evans’ explanation of the result:

The sharp fall in the Index is clearly indicating an unfavourable response to the recent Federal Budget. This puts the Index at its lowest level since August 2011, before the Reserve Bank began its recent rate cut cycle. Since November 2011 rates have fallen from 4.75% to 2.5% and the Index is now back below pre-rate-cut levels.

The fall of 6.8% is comparable to the 7% fall we saw in the Index in May 2013 (from 104.9 to 97.6). That sharp fall was also in response to the Budget in that year and came despite the Reserve Bank cutting rates in the same month.

Confirmation that the Budget was the key driver in both years is the response to a special question in the survey which was run in both years asking: “What impact do you expect the Federal Budget to have on your family finances over the next 12 months?”

For 2014 the responses were: 3.1% (improve); 37.7% (stay the same); 59.2% (worsen). That compares with responses in 2013 of: 5.6% (improve); 48.7% (stay the same); and 45.6% (worsen).

The initial response to a Budget can sometimes be an overreaction. For example, in 2013 the Index bounced back by 4.7% in June.

It is also true that it is not unusual for Sentiment to plummet at Budget time. Other comparable falls were: May 2010 (–7%); May 2009 (–4.3%); May 2006 (–6.4%); and May 1995 (–7%).

As indicated by the “special question”, respondents were particularly concerned about the impact of the Budget on their own finances. The sub-index tracking assessments of ‘family finances compared to a year ago’ fell by 11% to its lowest level since July 2013. The sub-index tracking expectations for ‘family finances over the next 12 months” slumped 23% to its lowest reading on record. There was also concern about the near term economic outlook: the sub-index tracking expectations for ‘economic conditions over the next 12 months’ fell by 14.2% to its lowest level since August 2011.

In contrast, respondents seem to be signalling that the Budget will assist the economy over the medium term. The sub-index tracking expectations for ‘economic conditions over the next 5 years’ was boosted by 11%, while the sub-index tracking assessments of ‘whether now is a good time to buy a major household item’ rose by 3.2%.

Despite the overall negative response to the Budget, respondents did not expect their job prospects to deteriorate. The Westpac Melbourne Institute Index of Unemployment Expectations was largely unchanged declining from 159.1 to 158.3.

In contrast, attitudes towards the housing market took a tumble. The index tracking assessments of ‘whether now is a good time to buy a dwelling’ fell by 6% and is now at its lowest level since November 2010, when the Reserve Bank had been lifting interest rates, and 25% off its highs of September last year. This response is unlikely to be solely driven by the Budget. Respondents have been lowering their confidence levels for some months. Between September last year and April the Index had already fallen by 20%.

Confidence around housing is particularly fragile in the major states with the Index being down by around 30% from September’s highs in both NSW and Victoria.

Waning confidence in the housing market is also apparent in the Index of House Price Expectations. The Index fell by 9.8% in May to its lowest level since January 2013. Concerns over high prices and limited affordability are likely to be the key reasons behind these trends.

The Reserve Bank Board next meets on June 3. As indicated in the minutes of the May Board meeting, the RBA expects to keep rates on hold “for some time yet”. The big issue for the Bank and the economy will be whether this strong reaction from consumers indicates that the recent improving trend in consumer spending is interrupted. While households have clearly reacted to some very unnerving headlines, the Budget has clearly been structured to minimise its impact on the fragile recovery.

Over the first 3 years of the Budget savings measures will only ‘take’ around 1% of GDP out of the economy and only $1.7bn (0.1% of GDP) in 2014/15. The major savings are structured around the out years from 2017/18 onwards.

Over time households will recognise this strategy and it seems unlikely that the Budget will derail this recovery in the face of a strong lift in household wealth (around $700bn) associated with recent house price increases; a very high household savings rate which is supporting a substantial strengthening in household balance sheets; and very low interest rates that are likely to remain in place until the second half of 2015.

The internals are provided below. Note the big falls in “family finances” and “economic conditions in the next 12 months”, which drove the fall. House price expectations also weakened materially, especially in the larger markets.

Some positives to come out of the release are that unemployment expectations were largely unchanged, and “time to buy a major household item” rose in May, which could support spending.

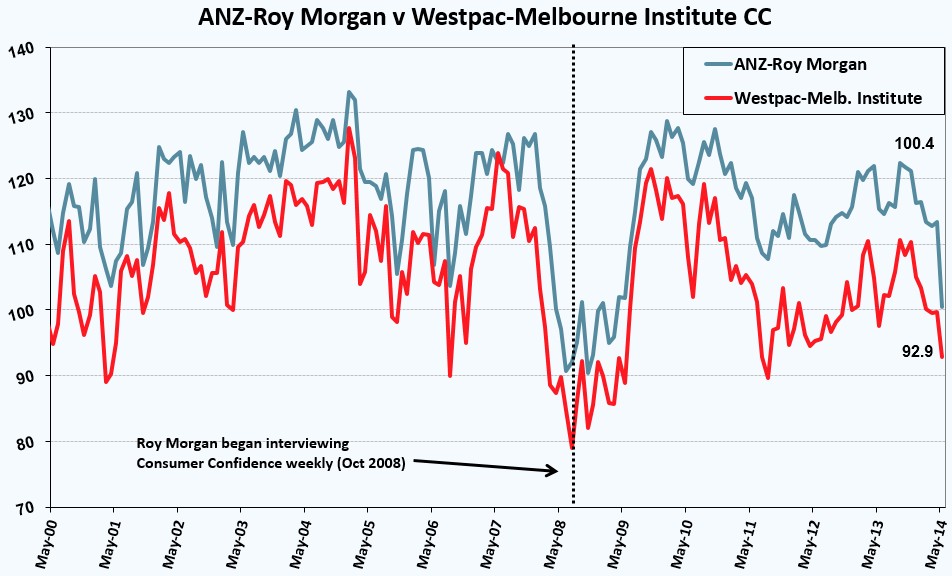

Finally, here is the Westpac-Melbourne Institute consumer sentiment index plotted alongside the ANZ-Roy Morgan consumer confidence index, with both moving in the same direction – down: