The AFR’s Agnes King has written a ripper article highlighting the egregious nature of Australia’s superannuation system, which has increasingly become a mechanism for richer older people to avoid paying tax, rather than a genuine means for Australians to pay for their own retirement and avoid drawing on the Aged Pension:

An Australian Financial Review analysis of Australian Taxation Office statistics shows almost 9200 self-managed super funds have a balance of more than $5 million, a rise of 76 per cent in the past three years, and the number of funds with over $10 million has doubled…

Tax advisers have raised the alarm on the number of super-wealthy clients able to have incomes taxed at zero to 15 per cent, instead of the current top rate of 46.5 per cent, by using generous concessions and “cracks” in the superannuation system.

“These are people with $10 million to $20 million in self-managed super, they’ve funded their retirement several times over, they don’t need concessions,” said one tax lawyer…

The most popular [strategy] is 55-year-old executives who start drawing a tax-free pension from their fund, while tipping their entire salary into it and effectively reducing their taxable income from 46.5 per cent to about 15 per cent…

Advisers say the sheer volume of this behaviour is causing “material leakage” to the nation’s revenue position.

There are two key issues at the heart of this problem.

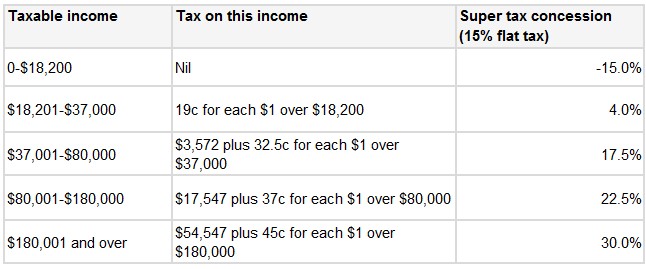

First, superannuation concessions are very poorly targeted, with higher income earners receiving the lion’s share of concessions when they contribute to super, whereas lower income earners actually incur a tax penalty (see below table).

As noted by John Hewson recently:

As a result of this poorly targeted tax concession, 36.1 per cent of the benefits go to the top 10 per cent of income earners, whereas the bottom 10 per cent don’t receive any assistance at all, but are instead penalised…

Treasury estimates that from the combined support of superannuation tax concessions and the age pension, most people (about 80 per cent) receive around $270,000 support over their lifetime. In contrast, the top 1 per cent of male income earners receives about $520,000 support over their lifetime, because of significant tax concessions to high-income earners.

Second, courtesy of the Howard Government, since July 2007, superannuation paid to anybody over the age of 60 is tax free, unless they are members of some untaxed public sector funds.

These two factors combined have made superannuation the tax minimisation strategy of choice for high income baby boomers approaching retirement.

With superannuation concessions costing the Budget many billions of dollars (and growing fast), and most of the benefits flowing to wealthier people, it is high time that all sides of politics attacked this lurk head-on, in the interests of both long-term Budget sustainability and equity.