By Catherine Cashmore, a market analyst, journalist, and policy thinker, with extensive industry experience in all aspects relating to property. Follow Catherine on Twitter or via her Blog.

As we approach the Federal budget, once again we have to endure another round of economic nonsense, as the Treasurer tries to convince ‘ordinary’ Australian’s that the country is ‘running out of money’ – facing a ‘budget crisis.’

So ingrained is this message, that few question it.

Instead, Talk Radio is flooded with callers; outraged at the ‘debt burden’ they imagine will be passed onto their children. A lifetime of work and servitude lay ahead – not only charged with the responsibility of paying down their own debt – but the government’s debt as well!

For an administration that wants to retain leadership through blaming the last government for the ‘mess’ they’ve reputedly left us in, it’s a convenient message to sell.

“Fiscal responsibility” is the catch term of the day, cuts to health services, education, welfare, job seekers allowance, wages, and proposed ‘back to work’ assistance for those ‘laid off ‘ from the car industry – you name it, it’s on the table.

Everything that is, except the ‘golden egg’ of speculative windfall gains that can be gleaned from the game of ‘Monopoly’ – or to be more accurate – the increasing value of land.

Unlike countries such as Germany, which have historically managed to divert speculation away from residential real estate, with the focus being on productivity instead. Here, we’re all subject to an economy, built on the retirement ‘wealth egg’ of land – our personal economic leverage for all lifestyle and business needs.

It used to be called ‘Monopoly.’ Today its termed – ‘Getting onto the Property Ladder.’

The rules of the game are simple. The player uses as much debt as they can borrow – to ‘buy and hold’ as much as they can – and those who ‘got in’ at the beginning of the lending boom, securing the ‘best’ plots available, win the game.

In relative terms, the ordinary homeowner doesn’t advantage much, but what else can they do? Retire still renting? Or become a contestant and hope their house yields enough ‘appreciation’ to support them when they retire. (But not so much that their children can’t get a foot onto the first ‘rung’ of course, and leave home before the age of 40.)

Our lives are therefore spent working to pay off a mortgage – or two. (That is, unless you’re an unlucky tenant, in which case you play a game called ‘The Rental Trap.”)

The question we ask however is; ‘At what expense?’ – or perhaps “At whose expense?”

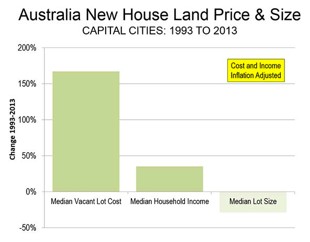

As demonstrated by a recent HIA report – land values continue to skyrocket – with the weighted median across all capitals during the final quarter of December 2013, rising to the:

“Highest level on record… a 22.3% increase on the final quarter of 2012.”

Or perhaps it can be better illustrated on a graph Wendell Cox (author of the “Annual Demographica Housing Affordability Survey”) constructed which cuts through the usual measures used to convince readers that ‘housing has never been more affordable,” with overwhelming focus on mortgage serviceability rates alone.

Instead, it demonstrates the speculative nature shaping the property cycle, which affects not only established house prices, but building activity as lot sizes reduce, whilst land price per square meter, outpaces income growth considerably.

As I said in my last column, whilst citing the political motivation behind housing policy; “The smoke screen debates on affordability and scrapping negative gearing, are just that” smoke screens. Something that was subsequently confirmed upon release of the Government’s Commission of Audit, which ruled out any consideration of a change to housing policy – better to tax income instead – easier for the top 10% to avoid it, whilst low to middle income earners suffer the shortfall.

We ‘all’ have to shoulder the burden, tighten belts, work harder – pensioners included!

‘All’ that is, except those imposing the ‘rules’ – whose ‘entitlements’ are immune from any ‘fiscal responsibility.’

Yes – the Members of our Federal Government – the ‘issuers’ of our monetary supply, offset through taxing those who do have to ‘earn’ dollars before they can ‘spend’ it – whilst our Government ‘earns’ nothing – but is rather elected, and charged, to manage the budget in the best interests of its working population to promote economic growth – for which education, health, ‘back to work’ initiatives and so forth, are vital pillars.

There is no evidence and no economic wisdom, that indicates running a surplus is good for the economy.

Something, Steve Keen does an excellent job of demonstrating in a recent lecture given in Sydney, in which he shows the inevitable consequence to GDP should our Government attempt to do so!

Economic orthodoxy, which stubbornly insists austerity measures to pay down government debt, should take precedence whilst imposing onerous taxes on its working population, are lessons that should have been learnt following the Great Depression in the 1930s.

There is nothing ‘new’ about this – indeed, Australia’s oldest PhD at 93 – Dr Elisabeth Kirkby – has just written a 100,000 word thesis on it. And whilst valuable lessons reaped from the grains of history are ignored, the patterns that led to our greatest economic disasters are repeated.

What all demonstrate is, when the government tightens its belt, for no other reason than a vein attempt to ‘spruik’ a surplus, it has the unwonted effect of withdrawing money from the economy – leaving the private sector (the working class population) to pick up the slack.

Therefore “repairing the [government] budget” with the claim it’s putting Australia “on the right track” – is not putting the fate of ‘Australian’s’ on the ‘right track.’

It is the Government’s responsibility to make sure our monetary system works for the population, by spending enough money into the economy to keep employment and productivity thriving.

What however, is economically irresponsible, is to have a growing deficit offset by tax receipts, that reward speculation and by consequence, widen the wealth gap between rich and poor. Ironically, the very gap the tax and transfer system is supposed to narrow.

In other words, we are not burdening our children with debt – we are burdening them poor economic management.

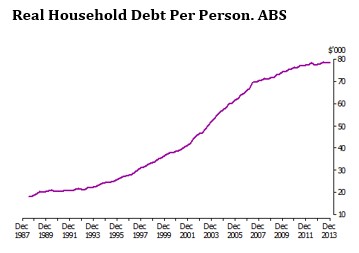

As austerity measures bite and the retirement age increases, the majority of Australian’s will be working longer and harder – and whilst the Government pays down its reputed ‘debt burden’ – private debt levels will continue to increase as families borrow to ‘afford’ the basic necessities they need, most likely leveraged against their own homes.

For those that need a reminder – as demonstrated in the latest ABS social trends report – total household debt was $1.8 trillion as at the end of 2013 – higher than it has been at any other time over the past 25 years.

Low interest rates aside – $1.8 trillion is a hefty figure.

To put it in some kind of context – a trillion, is a thousand billion.

The sun is set to burn out in approximately 500 billion years. A trillion is so large; it’s almost meaningless in real terms.

Total Government debt securities on issue are around $542 billion (as at March 2014 – RBA) – that’s around 35% of our GDP.

In contrast, our household debt to GDP ratio is estimated to be 97% (as at December 2013 – RBA) – assisted by low interest rates and an array of financial products to ‘woo’ new borrowers into the property market (such as shared equity schemes, interest only loans, redraw facilities, offset accounts and so forth.)

Therefore instead of our current leaders asking Australian’s what they can do to assist Government debt. We should be asking the Government, what it will do to assist private debt? Particularly as we move forward over the next 12 months or so, and the lending cycle turns.

Capitalism?

Of course, this problem is not unique to Australia. Thomas Piketty’s book “Capital in the 21st Century” has just come out to great acclaim, choc full of statistics to demonstrate how income earners – the vast body of productive workers, who prop up the local economy through the taxes they pay and products they produce – are the losers, compared to those who hold stores of unproductive wealth.

The book focuses on the ‘1%ters’– advanced through gifts of inheritance – those who hold the vast majority of ‘assets.’ Controllers of the stock and bond markets – collecting their ‘economic rent’ by way of hording property, and effectively, ‘buying’ protection through lobbying seats of power.

It’s an age old game, and in a world where gaining political leadership is only possible with vast sums of ‘advertising’ dollars, lobbying is crystallised into the system.

We’re currently seeing this with the ICAC investigation, as it uncovers a web of alleged political corruption, with illegal donations from property developers and other sources, funnelled into a Liberal Party slush fund.

Meanwhile, Clive Palmer has been accused of “spending money like a drunken sailor” to secure a third seat in Senate for his PUP party.

Palmer reportedly entered the leadership battle due to “poor policy decisions” by the Gillard Government – the ‘carbon tax’ in particular being highlighted, which promised to negatively impact his core business.

However, his other policy evaluations leave much to be desired.

For example, Palmer’s ‘housing affordability’ plan, is to make home loans tax deductable for the first $10,000 – a move which will unquestionably push land prices higher, as future buyers factor the savings into their budget and adjust price expectations accordingly.

But then, considering Mr Palmer’s significant land holdings, which are said to include:

- “A six bedroom, 11 bathroom, 22 car garage property in Queensland – along with;

- An array of golf courses. As well as;

- “Family and associates” owning a total of “11 homes in the Sovereign Islands” on the banks of the Southport Broadwater – as well as;

- “Other known properties at Broadbeach Waters on the Gold Coast, Fig Tree Pocket in Brisbane, Jandowae on the Darling Downs, Queensland, and Port Douglas” and notwithstanding;

- “An undisclosed number of properties held in trust for their daughter.”

I suspect lowering land values, may not be top of mind.

The wealth tax ‘solutions’ Piketty proposes to stop the ‘gap’ widening; fail not only by the confused definition of what one would consider ‘wealth.’ (A Rembrandt painting, or luxury Yacht for example?) But also that of ‘capital.’

In modern terminology, capital is used for anything that yields a profit – which under our current system includes land. However, in classical terms, capital is a factor of production – a depreciating asset and one, which can be reproduced.

In a society built on the foundation of ‘free markets,’ factors of production flourish under competition. If one widget costs too much, an entrepreneur will find an innovative way to produce the same widget at a cheaper price.

It’s called capitalism.

Land however is not a factor of production. It can’t be moved or reproduced and it’s limited in supply. Therefore the revenue stream generated from the unimproved portion alone is due to its locational advantage, and little else.

The free market activities in a capitalist society, cause land values to increase – and considering this is through no act of individual exertion on the vendor’s side, but rather the collective efforts of the community, it makes sense that most consider owning a well located plot of land, better than both money in the bank and the wages they have to ‘earn.’

This is why increasing charges on the revenue stream ensuing from the locational value of land, and recycling it back into the community – (which is where it came from, and where it belongs) – by way of a tax shift off productivity (wages) and onto our valuable and limited natural resources – was termed the ‘least bad tax’ by the capitalists Milton Friedman and Winston Churchill – to name but a few.

Rising land values harm capitalism, they increase the rent for small business owners, always benefiting the landlord but never benefiting the wage earner. Furthermore, rising land values force young people out of the market, whilst making those ‘in’ the market wealthy – and widening the gap between ‘rich and poor.’

When land prices inflate, jobs are lost as more revenue is taken away from productivity and soaked into the ground.

It’s not called capitalism; it’s called capitalizing -‘taking advantage of’ community created revenue – the total of which is pocketed by the landowner.

This is why land prices are so high – and ‘vested’ interests of policy makers always act to push them higher.

The great man Buckminster Fuller – architect, systems theorist, author, designer, inventor, and futurist – once said;

“You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete.” (H/T author of soon to be published book “Land” Martin Adams)

We live in a democracy, therefore any change to the status quo needs to come from the ground up – we will never get it from the top down.

The Henry Tax Review set out recommendations for transitioning our economy based on the ideas penned above.

How we get there is worthy of debate – however thankfully, due to the internet and a new age of enlightened ‘priced out’ folk, we can start that debate in 2016/17, by using our own preference and economic wisdom to vote a government which acts to widen the rich/poor divide out. By which time there ‘may’ (?) be better options to vote in.