Some things just do not pass the laugh test.

Despite negative real wages growth, stable mortgage rates, and ongoing solid house price growth, the HIA-CBA Housing affordability index has magically registered an increase, with housing affordability supposedly at its most favourable level since March 2002:

“The continuation of record low interest rates, combined with decelerating home price increases and growth in earnings over the quarter saw the HIA-CBA Housing Affordability Index improve to its most favourable level since March 2002,” commented HIA Senior Economist, Shane Garrett.

“The HIA-Commonwealth Bank Housing Affordability Index improved by 2.1 per cent during the first quarter of 2014 and affordability is now 10.8 per cent more favourable than a year ago,” explained Shane Garrett. “Increases in home prices over the past year have been significant. However, the impact of lower interest rates and continued earnings growth has ensured that home purchase affordability has improved over the past year for existing home owners and those on the cusp of entering the market in the short term,” Shane Garrett pointed out.

“The RBA has signalled that interest rates are set to remain low for some time,” added Shane Garrett. “As home price pressures ease off, we expect home owner affordability to remain reasonably favourable for the foreseeable future,” predicted Shane Garrett.

The below chart plots the time series since 1994. As you can see, housing affordability is supposedly at a 12-year high, according to the HIA:

Regular readers will know that I have huge concerns with this index.

First, housing affordability (i.e. the cost of the home relative to incomes) and mortgage serviceability (the immediate cost of servicing the loan) are not the same thing. The former remains near all-time lows, whereas the latter has improved significantly thanks to the reduction in interest rates, which are unlikely to always remain so low. In this regard, the HIA’s index should really be labelled a “mortgage affordability index”, since it measures the current cost of obtaining a mortgage on a median priced home, not the structural cost of housing per se.

Homes are currently only “affordable” if one assumes that current low mortgage rates are permanent. But given most mortgages now are for 25 to 30-year terms, it is fair to assume that repayments won’t always be so low.

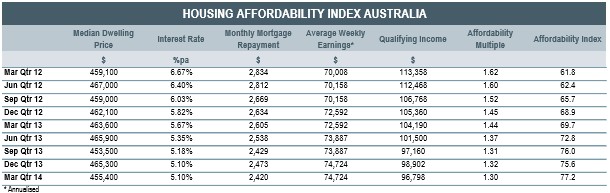

Second, the dwelling price inputs into the HIA’s index are dodgy. As shown below, the median dwelling price of 455,400 as at March is said to have decreased by 2.1% over the quarter and by 1.8% since March 2013. Hell, it even says that the median priced home is worth $3,700 less than March 2012:

Now compare this result to the ABS’ house price index, which recorded 11.5% growth over the year and 15.3% growth since March 2012.

Something does not add up (unless you work in the MSM):

unconventionaleconomist@hotmail.com