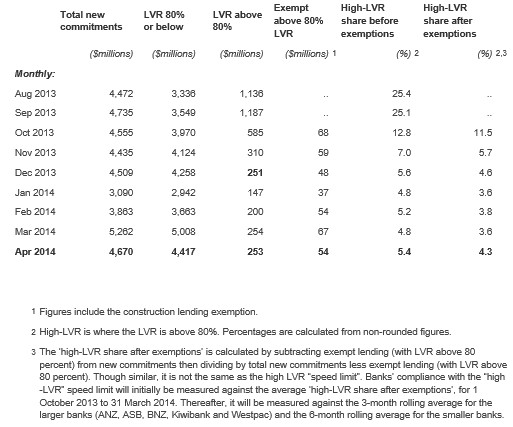

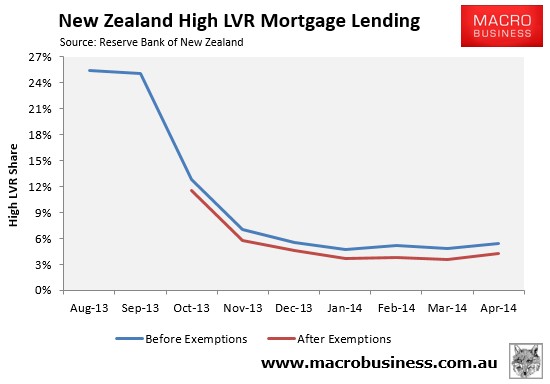

New statistics released by the RBNZ show that the share of high LVR lending plummeted following the introduction of the LVR cap, falling from 25% in the months proceeding the change to just 5.4% (before exemptions) and 4.3% (after exemptions) as at April 2014:

Advertisement

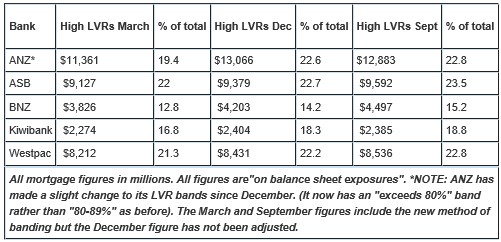

Moreover, according to figures released today by Interest.co.nz, New Zealand’s biggest banks “have sharply reduced their overall exposure to high-LVR lending”:

The table below shows the amounts the banks had outstanding in high-LVR mortgages as of March and compares this with the figures as of December and September – immediately prior to October’s introduction of the LVRs…

[There has been]…a substantial rebalancing of the banks’ overall mortgage portfolios as fewer new high LVR mortgages are created and presumably many existing loans get re-categorised as low LVR loans following either a reduction in principal or an upward revaluation of the property.

Advertisement

Australia needs concrete rules to mitigate mortgage risks, not fluffy prudential practice guides.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.