Huge negative gearing losses revealed

Advertisement

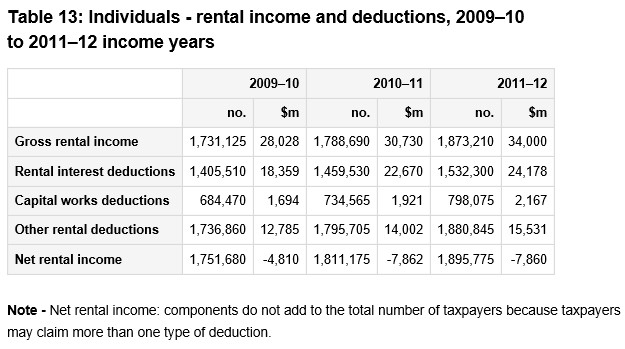

The Australian Taxation Office (ATO) has just released its 2011-12 Taxation Statistics, which once again revealed Australia is a nation of loss-making landlords, with 15% of taxpayers owning rental properties declaring a combined $7.86 billion of losses.

According to the ATO, there were 1,895,775 property investors in Australia in 2011-12, up from 1,811,175 in 2010-11 (see next chart).

Advertisement

Some more interesting (worrying?) facts that can be deduced from the ATO data includes:

- Just over 1 in 7 (1,895,775) Australian taxpayers are a property investor (either negatively geared or positively geared), claiming a total of $7.859 billion in rental losses;

- 1 in 10 Australian taxpayers (1,266,540) are a negatively geared property investor claiming a total of $13.799 billion in rental losses;

- The average income loss for all property investors in 2011-12 was $4,146; and

- The average income loss for all negatively geared property investors in 2011-12 was $10,895.

Advertisement

An in-depth report will be provided in the MB members report for May.

unconventionaleconomist@hotmail.com

Advertisement

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement