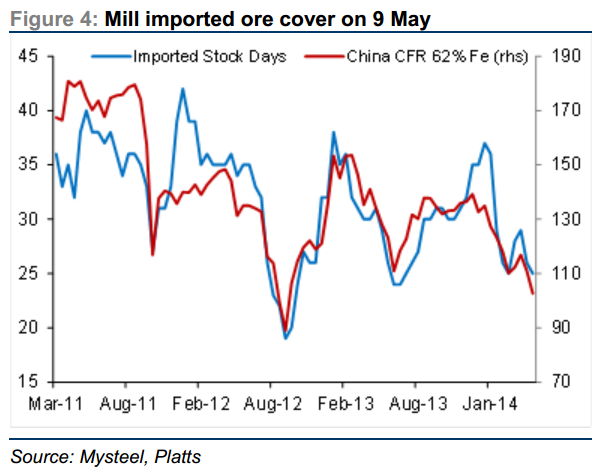

We know that Chinese steel mills have been destocking raw materials, which is one significant reason why the price has been falling. Courtesy of Credit Suisse, here was the state of inventories on May 9 (the latest update):

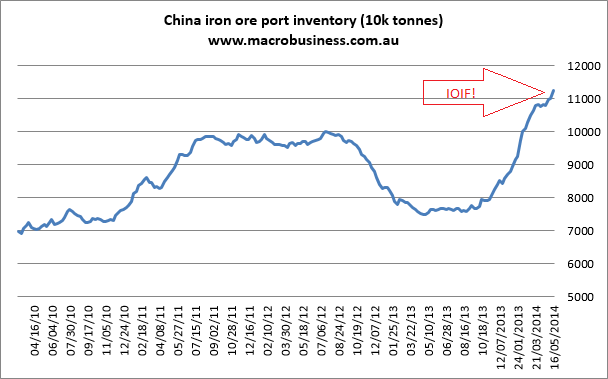

25 days of coverage is low by historical standards (and it’s probably lower now) but there are reasons the believe it’s not so low in longer term context. The downtrend in inventory stocking is clear over time. It’s simply no longer necessary for steel mills to tie up capital in the storage of excess iron ore given the oversupply situation. As well, without the prospect of large stimulus packages, mills can be confident that demand will not suddenly spike. Finally, there is the giant port pile:

As Macquarie Bank has noted, still mills also seem to be storing more stock at ports than in the past so the real inventory coverage ratio is probably higher than the first metric suggests.

Even so, inventories are clearly not high in aggregate, probably around the median if we if adjust for lower stocking over time.

This is vital in assessing how low the iron ore price can go. In 2012 high port and mill inventories enabled an epic destocking that crashed the price over $60. If mills decide to run down stocks to similar levels we could do another $20 plus downside this time.

But will they? There is one major argument against and one major argument in favour.

The argument against is that the accumulated inventories give Chinese mills pricing power. With good stocks they can out wait the Pilbara cartel which aims to sell stock in a manner that maximises price, sometimes pausing, sometimes lifting sales. If China is well stocked then it can wait out these machinations as miners need to deliver volume targets.

However, it’s probably not wise to see steel mills as a monolithic player in game theory. As such, they could again pursue individual interests and destock en masse if their own margins are too weak and/or demand conditions deteriorate.

Some of that is happening now but output is still high on local and export demand so it probably can’t run too far. That’s why I have a $95 target for the current move.

The big risk of deeper downside comes if a demand shock arrives from a further downturn in Chinese construction, which seems inevitable at this point, and if that combines with seasonal weakness in Q3. There are also the ongoing risks of further bankruptcies in the Chinese steel sector as the reform process continues.

I still see the second half as more troubled than the first despite the ramp up of supply slowing for a little while.