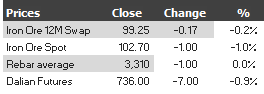

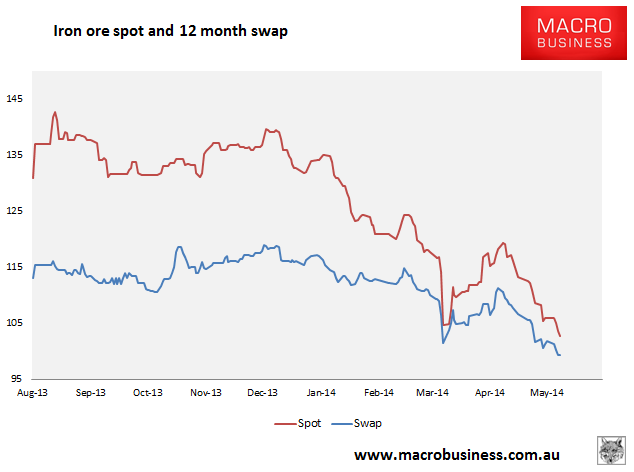

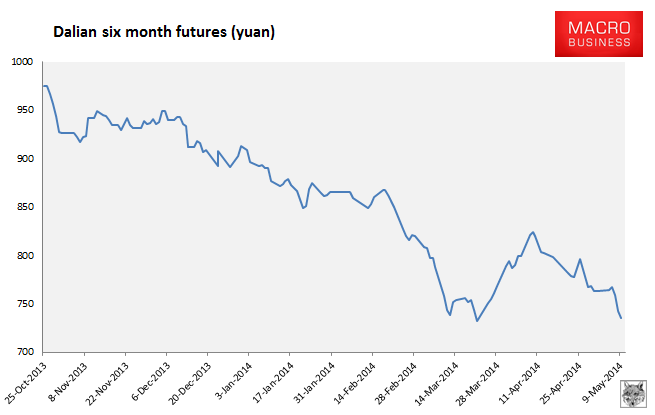

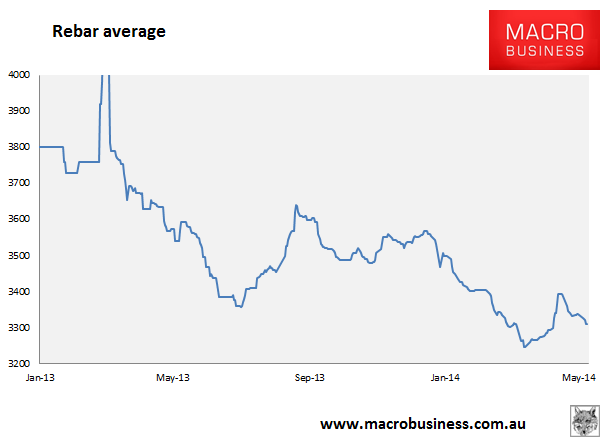

Here are the iron ore charts for April 10, 2014:

Another bad day for prices on Friday. Paper market falls eased but still hit new lows in the 12 month swap and rebar futures. Dalian futures are within a whisker of a new low as well.

In physical markets, spot is down, rebar eased a bit and the Baltic Dry capesize component fell another 4.5%.

Texture from Reuters:

“A lot of buyers are holding back. They feel the market will drop further,” said a Shanghai-based iron ore trader.

“Many traders and even mills are offering their cargoes in the market so supply is huge.”

“With current prevailing weaker sentiment, we’ve adjusted our Q2 2014 average forecast down $4 to $116 but remain upbeat for a price recovery in the coming months as seasonal Chinese demand improves,” ANZ bank said in a note.

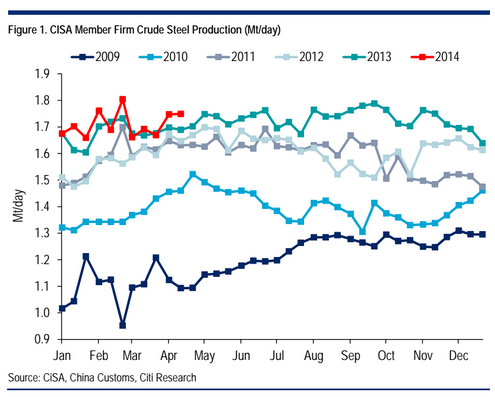

There’s nothing wrong with demand and the recovery is already here. Steel is pumping out at the usual astonishing rate. CISA released its late April output figures over the weekend and production at large mills is up 2.7% from mid April. The total output figure wasn’t released for some reason but it’s likely up further from mid April and is running modestly ahead of 2013. From Citi (before Friday’s update)

It may not be the boom growth of yesterday but it’s still growing at low single digit rates. Reuters goes on:

“We have long been saying we see 2014 as being the year when iron ore supply will finally accelerate ahead of demand, pushing prices below $100/tonne,” CLSA commodity strategist Ian Roper said in a report.

“As we move into oversupply, the market will become increasingly challenging for suppliers who’ve only recently entered the market while prices were high,” said Roper, who sees global iron ore supply growing by 140 million tonnes this year, mostly from top producers Australia and Brazil.

“I don’t think $100 can be a support level. The chance of prices falling below that is increasing and we may see it happen in May,” said the Shanghai trader.

Yep, it’s supply, too much of it.

The odds are that this imbalance is not going to improve in the second half. Supply growth will ease but demand is likely going to weaken as well as the property shakeout gains pace. A repeat of the 2010, 2011, 2012 production pattern looks a fair bet (see above chart). We may see housing stimulus by year end but remember that construction lags easier credit by six months so we’re talking 2015 before we see any real pickup in iron ore demand. As well, the prudential measures around ponzi borrowers in the steel sector are going to remain in place so more default shocks keep the risk of further price gapping live.

Business Spectator’s Bartho has details of Goldman analysis that is right about the implications:

That rising curve of over-supply would have obvious implications for iron ore prices and the Goldman team, like many others, see it falling back to around $US80 a tonne next year – and staying there as the expansion in production capacity continues.

…A separate piece of research focused on the “extraordinary fixed cost leverage” of Australian producers…While Goldman says iron ore exports will continue to rise strongly – 19 per cent this year and another 9 per cent off that expanded base in 2015 – it says the lower prices will lead to a $US4 billion decline in revenue.

The fixed cost leverage that the report is focused on shows up in a $US10 billion dive in pre-tax earnings.

…Obviously the miners – most notably Rio Tinto and BHP Billiton – are addressing the productivity challenge and the compression of their margins by making massive and continuing reductions in their cost bases while still lifting their output.

…The challenge is somewhat more acute for smaller players and even more acute for aspiring producers.

It could be this quarter or next but the the small producers and Fortescue are about to find themselves as the swing producers on the cost curve. Unless something in China changes quickly, crisis will envelope them sooner rather than later.