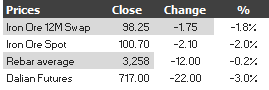

Here are the iron ore charts for May 16,2014:

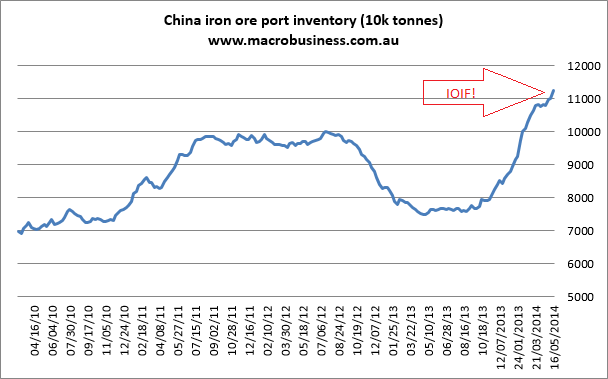

It’s all going to shit! Paper markets are in free fall with rebar futures also tanking. Physical markets are buggered as well with iron ore poised for double-figures and rebar average also about to break to a new low. Baltic Dry capesize fell 1%. The hilarious port pile grew another million tonnes or so last week to 112.5 million tonnes. I’ve made the acronym a little easier this week.

Steel continues to pour out in China. CISA’s fast data showed that in early May, average aggregate daily crude steel output of large and medium-sized steel enterprises in China totaled 1.824 million tonnes, up 1.6% from late April to another all time record.

From the FT:

“If Chinese steel production hadn’t been this high, the price would have fallen even more than it has,” said Colin Hamilton, head of commodities research at Macquarie. “At the moment people are holding enough iron ore for current production and future growth, but if expectations come down they’ll hold less iron ore and take less from the market.”

Last night Macquarie, one of the most accurate predictors of iron ore’s price over the past year, dramatically cut its estimate for the average price of the raw material for the third quarter to $100 a tonne, down from previous forecasts of about $115.

Falling steel prices are also putting pressure on Chinese steel mills.

“The steel sector is in a financial mess, with both private mills and state-owned enterprises struggling to generate positive cash flow. Credit is extremely tight,” wrote analysts from Credit Suisse in a report published this week. “Meanwhile, China’s domestic iron ore sector is now being savaged by lower-cost, abundant imports.”

The price of iron ore may be down but Chinese production isn’t, rising 12.3% from a year ago to 122.4 million tonnes and total output hitting 427.8 million tonnes in the first four months, up 8.7% year on year, despite a sluggish start to the year.

It’s just too tempting to point out that Mac Bank was bullish late last year and remained so until only a few weeks ago, despite the evidence pointed out at MB, so a pat on the back to ye auld humble blog is in order!

The news out of India would normally stabilise things but sentiment seems so bad that I doubt it this time. Stand by for more sell side capitulation as downgrades to equities must follow. Citi, JPM meet facial egg.