While Australia’s Reserve Bank continues to bury its head in the sand, the Bank of England (BoE) has joined the Reserve Bank of New Zealand in issuing stern warnings about risks building in the housing market, and is now looking to implement macro-prudential controls on mortgage lending.

In an interview with Sky News over the weekend (above), BoE governor, Mark Carney, expressed concerns about the “big debt overhang” building up across the UK economy, whereby homebuyers are taking on loans that are many times bigger than their annual salaries:

“We don’t want to build up another big debt overhang that is going to hurt individuals and is very much going to slow the economy in the medium term… We would be concerned if there were a rapid increase in high loan to value mortgages across the banks. We’ve seen that creeping up and it’s something we’re watching closely”.

Carney also noted that there is evidence that jumbo mortgages – those where loans are more than four times people’s salaries – are on the rise once more. He also warned that the UK housing market is the biggest threat to financial stability:

“The biggest risk to financial stability, and therefore to the durability of the expansion, those risks centre in the housing market and that’s why we are focused on that”.

He also noted the “deep, deep structural problems” arising from the UK’s dysfunctional housing supply system, which has for a long-time delivered a chronic under supply of homes and placed upward pressure on prices and facilitated extreme demand for mortgages:

“The issues around the housing market in the UK … is there are not sufficient houses built in the UK. (There are) half as many people in Canada as in the UK, (but) twice as many houses are built in Canada every year than in UK”…

And as noted in the UK Telegraph over the weekend, the BoE is mulling whether to impose macro-prudential limits on mortgage lending, such as capping mortgages to four-times incomes:

Mr Carney suggested that the Bank could impose a new “affordability test” for borrowers as well as reining in the Government’s controversial Help to Buy scheme which provides taxpayer-backed guarantees for homebuyers…

“We could do more, we could take steps around affordability to test whether or not individuals can test mortgages at much higher interest rates…

Mr Carney raised the prospect of people being stopped from taking our mortgages which were more than four and a half times times the size of their salary.

He said: “The level of higher loan to income mortgages, ones above four and a half, five times loan to income, potentially could store up bigger problems for the future.

Meanwhile, Deputy Prime Minister, Nick Clegg, has backed Carney’s assessment, seemingly endorsing winding-back the Government’s “Help-to-Buy” scheme and noting the chronic shortfall in housing construction:

“I think if (Mr Carney) says that we need to pare back some of the Government schemes, like Help to Buy, then I think we should do so.

He’s certainly right when he says the big long-term problem is we simply don’t build enough homes in this country, we haven’t done so for years, we’re making progress now but we need to do much more in the future.”

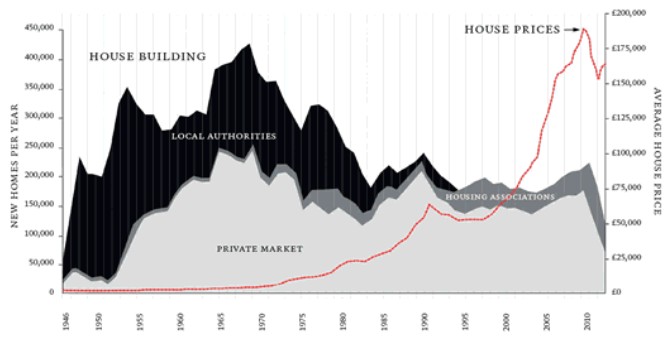

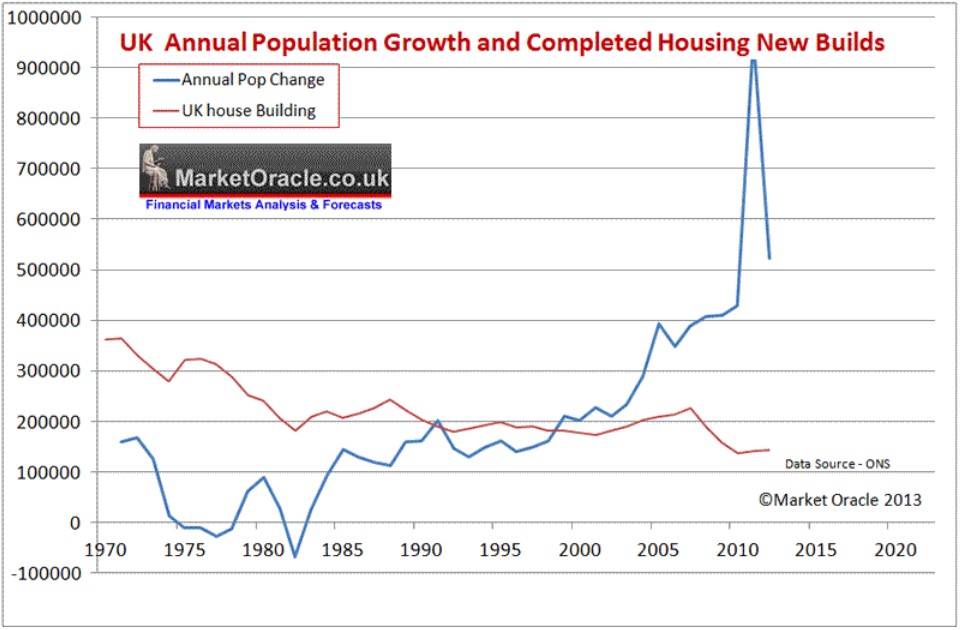

In additional to mulling macro-prudential controls on mortgage lending, it is encouraging to see both the central bank and government in the UK speaking-out against the structural impediments and supply-side constipation afflicting the UK housing market, which have meant that housing supply has been incapable of responding to rising demand, with the amount of new homes built in the UK crashing despite rising prices and high population growth (see below charts).

While the warning are certainly a case of ‘too little, too late’, at least authorities in the UK have begun the discussion, which is more than can be said for their Australian cousins, who remain largely silent on the issue of housing affordability and risks.

unconventionaleconomist@hotmail.com