Reuters has a piece today that’s stirring up some MSM fuss in implying iron ore could still crash owing to credit limits:

Commodities such as copper and rubber have been commonly used for financing, where traders or investors borrow against the commodity with the aim of investing the money in high-return areas such as real estate.

But Beijing’s credit tightening has spurred investors desperate for cash to turn to iron ore. Industry sources familiar with the practice estimate some 30 million tonnes or $US3.5 billion of stocks are now tied up by financing.

…”You cannot stockpile iron ore too long, otherwise the iron will be oxidised and the quality will go down,” said UOB-Kay Hian’s Lau.

Iron ore also takes up a lot of space at ports, which can increase charges if they want to move the cargo or to free up space, said a trader who had a cargo stored at a port for up to a year.

…Many Chinese banks have slashed lending to these sectors by up to 20 per cent, part of Beijing’s efforts to reform an economy that in three decades relied on cheap debt to expand at a double-digit pace.

Some traders say credit conditions are tightening even further, with some banks refusing to open letters of credit (LCs) to industries such as iron ore and coal.

A Shanghai-based trader who sells Asian cargoes to Chinese mills said a buyer was recently refused a letter of credit by a major Chinese state lender, but was able to get credit at another bank.

“Our bank in Hong Kong has been warning us that the future might come when Chinese banks will refuse to open a letter of credit,” he said.

Credit is a problem, yes. But the financing deals are secondary. So long as underlying demand holds up the port pile will clear. The primary credit-related risk is reserved for underlying demand and the likelihood that the reform process causes a growth undershoot in the next nine months.

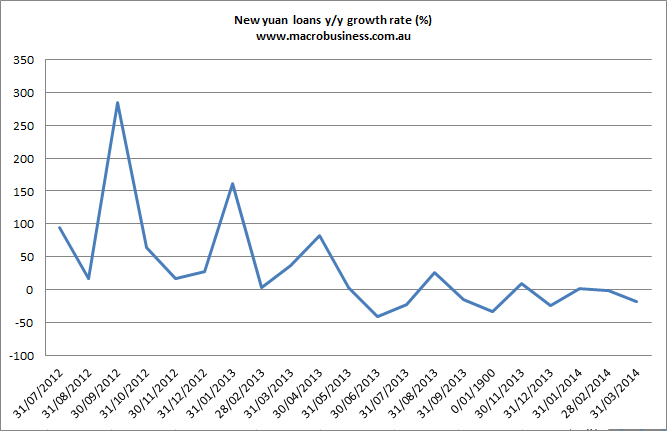

New yuan loans year on year growth is now consistently and materially negative:

That will weigh in growth, especially in the most credit sensitive and leveraged sectors such as property, shipbuilding, steel etc. That was the key point in an iron ore report by Westpac this week:

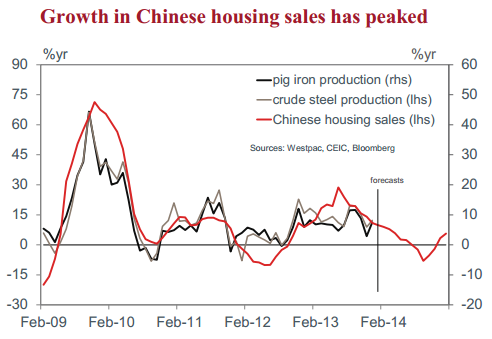

At the end of 2013 the pace of growth in Chinese output of pig iron and crude steel had slowed to around 7% to 8%yr; close to stalling speed for this industry. At the same time, our preferred leading indicators for Chinese steel demand, housing sales and total construction activity, continued to moderate.

Based on recent data and our observations of the administration’s policies, we believe that domestic activity will be even more of a drag on 2014 steel demand placing a weight on both crude steel production aniron ore prices.

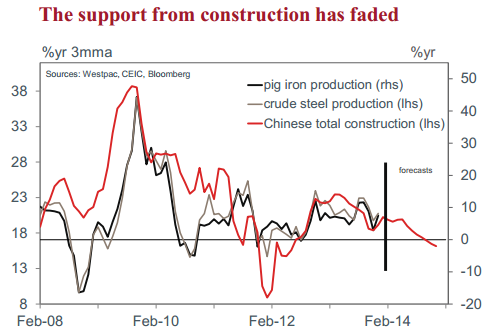

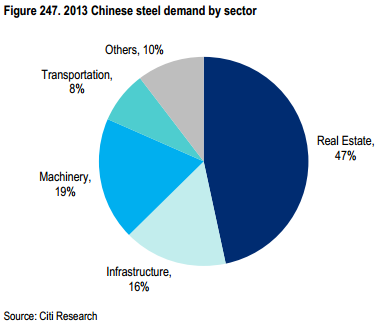

Westpac is right to watch building. It constitutes the lion’s share of demand. From another recent report, this time by Citi:

Some see it as smaller but you get the picture, building is the primary driver and it’s going to keep slowing, notwithstanding recent talk of “mini-stimulus”.

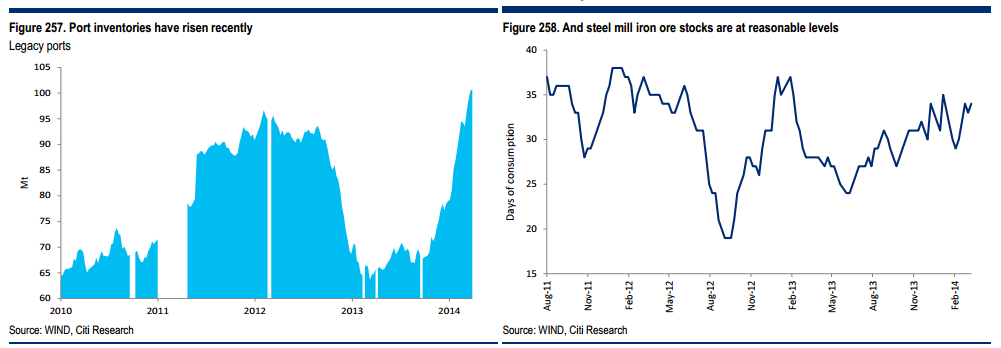

Citi is more constructive on Chinese growth in the second half, assuming more stimulus, but notes that total Chinese iron ore inventories at ports and mills are reasonable to high:

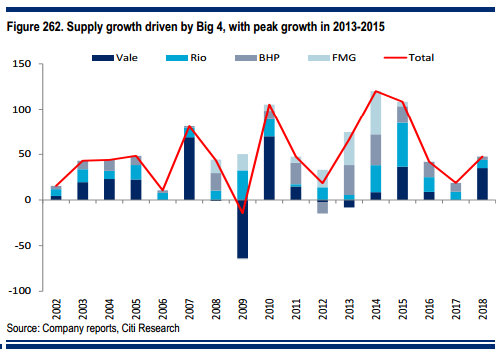

But it also notes that there is some offset in the fact that increased supply is front-end loaded this year:

However, the ramp up in supply from India and others continues all year and then all supply takes off again next year.

Funnily enough, despite Westpac being more bearish on growth, it reaches more bullish conclusions about the iron ore price, largely because it thinks Chinese domestic ore will be taken out:

Citi is considerably more price bearish:

I agree with the latter. In fact, if the Westpac forecast for weakening Chinese demand delivers – and today’s credit data supports it – then we’ll enter the third quarter seasonal Chinese steel mill destock with lousy demand and high inventories, setting ourselves up for a rerun of the 2012 iron ore price crash.

Irrespective of such a dramatic outcome, my bet is that the second half average price for iron ore will fall below that of the first half.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.