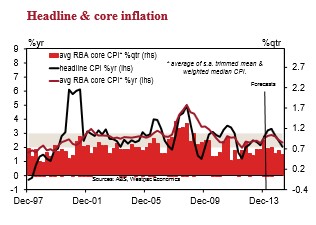

Westpac has released its March quarter consumer price index (CPI) forecasts, with the bank seeing inflation edging-up to a headline 0.9% QoQ/3.2% YoY (from 0.8% QoQ/ 2.7% YoY) and an underlying 0.7% QoQ/ 2.8% YoY (from 0.9% QoQ/ 2.6% YoY):

Our Q1 headline CPI forecast is 0.9%qtr/3.2%yr. Core inflation, as measured by the average of the trimmed mean and weighted median, is forecast to rise by 0.7%qtr/2.8%yr.

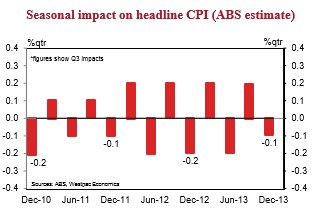

March is traditionally a seasonally strong month and has historically been worth about +0.2ppts on the CPI. We see this seasonality again this quarter which is part of the reason for the robust forecast.

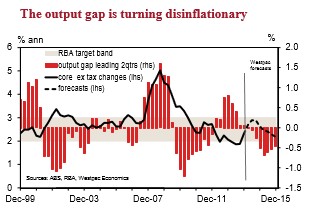

We estimate that the 6 month annualised pace of core inflation will lift from 3.0%yr in Q4 to 3.1%yr. The pulse of inflation is now around the top end of the RBA’s 2-3% target band but the lack of wage inflation, low inflation expectations and the ongoing widening of the output gap suggest the risks that this lift will become entrenched remain low.

Traded goods are forecast to rise 0.1%qtr/2.3%yr while non-traded goods are forecast to rise 1.2%qtr/3.6%yr.

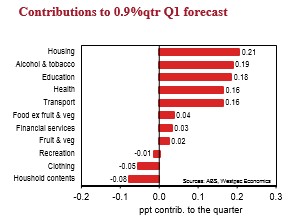

Housing has seen a key shift and while utilities inflation has moderated significantly, house purchase inflation has picked up again. Housing inflation tends to be key to the momentum in both core and non-tradable inflation.

The most direct impact from the weaker AUD, down 3%qtr against the USD in Q1, is seen in higher petrol prices which surveys suggest rose around 3.7%qtr. Car prices may be under some pressure too but the weaker yen would be helping as does the ABS’s hedonic pricing method. If a new model is the same price but has more features the ABS adjusts for this increase in quality with a fall in price.

Alcohol and tobacco make a healthy contribution to this quarter with an increase in the rate of tobacco excise being applied this quarter. Another key seasonal rise is pharmaceuticals as the PBS is reset and fewer households qualify for discounts. Education also rises at the start of the year and the 5.8%qtr is on par with 2013Q1.

Dry conditions extended into 2014Q1 and this boosted fruit prices again while vegetable prices did not fall as much as you might expect given the 7.1% jump in Q4.

Clothing normally does see some discounting in Q1, due to the post-Christmas sales, but given we still see some adjustment to the weaker AUD, we have allowed for just –1.3% compare to –3.9% in 2013Q1.

Domestic holidays have a seasonal bump in Q1, as confirmed by airfares data, but international holidays have a seasonal fall. We suspect the fall in international holiday prices will be less this year given the weaker AUD, hence our –0.2%qtr forecast for holiday travel compared to –1.8%qtr in 2013Q1.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.