Two commentators between them today sum up the state of housing, Australian rebalancing and monetary policy. The first is David Bassanese at the AFR:

The Reserve Bank has prematurely shifted the emphasis of its jawboning strategy from the exchange rate to house prices, with potentially disastrous consequences for the economy in the months ahead. With household and business confidence flagging again, the RBA needs to reshape its message and start focusing on the great “rebalancing” challenge still facing the economy.

After a bounce late last year, the Westpac-Melbourne Institute measure of consumer confidence had by April again slipped back below long-run average levels.

…We can’t afford to be complacent. If the housing market gets spooked too soon, and the $A remains high, there’s a risk that encouraging housing and exchange rate-led gains in business sentiment and hiring conditions will quickly unwind. A likely tough budget next month only adds challenges.

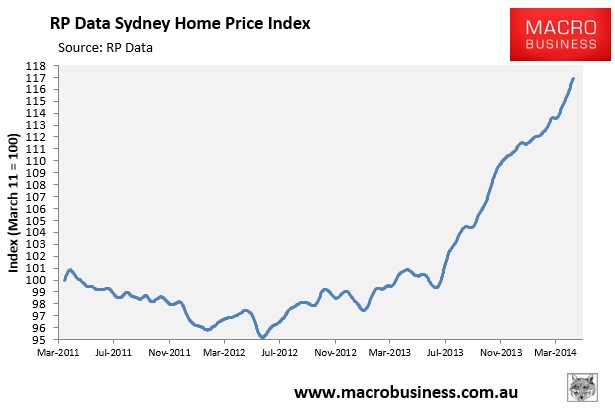

A quick look at Friday’s Sydney and national speculator numbers tell you that slowing asset prices are still some way distant:

As I illustrated last week, the RBA jawbone is pretty useless on housing anyway, until it pulls the trigger. So if Bassanese wants higher house prices he should call for more interest rate cuts.

But why he would want an even more conspicuous bubble is the question that Callam Pickering raises at Business Spectator:

…Speculation has driven the Sydney market into the stratosphere but also boosted Melbourne prices significantly. By comparison, cities without strong investor activity have experienced little price growth.

…The size of each downturn appears driven by three factors: size of the boom, how long the boom lasted and the interest rate environment.

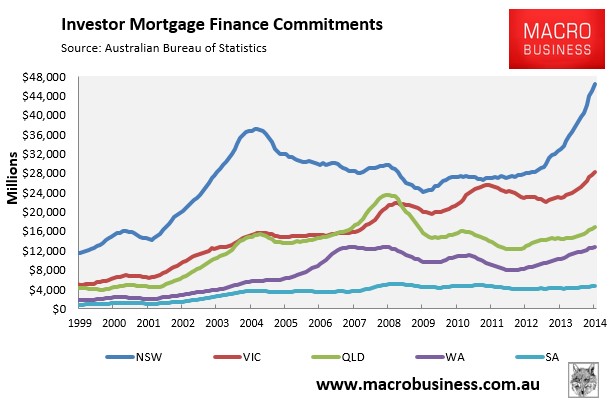

The current investment boom in New South Wales has lasted 26 months. By comparison, the boom in the early 2000s lasted for 37 months. But the current boom is rapidly approaching the dizzying heights of that earlier boom and, given the generous interest rate environment, there is a distinct possibility that the investor boom in Sydney could persist for another year.

In Victoria, the current boom has lasted 16 months and has obviously not been as frenzied thus far.

…Rarely has a boom in investor activity been centred on such a flimsy economy. The outlook for the Australian economy continues to be subdued, with investor sentiment completely out of whack with expectations for growth.

Furthermore, there is a very real possibility that investor demand may deteriorate just as mining investment collapses, providing a double-whammy for both households and the Australian economy.

Exactly right. Let’s not beat around the bush. That will mean a very nasty recession. But Bassanese’s (and the RBA’s) notion that the economy can levitate over the mining investment cliff enclosed in a protective housing bubble is even less reassuring. Another 18 months of current house price growth and the bubble will be enormous, yet we’ll only be halfway down the capex cliff.

The RBA is either heedless or reckless. Take your pick.