The Australian has published new research by the Canberra University’s National Institute for Social and Economic Modelling (NISEM), which sows that Australian wages rose by only 0.1% over the December quarter versus a 0.7% rise in living costs, meaning that real wages and living standards are going backwards. And NISEM sees no immediate relief in sight:

AVERAGE living standards fell in the December quarter and the outlook for households is now weaker than at any time since the Hawke government in the 1980s…

NATSEM principal research fellow Ben Phillips said the net 0.6 per cent fall in the December quarter meant living standards had now dropped for three of the past five quarters. The only increases, in the middle of last year, were the result of interest rate cuts rather than wage growth…

Mr Phillips said prices for principal exports would not pay for further income growth, while there was no potential for income tax cuts, little scope for interest rate reductions and the jobs market was weak.

“It is hard to be bullish on household standards of living in the short term”, he said.

I am not surprised at all by this result.

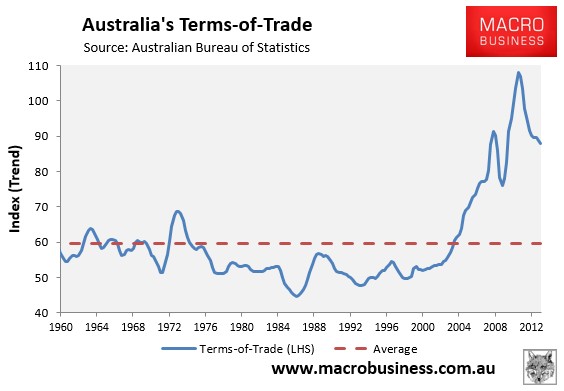

The fact is, national income is now being dragged-down by falling commodity prices and the terms-of-trade, which is retracing after rising to its highest level in the nation’s history in 2011 (see next chart).

As commodity prices and the terms-of-trade retraces, Australia’s pay is essentially cut, since it can now buy less imports from a given level of exports.

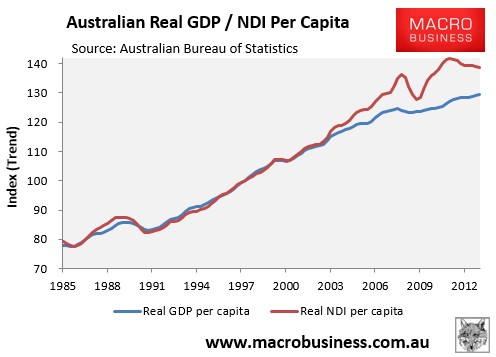

These dynamics can be seen in the below chart, which shows NDI growing at a much faster rate than GDP between 2003 and 2011, but starting to converge back towards GDP ever since as incomes have retraced (see next chart).

Given that Australia’s terms-of-trade remains highly elevated on an historical basis, it’s a fair guess that it has a lot further to fall, meaning that NDI growth will at best remain anaemic.

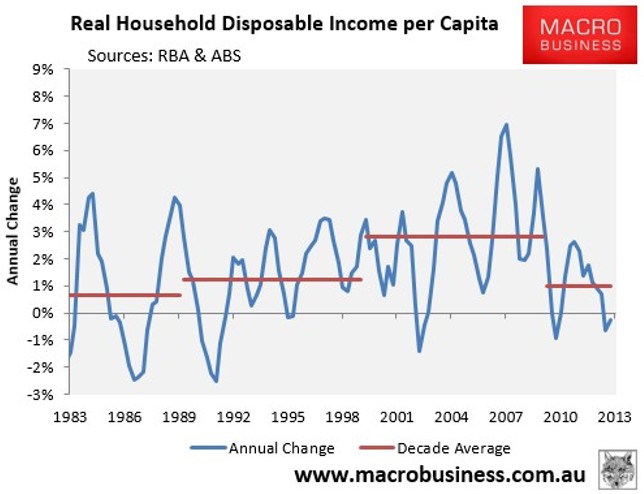

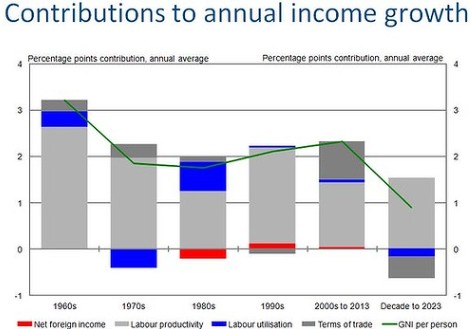

The falling terms-of-trade’s impact on household income (rather than NDI) is illustrated clearly in the next chart, which plots the annual growth rates in per capita household incomes and the average growth rates for each decade:

As you can see, between 2010 and 2013, real per capita household income growth has averaged just 1.0%, the lowest rate of growth since the 1980s.

Indeed, late last year, the Australian Treasury forecast that average per capita income growth would halve over the next decade to the lowest rate of growth experienced in 50 years, weighed down by the falling terms-of-trade (see next chart).

To the extent that commodity prices and the terms-of-trade continue to retrace back towards their longer-term average levels, it will detract from household income growth. And with it, much of the income gains enjoyed over the 2000s will be unwound.

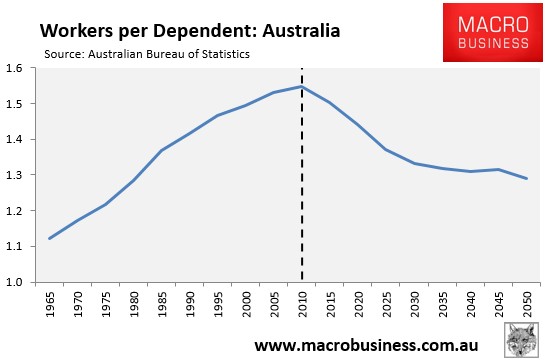

The second major structural headwind for incomes is Australia’s ageing population. The withdrawal of the large baby boomer cohort from the workforce will result in a rising dependency ratio and a falling share of workers supporting non-workers (see next chart).

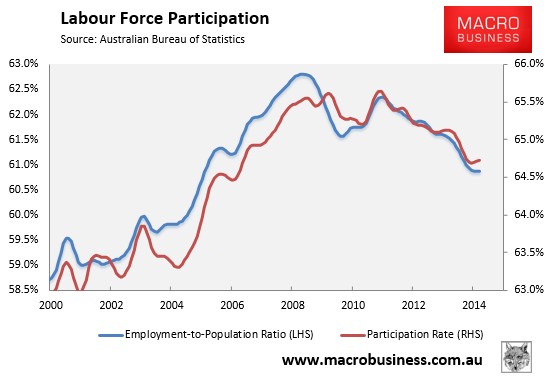

In turn, the labour force participation rate and the employment-to-population ratio is likely to continue trending lower (see next chart), lowering growth in both GDP and national income.

These are two of the major structural headwinds facing the Australian economy, are are the key reasons why real Australian income growth and material living standards are unlikely to experience much improvement in the years ahead.