It seems most groups have resigned themselves to the fact that there will be cutbacks to the Aged Pension in this year’s Budget. Instead of opposing reform outright, focus appears to have shifted to ensuring that cuts are targeted at wealthier retirees. From The Australian:

WELFARE groups have called on Tony Abbott to target asset-rich retirees and raise the age for access to superannuation rather than cut pension entitlements for low-income earners…

The expenditure review committee is also examining income and assets tests for the pension as its members seek to make the benefit “sustainable’’ into the future with an ageing population…

Australian Council of Social Service chief executive Cassandra Goldie urged the government to tighten access to the aged pension for retirees with significant assets and increase the preservation age of superannuation rather than introduce changes that resulted in savings being made from those on the lowest incomes…

I lean towards this approach. The main problem with Australia’s retirement system is that it allows too many well-off retirees with substantial assets to receive taxpayer support.

While there are no doubt many genuine pensioners scraping by on $20,000 a year, according to the Grattan Institute, 80% of Australian families over the age 65 with about $1 million in assets get the pension or another welfare benefit.

Means testing has become so lax that over 70% over the mature aged population passes the test and receives at least a part pension, as noted by Peter Martin today:

Included are couples earning $70,000 (untaxed if it’s from super) with up to $1.1 million in assets, plus their “family home” which they are allowed to expand or upgrade knowing it won’t be caught in the assets test.

Anyone who fails this test is by definition well off. But the well off aren’t left out. About half of them get the seniors supplement and Commonwealth health card, which entitles them to cheaper prescriptions. There’s no assets test, millionaires can get it. There is an income test, but it comes with a hole. Singles with more than $50,000 and couples with more than $80,000 in taxable income can’t get the card. But income from superannuation isn’t taxable, so it isn’t counted. It is possible to receive $200,000 a year from super (plus $50,000 in other income) and still get the card. Almost certainly an unintended consequence, it makes a joke of the tight rules that apply to younger Australians who actually need help.

For the sake of equity and Budget sustainability, assistance to wealthy retirees must be cut-back, so that benefits only flow to those genuinely in need.

That’s not to say that changes should not also be made to indexing arrangements, to ensure that Aged Pension does not continue to rise faster than the rate of inflation. As also illustrated by Peter Martin today, in the 4 1/2 years since the former Labor Government implemented the special age pensioner cost of living index, age pensioner cost index of living has risen 14%, whereas the pension itself has climbed 25%. Meanwhile, those on Newstart have received CPI increases, which rose by only 13% over the same time period:

The automatic [pension] increases are the envy of less-fortunate Australians on Newstart, Youth Allowance, Austudy and many on wages.

The full pension package now amounts to $21,900 for a single, and $33,000 for a couple.

Once in the ballpark, the Newstart unemployment allowance languishes at an impossibly low $13,300.

That said, it is simply not enough to only focus on the overly generous nature of the Aged Pension. Just as bigger lurks lie with superannuation, although politicians and the media are largely quiet on this issue.

While the superannuation system was originally designed so that a younger generation could pay for its own retirement, it has instead become a mechanism whereby older people pay less tax given their income than everybody else, with the lion’s share of benefits also overwhelmingly going to richer people.

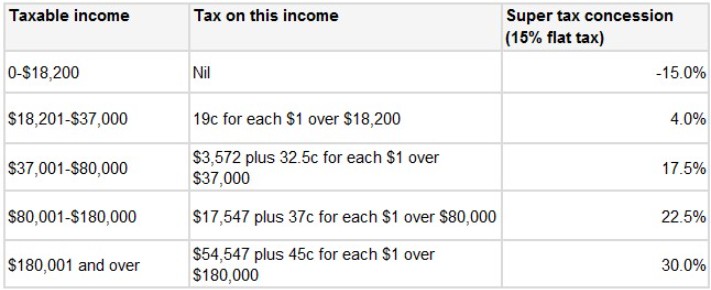

Under the current system, all employees that contribute compulsorily into super pay a flat 15% contributions tax, which effectively means that the amount of concessions received increases as one moves up the income scale (See below table).

For example, someone that earns in excess of $180,000 per year receives a 30% tax concession for each dollar that they contribute into super (i.e. 45% marginal tax rate less the 15% flat tax). At the other end of the scale, someone that earns less than $18,200 per year in effect gets penalised 15% for each dollar that they contribute into super.

According to the Australian Treasury, concessions on superannuation contributions were estimated at $16.5 billion in 2012-13, with concessions on superannuation earnings valued at $15.5 billion. Moreover, the Treasury estimated that the top 5% of contributors would receive 20.3% of contribution concessions, with higher income earners also receiving the lion’s share of the earnings tax concessions.

Clearly, superannuation concessions also need to be pulled back from higher income earners, in order to improve the integrity, fairness and sustainability of the entire retirement system.

unconventionaleconomist@hotmail.com