March has delivered another record month of production. The solid print for March was predominantly driven by: (1) FMG’s ramp up of Kings to 40mtpa; (2) ongoing optimization of BHP’s inner harbour and ramp up of Jimblebar; and assisted by (3) increased use of larger vessels; and the (4) absence of weather-related interruptions (c.f. 1.2 day March average).

Top down vs bottom up – Forecasts in line

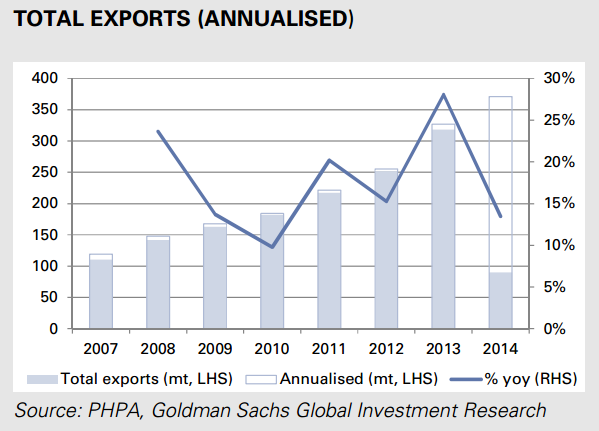

For the major users of this port, BHP Billiton (BHP.AX), Fortescue Metals (FMG.AX), and Atlas Iron (AGO.AX), it provides a good barometer of iron ore export activity. For the quarter to 31 March, total exports were up 35% to 90.4mt. This supports our bottom up estimate of 91mt derived from our individual production forecasts for BHP (53.4mt), FMG (34.5mt), and/or AGO (2.7mt).

Annualised capacity for the quarter was 362mtpa (including 413mtpa in March), however it will need to lift to above 450mtpa to accommodate the miners’ proposed growth plans. That said, we remain of the view that it could theoretically accommodate 640mtpa. (refer “Port Hedland: Unleashing the inner harbour 2; we see upside for BHP (Buy)” December 10, 2013).

Iron ore outlook underpins ratings: BHP (Buy), FMG (Sell)

No change to our ratings or target prices ahead of quarterly production results late this month: BHP (Buy; A$37.75) 3Q14 – 16 April; FMG (Sell; A$5.45) 3Q14 – 17 April; AGO (Neutral; A$0.98) 3Q14 – 24 April.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.