Iron ore has a habit of making a goose out of analysts. It happened to me early last year when India pulled the pin and saved the market. It happened to UBS later in the year when a forecast crash turned into a price spike. And it’s happening right now to Mac Bank’s excellent Graeme Train. Here is his confession:

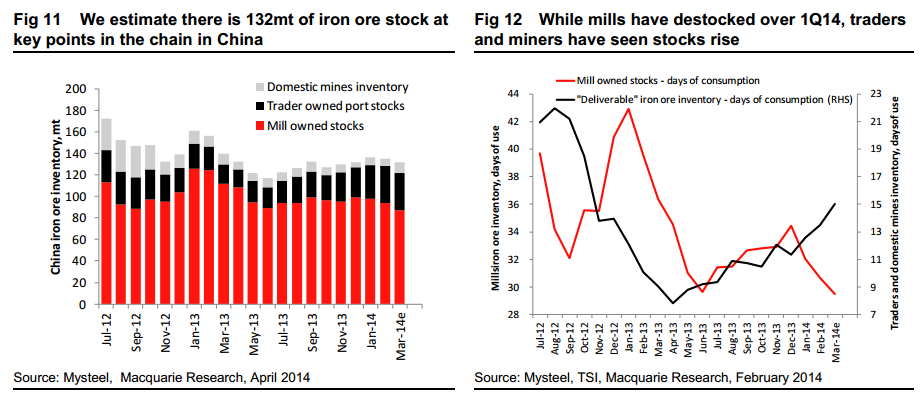

Combining the three sets of inventory data we can attempt a much more complete assessment of iron ore inventory in China. On our numbers, there was a total of 132mt of stock at these key points in the chain by the end of March, equivalent to ~45 days of consumption.

What also becomes apparent is that the destocking over 1Q14 has been somewhat different to what we saw over 1H13 – last year, we saw destocking at every point in the chain until May, when traders started to restock. This year, however, although the mills have destocked, their destocking has been almost entirely offset by the rise in inventory at mines and traders (this is shown in fig 12 below, where the range of each axis is the same, although the absolute level is different).

This time around, the circumstances are different – with “deliverable” inventory (that held by traders and miners) higher, there would appear to be less potential for a squeeze in prices. However, as we saw at the end of 2012, a transfer of stocks from the traders and miners to the mills can still result in upward pressure on prices. Unlike 2H13, we are expecting steel production to increase over the coming months, so purchasing activity by the mills should be bolstered by both restocking and rising real demand. In addition, we are not expecting as much of a sequential increase in 2Q iron ore supply as we had previously, given that minimal seaborne supply disruptions over 1Q mean more material has stayed in the market.

In conclusion, a more holistic approach to assessing iron ore inventory should help cut through the noise that arises from trying to manage multiple sets of overlapping data. In our view, the results of this analysis support our view that bearish interpretations of the port stock data so far this year are overdone (overall inventory on our numbers is around 40mt lower than the last time port stocks were at similar levels to now, back in 2012). However, we also concede that we had perhaps been too focussed on mill inventory and overly dismissive of inventory at other points in the chain. Our view that iron ore prices should rise in 2Q on the back of mill restocking hasn’t changed (this has already started to play out), but the risk of a squeeze pushing prices significantly higher is perhaps lower than we had previously thought, and our view is now more dependent on a rise in steel production than it had been previously.

The only issue I have with this analysis is that the data is one month old and mills have been pretty clearly restocking over that period so the balance is likely to have tilted further towards over supply.

Anyway, like all markets, iron ore is tough to forecast and I’ll happily conceded that Mr Train has done a better job than most.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.