From JP Morgan offers an impressive piece of analysis today:

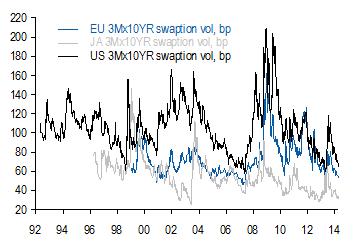

Alongside the ballistic rally in high-yield currencies since early February, volatility in most asset classes is collapsing. Rate vol is within 6bp of its all-time lows in the US, Europe and Japan (chart 1), while G10 FX vol and EM FX vol are within 1 point and 2 points, respectively, of their record lows (chart 2). Many explanations have been offered for these moves, all minor individually but perhaps more meaningful collectively. These include: China’s mini-stimulus floors commodity prices; an up-move in US labour participation validates the Fed’s patience on rate normalisation; the Bank of Japan should expand its balance sheet again this summer; the ECB might launch QE eventually; and investor impatience with negative-carry positions in rates and FX is considerable.

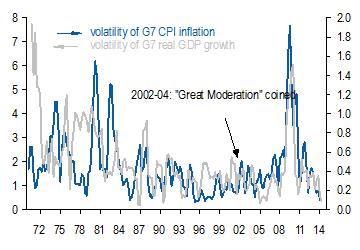

Maybe a less obvious, underlying explanation is that the Great Moderation is back. That term was coined over a decade ago to describe the apparent, trend decline in the volatility of global growth and inflation (chart 3). Since the range of possible scenarios on the global economy and monetary/fiscal policy influences the range of outcomes for asset prices, record low business cycle volatility should correlate with record low asset price volatility. That seemed a convincing theory until 2007, when the subprime crisis and then the EMU Crisis highlighted that the Great Moderation was a bit of an chimera which ignored unsustainable imbalances in the US and Europe.

Every 1% increase in global GDP growth lowers FX vol by about 0.5 points; every 1% rise in the vol of GDP raises FX vol by 0.7 points; and every 1% rise in inflation volatility raises FX vol by 1 point. The fit is similar over shorter samples like 15, 10 and 5 years, though the coefficient on inflation is higher. This results suggests that tame inflation has accounted for the bulk of FX vols’ decline over the past few years, perhaps because low inflation has motivated substantial central banks balance sheet expansion which indirectly suppresses FX vol by directly suppressing rate vol.

…Is it sensible to buy into the idea of Great Moderation 2.0? Not based on vol valuations, which are already rich even for this unusually stable global macro environment. The only argument for owning FX carry is that it has underperformed other risky markets so significantly over the past two years due to weak business cycles in the majority of the high-yielders which populate these baskets (Australia, Norway, Brazil, India, Indonesia, Turkey). Thus the strategy is somewhat cheap relative to other risky markets as and when business cycles bottom in any of these countries. This view assumes that macro vol remains contained.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.