Here’s a timely report by Goldman Sachs supporting my spray at iron ore delusion this morning:

Time to digest an investment binge in excess of US$2 trillion

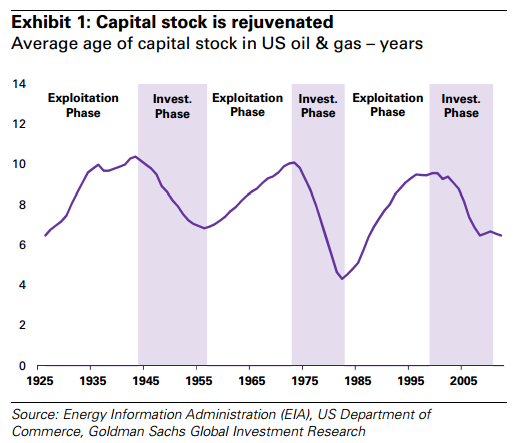

We have long argued that commodity supply cycles can be divided into investment and exploitation phases that create a full 20-30 year supply cycle. In the decade to 2012, commodity markets were in an investment phase, characterized by rising prices and, more importantly, attractive returns for producers that induced investment in new capacity, which eventually overwhelmed demand growth and created an exploitation phase, where the market ‘exploits’ the existing capacity.

Over this time period, the value of the capital stock in the mining and energy sectors increased by US$1.4 trillion in just six countries, including the US and China; once other regions are included, we believe the total increase is well over US$2 trillion.

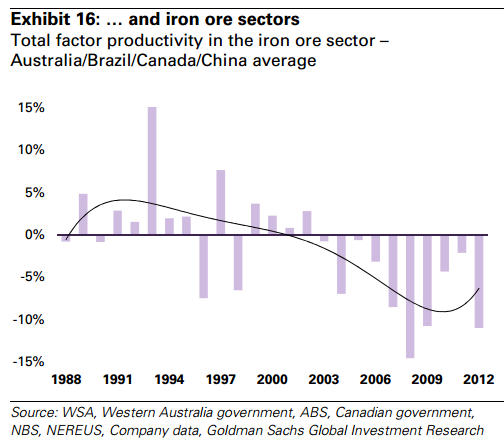

However, the rapid increase in spending decreased capital and labour productivity by as much as 45% over this time period. As the market outlook deteriorates and many markets move into surplus, margins will likely compress, forcing producers to shift their focus away from investing and towards improved operating performance, diversification and capital discipline to reverse the decline in productivity, which will become increasingly important in delivering shareholder value.

Composition of investment returns will likely shift but total returns should not be materially affected

For commodity-equity investors, the cost reduction achieved through improved productivity can be passed on to investors to maintain returns. For direct-commodity investors, the resulting hedging by producers to manage risk will likely create backwardated forward curves that will yield a positive carry or pay a ‘commodity dividend’ that will likely offset the lack of commodity price appreciation or even outright price declines, keeping total commodity returns relatively constant across the supply cycle. In other words, we believe commodity investors will likely be paid equity-like returns for providing commodity producers risk capital to help navigate the more competitive environment of the exploitation phase via more efficient deployment of both capital and labour even as prices and margins decline.

No doubt the returns from majors will remain constant over the “exploitation phase” but not before the big price shakeouts end.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.