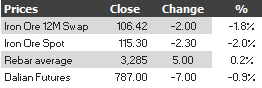

Here are the iron ore charts for April 2, 2014:

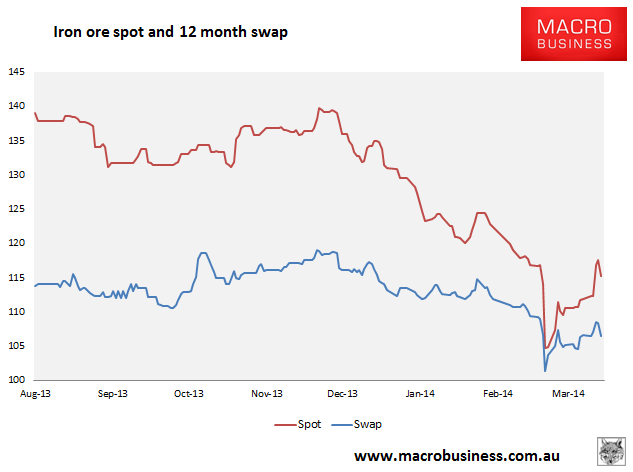

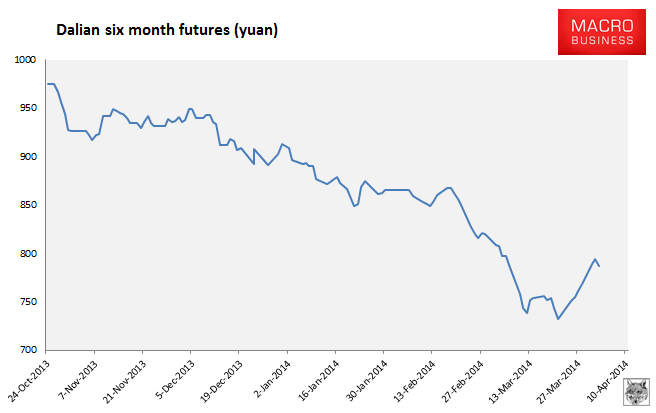

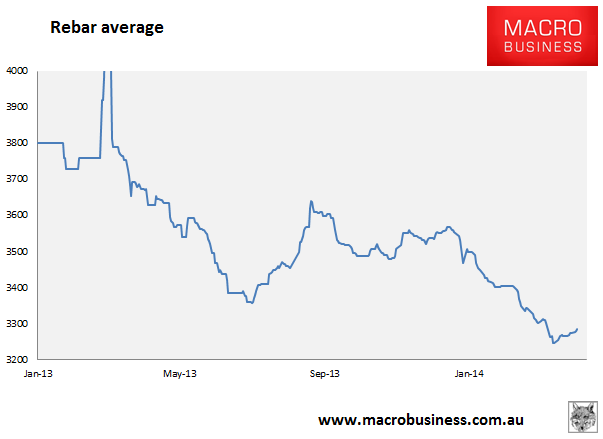

Paper markets were weak across the board with rebar futures also falling some. Physical markets saw spot fall sharply but steel firm up a little. Baltic capesize fell another 3%.

Whether this is the pause that refreshes or a return to slump is difficult to tell. My guess would be a balance of influences. The run in ore is far ahead of steel prices, the stimulus announcement looks luke warm and credit will remain tight but Pilbara strike action is still a possibility. From the ABC:

Negotiations will resume next week in an attempt to resolve a pay dispute between tug boat workers and a shipping company at the world’s largest bulk export port in Western Australia’s Pilbara.

The Fair Work Commission is mediating discussions between Canadian contractor, Teekay Shipping, and the Maritime Union of Australian (MUA) over a workplace deal for deckhands.

Tug boats play a vital role in operations at Port Hedland’s port, which is the export base for a number of iron ore miners including BHP Billiton, FMG and Atlas Iron.

The MUA says its Port Hedland members have indicated their willingness to strike and the union has been given permission to hold a ballot on strike action.

However, MUA WA branch secretary Chris Cain says that is not the union’s preferred outcome.

“The position with Teekay is that they want the best professional people they can get and we’re saying quite clearly we can deliver that.

“There has never been a stoppage in Port Hedland or any type of strike action and we’re trying to avoid that if we possibly can.”

While negotiations between the parties are confidential, Mr Cain said the MUA was seeking clarity on job security, rosters, work hours and pay for its members.

“Bear in mind, this is the biggest port in Australia, the most profitable port in Australia,” he said.

“My members deserve a decent wage in there for the hours of work that they do and the rosters that they do.

“I don’t think the pay is anything out of the ordinary for the north-west.”

The miners shouldn’t complain too much. A timely threat of supply disruption has already helped raise iron ore prices some 5%, so long as it doesn’t actually happen it can be gamed nicely.

The bigger picture remains troubled for prices beyond a short horizon. From Bloomie:

The Chinese steel industry’s ability to survive 1 billion yuan ($161 million) of losses per month without more defaults is under threat as a slump in iron ore and the yuan undermines a key source of financing.

The currency has weakened 2.5 percent this year and a measure of exchange-rate swings reached a record, prompting Goldman Sachs Group Inc. to predict funding that uses the steelmaking ingredient as collateral will drop over the next two years due to foreign-exchange hedging costs. Iron ore prices fell 11 percent in the past five months as cash shortages at closely held mills prompted what Morgan Stanley says is panic selling.

…“Private steelmakers will see very significant operational problems and funding issues this year, so we could see another default,” Sangyun Han, a Hong Kong-based credit analyst at Standard & Poor’s Ratings Services, said in a phone interview yesterday. “Higher volatility of the currency is another negative factor in their financing in addition to volatile iron ore prices and weak demand.”

…“Most of the iron ore financing deals are in dollars because of lower costs,” said Roger Yuan, a Hong Kong-based commodity analyst at Goldman Sachs. “While some steelmakers have been using iron ore financing deals to improve their working capital as they need the raw material for production anyway, the biggest problem still lies in their operations. That’s big supply and shrinking demand.”

…“Small- and medium-sized steelmakers are not making money in steel production, and I’m not expecting any potential recovery,” said S&P’s Han. “There is some political pressure in lending to the steelmakers out of environmental concerns.”

…“Some steel mills have been relying on iron ore financing for cheap funding as bank loans are already expensive and difficult to get,” said Huang Huiwen, a Shanghai-based steel industry analyst at Shanghai CIFCO Futures Co. “The policy trend is to tighten credit to the industry, hoping to alleviate overcapacity, and control pollution and energy consumption.”

…Some steelmakers will be forced out of the market within the next three years, Dai Zhihao, general manager of Baoshan Iron & Steel Co., said in an online chat with investors on March 31. The whole industry will continue to see little profit, he added.

“Iron ore financing provided cheap loans to steelmakers, so if it becomes more difficult, then their cashflows could worsen in the second half,” Shanghai CIFCO’s Huang said. “I’m not optimistic about the industry’s outlook.”

If we see further steel mill defaults (and it seems likely we will, perhaps many) it will trigger further gapping in iron ore prices as markets expect a combination of tightening finance for other mills and liquidating iron ore inventories at ports.