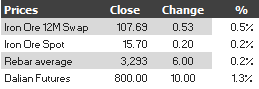

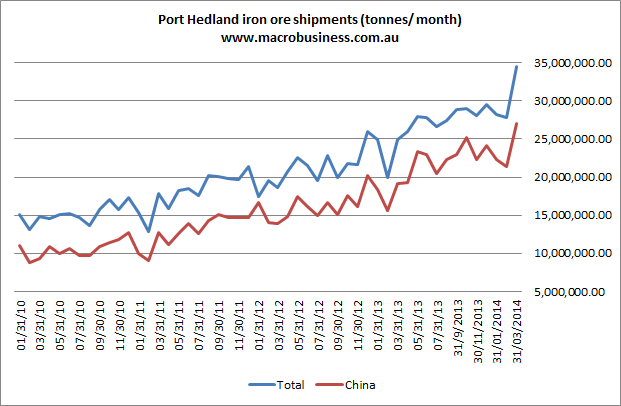

Here are the iron ore charts for April 4, 2014;

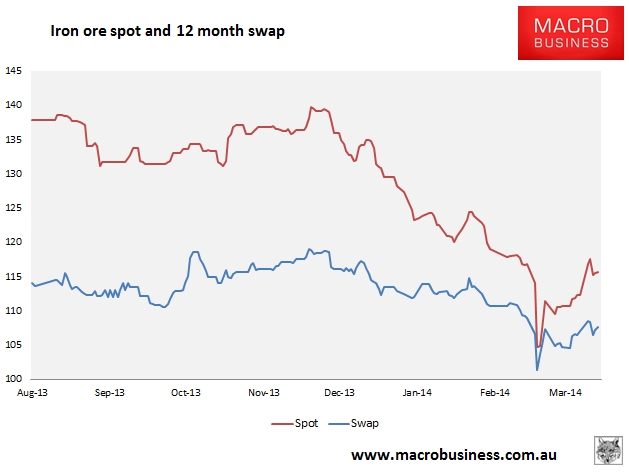

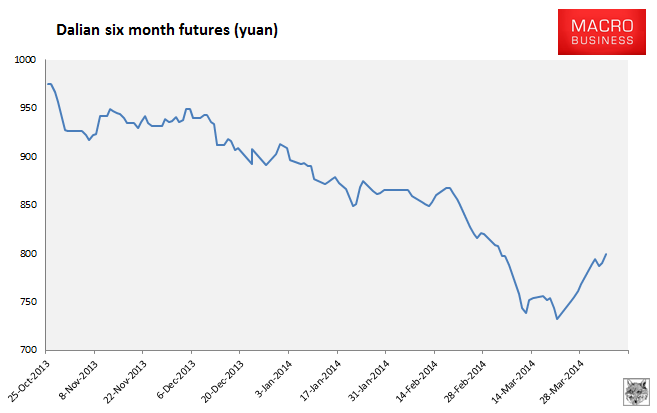

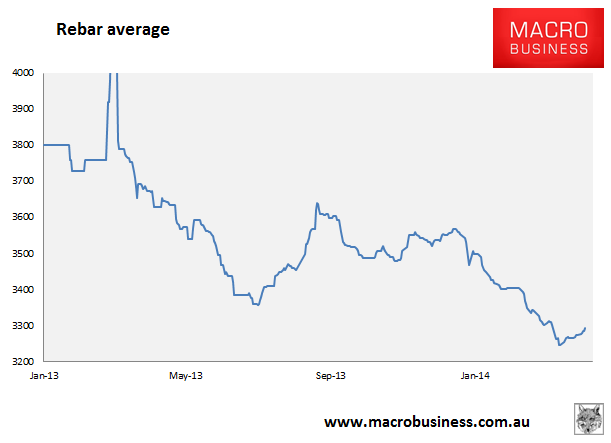

It was a good day on Friday for iron ore. Paper markets were firm with Dalian leading and rebar futures up as well. In physical markets, rebar average continues its muted recovery, hinting at some underlying demand. Iron ore spot is stalled but well off its low. Upsetting the party, the Baltic Dry capesize component fell another 1.5%.

The big news, however, is the late Friday release of this baby:

Port Hedland shipping volume figures for March were insane, up 38% year on year, 24% month on month, with China’s largest ever month by 7%. Korea and Japan also had blowout months, accounting for the madness.

What do we make of this? First, large volume gains are expected given the BHP and FMG capacity ramp ups (RIO ships from Cape Lambert). It is also not that unexpected given the Baltic Day capesize component had a good (though not great) March.

We might also see evidence here that Chinese iron ore mines have struggled to re-open after winter with prices in the doldrums.

What is surprising is that this kind of jump is possible without a vociferous steel mill restock and soaring spot price. Port stocks have been rising, obviously, but not enough to account for such volume gains. Mills have clearly raised inventories in some measure in the past month. We’ll get an update on how much this week, but these figures suggest that there’s been more buying activity than it appears and prices haven’t launched because demand has been met with a tsunami of supply.

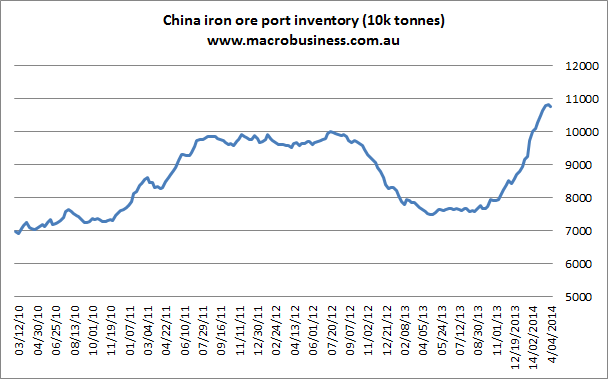

That thesis is born out by port stocks on the week, which finally peaked and fell slightly:

So, it’s a mixed story. Mills are very likely restocking but supply is preventing any return to higher prices (had this happened last year we’d be $20 higher). I do not expect a full restocking episode given the apparent slack in the steel market and disappointing stimulus so in the medium term it means higher mill stocks which, combined with the port pile, will see prices reverse steeply at some point.

Yet the volume gains are so extreme for now that major iron ore equities are probably going to bull-up.