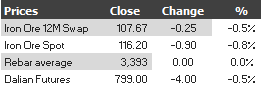

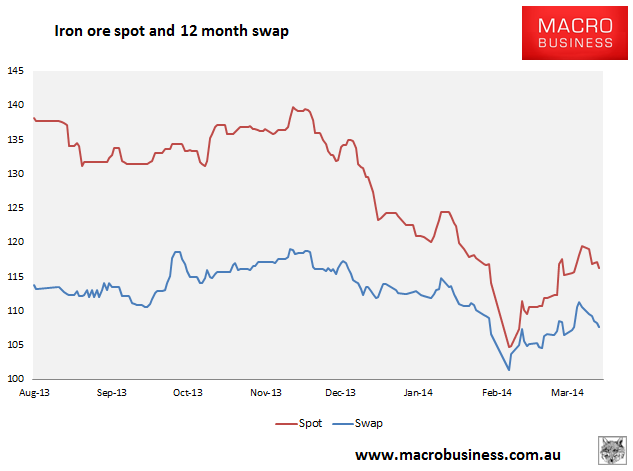

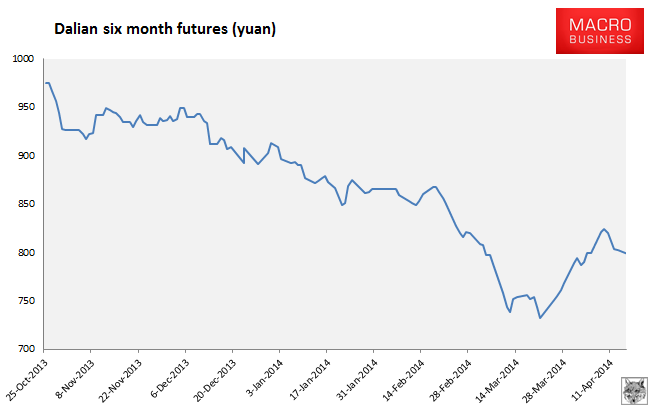

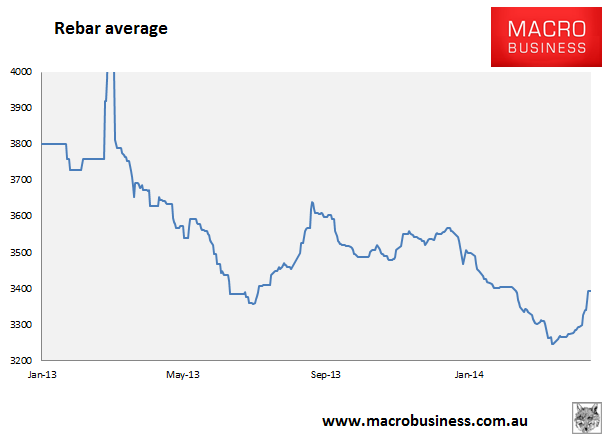

Here are the iron ore charts for April 16, 2014:

And so the paper market weakness rolls on. None of these charts look especially comforting and may all be forming head and shoulders top patterns. Rebar futures fell sharply too. In physical it’s increasingly as bad with the rebar recovering stalling and the Baltic Dry capezise component crashing 6.5%.

Basically, the restock is over, supply is abundant, demand mediocre and the prospects of greater stimulus slim. Not a very nice combination.

I will draw attention to the last few days of major iron ore miner production reports and make the point that both RIO and FMG reported serious under-performance versus nameplate capacity in Q1 (with BHP out-performing slightly). Roughly speaking the RIO and FMG ramp up of new supply was a combined 50 million tonnes per annum short of expectations and that supply is now rushing to market to meet volume targets.

As such, reports are already circulating of discounting for contract customers. From Platts:

Fortescue Metals Group, Australia’s third-largest iron ore miner, has offered deeper discounts to its major contractual customers for May-loading cargoes of its main products compared with April, some customers said.

The miner sold its flagship product of 56.4%-Fe Super Special Fines at a 7.5% discount to contractual customers for May, compared with 6.5% for April, sources said.

For its 58.3%-Fe Fortescue Blend fines, FMG set its May discount at 4.5%, according to several customers, from 3.5% settled for April.

…Customers said the miner raised the discounts to entice demand, given significant pressure on spot prices of FMG material amid abundant supply.

…Traders said reselling Super Special and FB fines cargoes on the spot market was proving challenging because of the abundant supply, and they have had to offer additional flat price discounts on top of FMG’s monthly discount rates.

A Shanghai-based source at a state-owned trading house said previously that it was difficult to persuade customers to buy more Super Special fines even with FMG’s increased discount levels every month.

“We see pretty consistent demand for [57.6%-Fe] Yandi fines, and they’re popular with mills, but for Super Special fines, it’s really hard to move volumes on the spot market.”

…A Hong Kong-based trader added that he was “avoiding” buying FMG cargoes lately because they were proving “so hard to sell despite the higher discount levels.”

Playing this out for the year ahead, then, mills are entering peak seasonal demand on rebounding construction and that will run through July but it’s going to coincide with the major miners rush to market so there is very little chance of any restocking and a pretty decent chance to a return to destocking given still weak steel prices.

But, as a base case, let’s say steel prices recover enough that mills maintain inventories but there is still a slow bleed in prices as buyers pick and choose and the port pile overhangs everything. Assuming that transpires, we arrive at the juncture of Q3 seasonal weakness with high inventories, still average demand, already low prices and abundant supply. Mills destock into September and that pushes prices to record post-GFC lows around $80 or below if China persists in its reform and real estate demand does not pick up.

The great iron ore glut is upon us, peeps, and it’s not outrageous to suggest that the peak iron ore price for 2014 is already past.