The AFR has posted an interesting article this afternoon citing survey results of 10,000 Australians showing that most people wish to retire at just 57 years old:

When recruitment firm Ranstad asked nearly 10,000 people about their ideal retirement age, most said 57, and fewer than a third said they were happy to work past the age of 62…

As the population ages, there are fewer working-age people to support the growing ranks of elderly who require health services and aged care…

The age pension cost $36 billion last financial year. The allowance provides up to $29,463 a year per couple and was paid to 2.3 million people in 2012.

As the cost burden grows, eligibility for the pension is coming under scrutiny.

The survey follows the release in December 2013 of the Australian Bureau of Statistics (ABS) Retirement and Retirement Intentions Survey for July 2012 to 2013, which also suggested that Australians are refusing to work longer.

According to the ABS, the average age at retirement for recent retirees, that is, people who retired less than five years ago, was 61.5 years – virtually unchanged from the last survey from July 2010 to June 2011. Moreover, the average intended age at retirement was just 63.4 years of age – below the current official retirement age of 65. Again, this was virtually unchanged on the July 2010 to June 2011 survey.

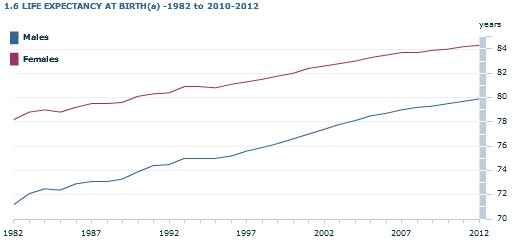

At the same time, data also released by the ABS showed that life expectancy continues to rise, whereby a 65 year-old male could expect to live for a further 19 years and females a further 22 years (see next chart).

To add insult to injury, the ABS also found that more than half of all retirees withdraw their super as a lump sum, with many then blowing the windfall on their homes or a new car:

Of the 3.3 million people aged 45 years or over who were retired from the labour force, 2.0 million (61%) had made contributions to a superannuation scheme. Men were more likely to have made contributions to a superannuation scheme than women. Just under three quarters (72%) of retired men aged 45 years and over had contributed compared to 52% of women…

Of those who had made contributions, 55% had received all or part of their superannuation funds as a lump sum payment (54% of men and 57% of women). Many of those who received a lump sum payment used it to pay off or improve their existing home or purchase a new home (32% of men and 31% of women) or to buy or pay off a motor vehicle (14% of men and 11% of women).

Meanwhile, the reliance on the aged pension increases the longer someone is retired, suggesting that superannuation is failing in its objective of replacing the aged pension:

For many people, their main source of personal income in 2012–13 at the time of the survey, changed from that at the beginning of their retirement with more people becoming reliant on a ‘government pension/allowance’. While 1.5 million (46%) of those aged 45 years and over who had retired reported that a ‘government pension/allowance’ was their main source of personal income at retirement, almost 2.2 million (66% of all those who were retired) indicated that this was now their main source of current personal income. This represents an increase of 45% compared with the number of people who stated that it was their main source of personal income at retirement.

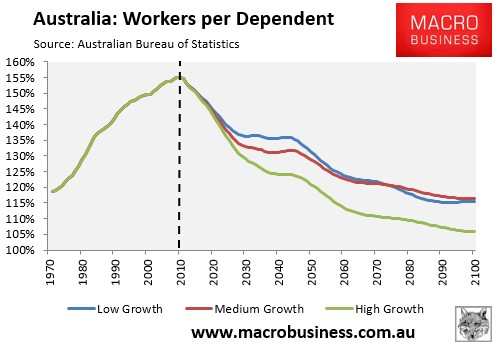

Clearly, Australia’s retirement system is on an unsustainable footing given Australia’s rapidly ageing population and declining tax base, irrespective of the rate of immigration (see next chart).

This is why I keep calling for a range of reforms to the retirement system to ensure that scarce taxpayer dollars only go to those in need. These include tighter means testing of the aged pension, such as inclusion of one’s owner-occupied home in the assets test (or part thereof), in order to remove the ability for retirees to access their super as a lump sum and sink it into their tax-sheltered home (and then access the pension), as well as reducing superannuation concessions for higher income earners.

Without reform to retirement policy, today’s generation Xers,Ys and Zs will become a generation of tax slaves, forced to pay more tax (and consume less) in order to pay for the generous entitlements provided to the old.

unconventionaleconomist@hotmail.com