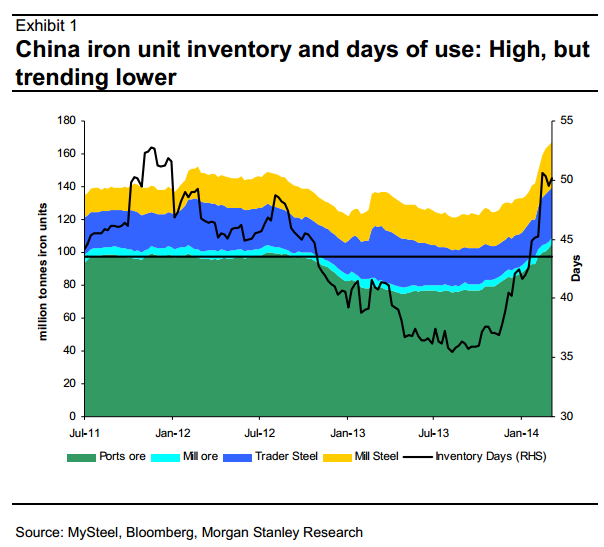

We believe the recent sharp sell-off in copper and iron ore prices has its origins in credit tightness in China. In our view, Beijing is targeting those using commodities for collateral in the shadow banking network – a channel used to evade capital controls and targeted credit policies aimed at reducing excess capacity and pollution.

We think the recent price action in copper reflected the worst case scenario of a rapid unwind in copper inventory financing – a genuine risk, but with a low probability, in our view. In iron ore, we think the quick collapse in price was driven by a “buyer’s strike” as high inventory, slower-than-expected steel production growth and tight working capital forced steel mills to refrain from spot purchases and led sellers to aggressively drop offers.

Can the damage be undone? Indeed, recent macroeconomic and sector-specific data in China have been mixed, leading to an uncertain near- and medium-term outlook for industrial commodities. However, we maintain our base case forecasts for copper and iron ore, as we have yet to see compelling evidence to suggest a fundamental change in China’s consumption patterns this year. We view the current round of price weakness as a buying opportunity.

Funny, when I look at that chart I reach precisely the opposite conclusion!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.