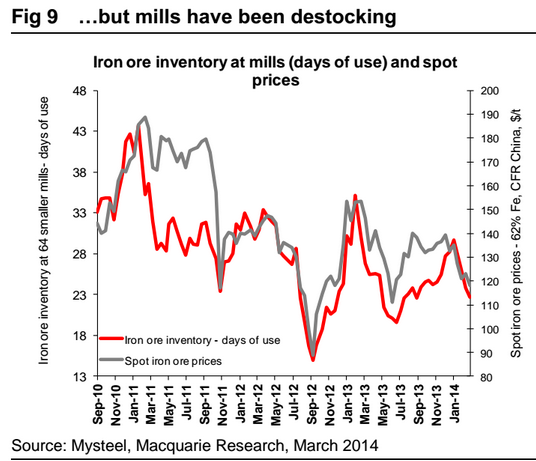

We expect to see mills starting to replenish some inventory as we head into 2Q (price action since Monday suggests this may already be underway). In our view, the swing from mills destocking to restocking is equivalent to adding 30mtpa of annualised iron ore purchasing activity. Combining that uptick with an increase in real demand from rising steel production should see total iron ore demand rising to a level that requires a very similar amount of the high-cost Chinese ore as was used in 3Q13 when prices averaged $133/t.

Given the further ramp-ups in supply expected in the second half, the market balance looks less favorable and this should be expected to result in softer prices (although we outlined here a scenario where marginal low grade seaborne tonnage could be displaced at higher than expected 62% Fe prices).

We have also outlined two alternative scenarios. The bear case assumes a situation where demand weakens further into 2Q, dropping to negative YoY growth. In this situation, we would expect some more aggressive liquidation of steel inventory, meaning production growth would be even lower than demand. In this situation, iron ore would struggle to rise above current levels and there would be an elevated risk of another round of destocking.

The bull case takes a more optimistic view of steel demand, with growth of 5-6% for most of the year. In this case, we would envisage average prices for 2014 looking very similar to those in 2013. However, for this to play out, we’d have to assume China is able to brush off the recent slowing growth trend fairly quickly, which would probably require some form of stimulus before the end of 1Q or early 2Q at the latest.

And that’s the rub. It’s stimulus or bust. Steel mills have destocked but there is scope for more:

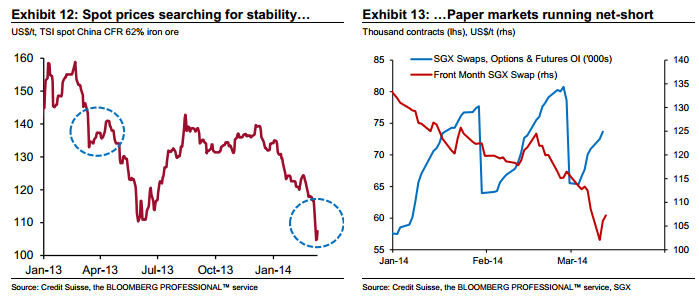

And that’s what Credit Suisse sees:

Advertisement

After sliding 10% in two trading days, physical iron ore has spent the past two days looking for some semblance of stability (Exhibit 12). However, with paper markets running heavily short, firmer physical prices have generated particularly whippy swaps trading, taking realized one-week volatility through 60% for the front month contract.

In terms of the past couple of days, we see it as a natural reaction for some consumers to have picked up volumes after a fall of this magnitude. Indeed, the price dynamics are similar to those in the wake of last March’s $10.50 two-day drop off (Exhibit 12).

Were prices to have continued their near vertical decline it would have likely indicated a far greater deterioration in China’s ferrous market fundamentals than even we have been advocating.

As we wrote on Monday, in the absence of more weighty government action, we expect prices to maintain their downward trajectory as mills continue to destock. This is unlikely to be a linear process.

This underlines the absurdity of the sell-side bullishness on iron ore stocks for the six months. It’s an all or nothing bet on an opaque group of Chinese communists that the guys taking the punt know no better than you and I. Even if they’re proved right in time, they were still wrong to take the bet.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.