Via Zero Hedge comes this must read piece from Goldman Sachs on the unwind of China’s manifold commodity financing scams. Brace!

Financing deal concerns mounting as CNY volatility rises

Concerns on an unwind of commodity financing deals trigger selloff

The recent sell-off in copper and iron ore prices reflects the market’s ongoing concerns regarding the impact of a potential unwind of Chinese commodity financing deals, though the weak underlying market fundamentals should not be discounted. The concerns intensified following the recent CNY depreciation which has raised uncertainty regarding the profitability of the deals and the impact on different asset classes were they to unwind.Up to 1mt of copper and 30mt of iron ore could be released were the deals to unwind, which would be bearish given the relatively limited physical liquidity to absorb the shock.

CCFDs are facilitating China’s total credit growth

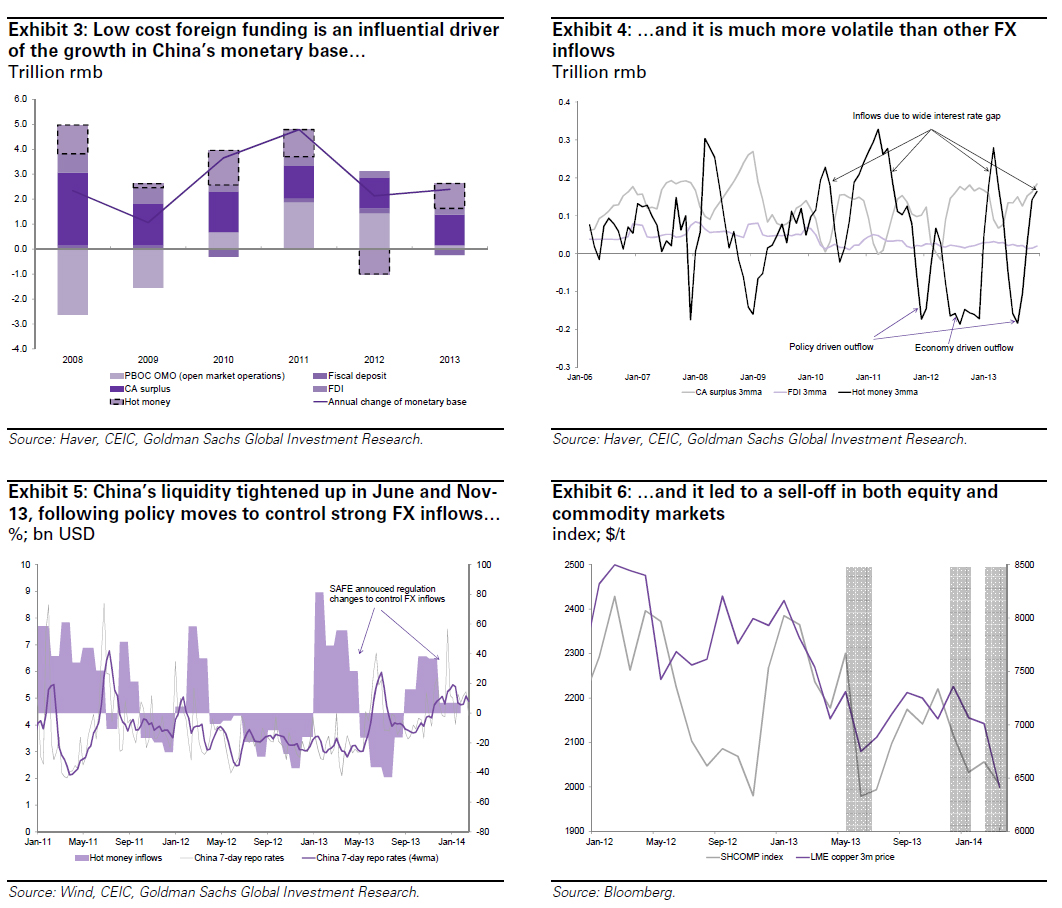

We believe CCFDs are ongoing and facilitating ‘hot money’ inflows into China by providing a mechanism to import low-cost foreign financing. In general, the profitability of most hedged commodity financing deals remains substantial (iron ore is the exception), due to a still positive CNY and USD interest rate differential, limited depreciation in the CNY forward curve and available commodity supply. In 2013, ‘hot money’ accounted for c. 42% of the growth in China’s monetary base of which we estimate thatCCFDs contributed US$81-160 bn or c.31% of China’s total FX short-termloans. Given this, it is crucial for the government to manage the immediate impact of ‘hot money’ flow changes on the economy and markets.

More commodities are used; a medium-term unwind is bearish

An increasing range of commodities are being used to raise foreign financing, which now includes iron ore, soybeans, palm oil, rubber, zinc, and aluminum, as well as gold, copper, and nickel. CCFDs create excess physical demand and tighten the physical markets artificially; in contrast, an unwind creates excess supply and thus is bearish to prices. We think CCFDs will be unwound over the medium term, mainly triggered by an increase in Chinese FX volatility, as indicated by recent CNY depreciation and PBOC’s latest move to widen the daily trading band. FX volatility could result in a higher cost of currency hedging, effectively closing the interest rate arbitrage. Higher US rates are another likely catalyst for an unwind in the long run. A continuous CNY depreciation in the short term, however, would trigger some deals to be unwound sooner than expected, and hence place downside risks to our short-term commodity price forecasts.

It should now become apparent why the ongoing sharp devaluation of the CNY, far more than merely impacting a few massively levered speculators, and recall that the European Knock In point of maximum vega is about USDCNY 6.20 as discussed previously, will have a far more broad hit to asset levels not just in China but across the world if and when the inevitable moment of CCFD unwind finally begins, and in a reflexive fashion, initial selling begets more selling, more CNY devaluation, greater margin calls, further CCFD unwinds, and so on, until finally the PBOC has no choice but to come in and bail out the financial system one more time.

For those unfamiliar with the concept of CCFD, and too lazy to read our previous article on the topic, here is Goldman’s Roger Yuan with a succinct summary of just why these key component of China’s shadow funding mechanism are so important on the way up… and down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.