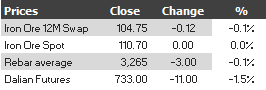

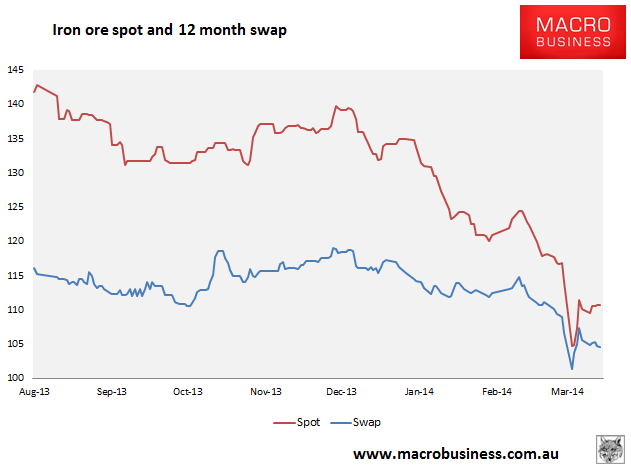

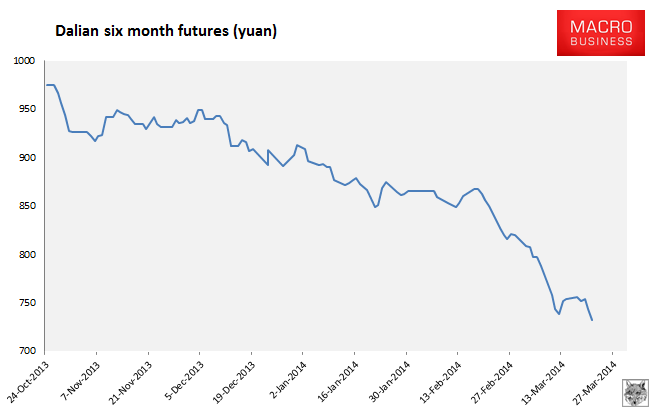

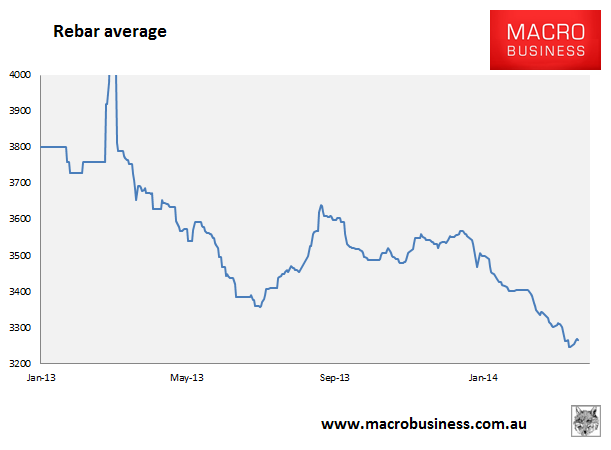

Here are the iron ore charts for March 21, 2014:

Well! That was an unsatisfactory reprieve! Friday action was poor across the board. In paper markets, Dalian September is plumbing new lows, Singapore 12 month swaps are bleeding out steadily, and rebar futures hit new all times lows.

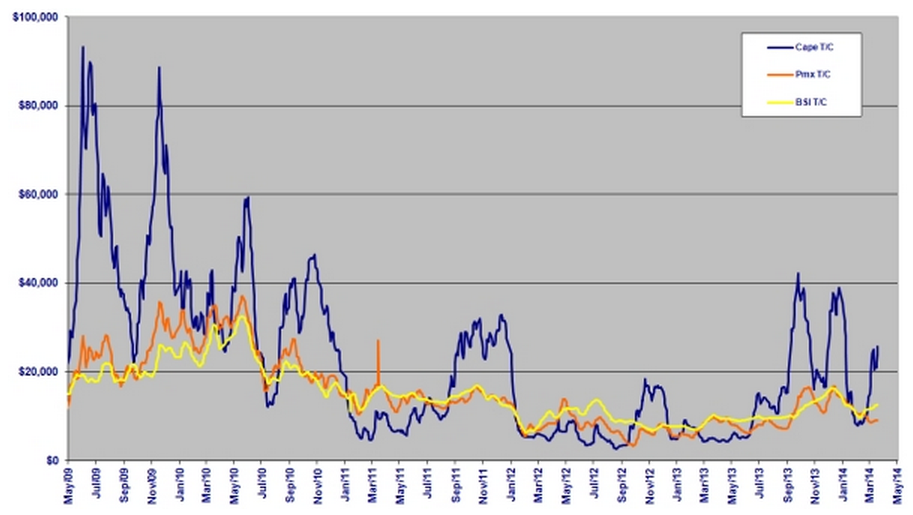

In physical markets, the weak recovery in rebar average stalled, spot was flat and the Baltic Dry sank 3% and is stuck at levels well short of any level signalling restock activity by steel mills.

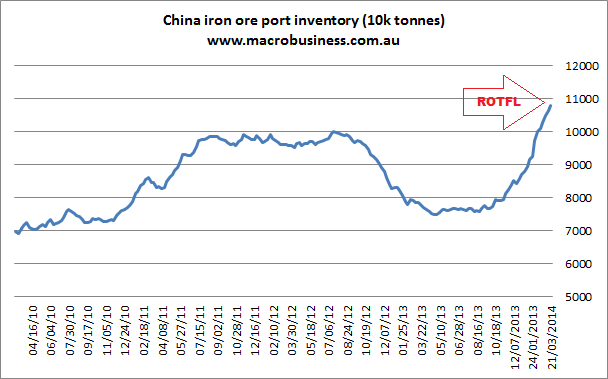

Finally, the morning’s hysterical laugh (in the Freudian sense) goes to port stocks, which lifted another 1.75 million tonnes (mt) on the week to a new all time high of 108.1mt, and are very definitely on some kind of mood-enhancing drug.

From Reuters, the news is bad or worse. Hebei is getting smashed:

China’s Hebei province produced 32.636 million tonnes of crude steel in the first two months of 2014, down 5.7 percent compared to the previous year, reflecting a funding crisis that has left at least 16 local producers on the brink of closure.

The bloated steel sector in northern Hebei is the main focus of a nationwide government campaign to tackle industrial overcapacity, cut sources of air pollution and ease the Chinese economy’s dependence on resource-intensive sectors.

Data issued by China’s statistics bureau show Hebei’s production over the first two months still amounted to 24.9 percent of the national total, down from 26.9 percent in the first two months of 2013 but recovering from November and December, when its share fell to less than 20 percent.

…The January-February output decline in Hebei, traditionally China’s dominant steel producer, was offset by double-digit increases in the provinces of Jiangsu, Fujian, Henan and Hunan.

A seasonal pickup in construction demand in China may not be strong enough to support steel prices as the overall economy faces headwinds from weak external demand that has hit its manufacturing sector, and a reform-minded Beijing.

There is typically a gap of around 500 yuan per tonne between rebar and HRC, a flat steel product used to make cars and home appliances, said Helen Lau, a senior analyst at UOB-Kay Hian Securities in Hong Kong.

But that spread is just above 300 yuan at the moment, with standard HRC steel sold at 3,544 yuan in China and rebar at around 3,200 yuan.

“This spread is too low and it shows there is oversupply of HRC in China. The gap may narrow further if we see more seasonal demand in construction and manufacturing remains weak,” Lau said.

…”We’ve seen some pickup in steel demand in the past two weeks but it’s not really strong enough to push prices significantly higher. A lot of steel mills are still losing money…There was some short-term demand for iron ore driven by mills that took advantage of the price decline. But I see further downside to the price because the fundamentals for the steel market haven’t really changed,” said the Shanghai trader.

All of the data agrees.