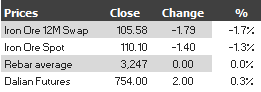

Here are the iron ore charts for March 14, 2014:

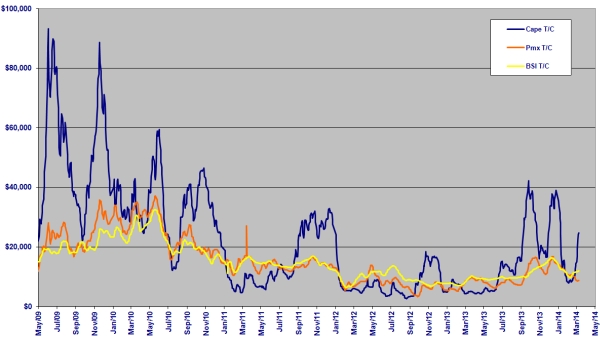

Rebar futures sold off as well. There is no update yet to port inventories. The Baltic Dry continued its rebound Friday, at a reduced pace, with capesize rates up less than 1%:

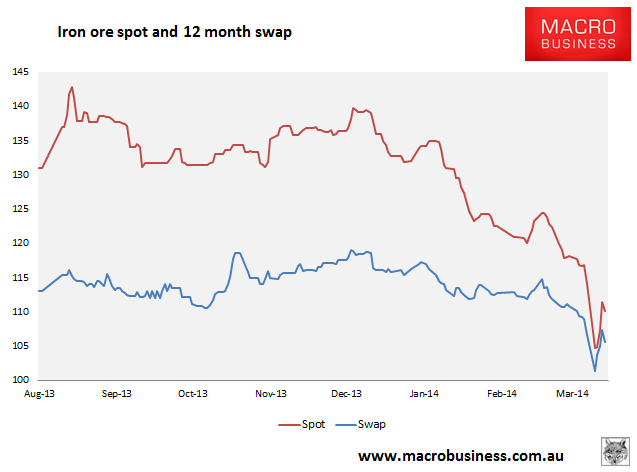

So, not very encouraging market action. Paper markets have managed a weak bounce and physical a little better but both look rather like dead cats today. The Baltic Dry is indicating some renewed buying but by who given steel prices are still very low?. According to Reuters, it’s not steel mills:

…traders say despite the quick rebound, the outlook for prices doesn’t look encouraging.

“Only traders are buying, steel mills are not buying,” said a Singapore-based iron ore trader.

While prices for fresh seaborne cargoes have recovered, those for stockpiles at ports, which stand at a record high 105 million tonnes SH-TOT-IRONINV, have remained low. Mills can buy seaborne cargoes on credit, but they need cash to purchase port stocks.

“I spoke with four steel mills this morning and they told me that sellers at ports are aggressively trying to sell way below prices in other platforms,” said the trader.

Australian 61-percent grade Pilbara iron ore fines are being offered at 720 yuan a tonne at Chinese ports, which translates to $106 a tonne, traders said.

…China’s Baoshan Iron and Steel kept prices for its major products unchanged for April bookings. The price adjustments by China’s top listed steel maker usually set the tone for the industry and its decision to keep prices flat in what is normally a peak steel consumption period points to slow demand.

That rather suggests that the iron ore scams are still robust. But for how long? If spot cargoes are selling at 5% more than port tonnages owing to the trader’s need for cash then the market is nowhere near capitulation yet. If there’s no sudden pick-up in demand forcing mills to push up the spot price via an aggressive restock then more traders are going to go out of business. Yet if liquid mills can pick off cheap port stocks the restock will never come. All things equal, we in a downward price cycle until enough traders (and/or dodgy mills) go bust and the port pile clears.

Also from the South China Morning Post:

Growing jitters about the financial health of bloated mainland industries have prompted many banks to cut lending in these sectors by as much as 20 per cent, banking and industry sources with knowledge of the matter said.

At the same time, the China Banking and Regulatory Commission has called on banks to submit their regular report of outstanding loans owed by various sectors, but has asked them to include loans linked to derivative products and debt financing, the sources said.

The inclusion of these two areas is a “new development”, said one banking source.

…”The specific sectors to be audited are steel, cement, aluminium smelting, flat-glass and shipbuilding,” said another bank source, who received a CBRC document outlining the requirements.

It was not clear what derivatives lending or debt financing the CBRC was focusing on.

But the sources said one area of concern may be bank lending to clients who used commodity imports such as steel or copper as collateral.

I can only observe that despite the good cheer from Australian miners that you can read anywhere and everywhere, their situation is unprecedented. Whether by broadly tight credit, or by more specific prudential restrictions, Chinese authorities now have the power to destroy the iron ore speculator complex that has tormented them for years.