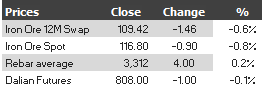

Find below the iron ore charts for March 4, 2013:

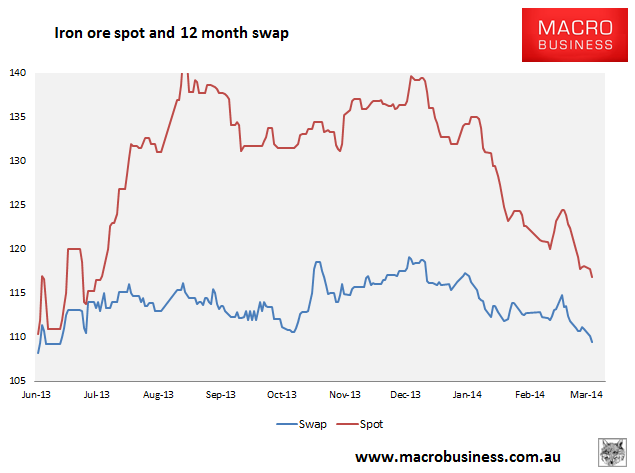

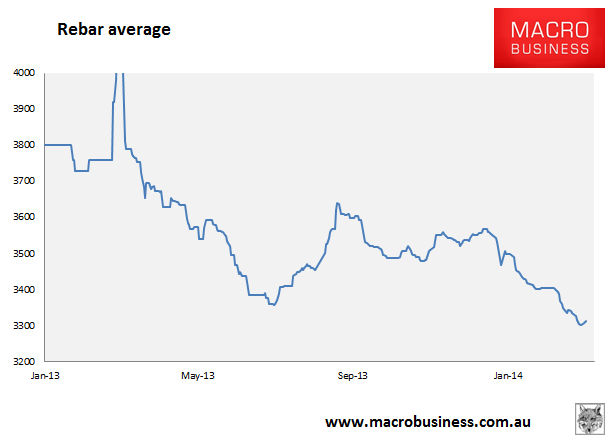

Rebar futures are still trading at their lows. It’s a better mix of weakness today with some steel price support as muted demand returns following winter and outright iron ore price falls indicate active destocking at mills which will ultimately cease and reverse. The breakdown of 12 month swaps presages more short term weakness.

Mac Bank added a little more in a note yesterday:

We attended the Metal Bulletin iron ore conference in Beijing this week. We came away comfortable that the current sell-off in iron ore is an overshoot and linked to destocking. However, it is clear that while steel demand is not collapsing, conditions are not as strong as a year ago. Mills and traders were very much focussed on the current price weakness. At the same conference last year, most discussions were on the second half of the year and the threat new supply posed to prices – this year, the conversation was on the next few weeks and even days. Mills were firmly in destocking mode and sentiment was quite poor, but the market felt divided between mills in Hebei that are struggling under ever more stringent production limitations and those in other regions where conditions are better. The manufacturing sector was reported to be better, with orders improving from the auto sectors.

In similar news, the Chinese steel PMI remains deeply depressed in February, down from January by 0.8 points to 39.9. We turn to Reuters for texture:

“There’s not too much demand coming from the market. Steel consumption is slow and liquidity is tight,” said an iron ore trader in Shanghai.

“Buyers are still not confident about prices and they expect a further drop,” he said, adding he sees iron ore falling another $5-$10 a tonne.

Sounds about right although I warn that I think Mac Bank is complacent. The destocking thesis is in play but so long as underlying conditions are weak, and they will stay that way unless more stimulus is forthcoming, the price falls are a portent not overshoot. Underlying demand weakness will mean any restock is muted, that mills will run leaner inventories this year than last, and that new supply will bleed the price all year. In that context, the port stock overhang remains a constant downside risk.