Apologies for being a little late with my daily post today. I’ve got some data issues. Spot was down slightly to $110.50.

In the mean time let’s take a look at a bullish report on iron ore from Morgans CIMB:

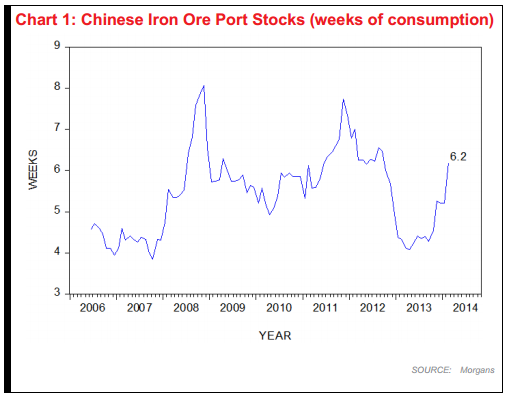

In this issue, we update our model of the iron ore price. Back on 5 February 2014, we noted that Chinese iron ore stocks at port had been rising relative to Chinese consumption. We said we thought that the stocks to consumption ratio would stabilise in coming months. We thought that when the stocks to consumption ratio did stabilise, the price would also stabilise. Both of these events have yet to occur.

Consumption is obviously the rate at which iron ore is being absorbed by Chinese steel mills. This rate of consumption is a function of Chinese crude steel production. Two things happened in February. The first was that Chinese steel production fell. The fall was sharp and we think short term. We think the fall had a lot to do with the time that it takes to restart production of steel after Chinese lunar new year. Another couple of months data will tell us whether we are right or not.

At the same time that consumption fell, we saw Chinese iron ore stocks at port rose. The two of these resulted in a rise in the stocks to consumption ratio seen in Chart 1. In November, December and January the stocks to consumption ratio had stabilised at around about 5.2 weeks. Had it maintained this level, the iron ore market would now be modestly tight. But that is not what happened. The combination of rising port stocks and declining consumption led our stocks to consumption ratio to rise to 6.2 weeks. This is at the higher end of the normal long term range of variation.

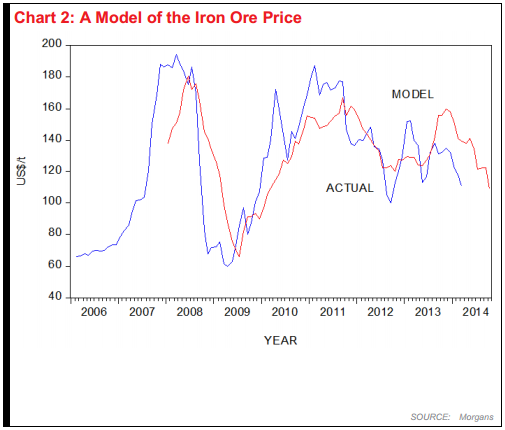

In Chart 2 we show our model of the iron ore price in $US terms. This is based on the stocks to consumption ratio shown in Chart 1. As the stocks to consumption ratio rises, our model estimate of the price drifts down.

Last year when the stocks to consumption ratio was low, our model estimate was suggesting a price above $US130 per tonne. This year as the stocks to consumption ratio has drifted up, that price has drifted down. Still, when the stocks to consumption ratio had stabilised at about 5.2 weeks, our model estimate suggested an equilibrium price for iron ore at around $US122 a tonne. This remained the case through November, December and January.

The increase in the stocks to consumption ratio to 6.2 weeks in February reduces our model estimate to $US108 per tonne. All of this suggests that the iron ore market in China is efficiently processing the same kind of data that we are using in our model.

We think it would be extremely unusual if the market in fact did not stabilise. We are now at the highest level of stocks relative to consumption of the normal operating range of the industry. Were the level of Chinese steel production merely to recover to the January level and then go sideways, the whole feeling of the iron ore market would rapidly recover.

China is not falling into recession. A period of tightness in the money market at the end of 2013 has now been followed by a period of easing money into 2014. Short term money market interest rates have fallen sharply. It is only a matter of time before this easier pattern of monetary policy moves through to a higher level of industrial demand.

We note that the official PMI for the non-manufacturing sector recovered significantly in January. The non-manufacturing sector in China includes construction. A higher level of activity in construction will generate higher demand for steel and in turn higher demand for iron ore. Our best guess is this period of softness in iron ore prices will come to an end in coming months.

That needs some serious unpacking:

Advertisement

As I’ve said before, port stocks should never be taken as a proxy for Chinese demand or as a directional guide to price movements. There have been long periods when Chinese steel mills have run down iron ore inventories as port stocks rise and vice-versa. Port stocks are a useful gauge of the fullness or otherwise of the Chinese iron ore supply chain. A much better guide to prices is the mills iron ore inventories, which are currently lowish bit could go considerably lower yet. The high port stocks now are an overhang for higher prices and downside risk if we get a credit event.

On steel, we don’t know exactly what January levels of production were because official data conflated January and February. The data had the combined months running at about an annualised production rate of 810 million tonnes per annum, 4% up on last year. Then again, the World Steel Association reported flat production year on year for the two months. Even now, CISA is reporting figures of 2.1 million tonnes for the March 1st to 10th period, rising by 0.7% from late February but that’s unreliable as well! The only conclusion we can draw about current steel production is that it is probably running very slightly ahead of last year. More to the point, what is most remarkable about current conditions is that a small fall in the fixed-asset component of Chinese growth has smashed the iron ore market.

It would be unusual if the iron ore prices stayed down or fell further but the circumstances we are in are very obviously unusual as well. China has not framed its slowdown as a reform process so explicitly before, nor has it had the motive of addressing pollution. Arguing the iron ore will rise “just because” is not persuasive.

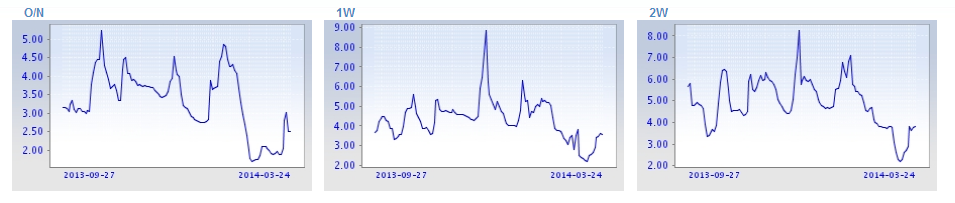

It is not at all clear yet that the PBOC has loosened. In fact, it’s been tightening implicitly via reverse repos in the last week and SHIBOR has jumped (though is still below prior levels):

Its open market operations are Tuesday and Thursday so we’ll know more today but it is equally possible to read recent interbank loosening as the result of bank liquidity hoarding. We know, for instance, that prudential measure are underway, targeting developers, ship-builders and steel so this might be banks not needing money to lend.

At some point this year, when the stimulus flows, there is a reasonable prospect of a temporary bounce in iron ore as steel mills restock inventories but it’ll likely be short-lived as supply mounts. In short I’d be discounting the Morgans report not an iron or recovery.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.