From Westpac’s Elliot Clarke comes an interesting update on US public finances following release of the Congressional Budget Office’s (CBO) revised long-term fiscal forecasts:

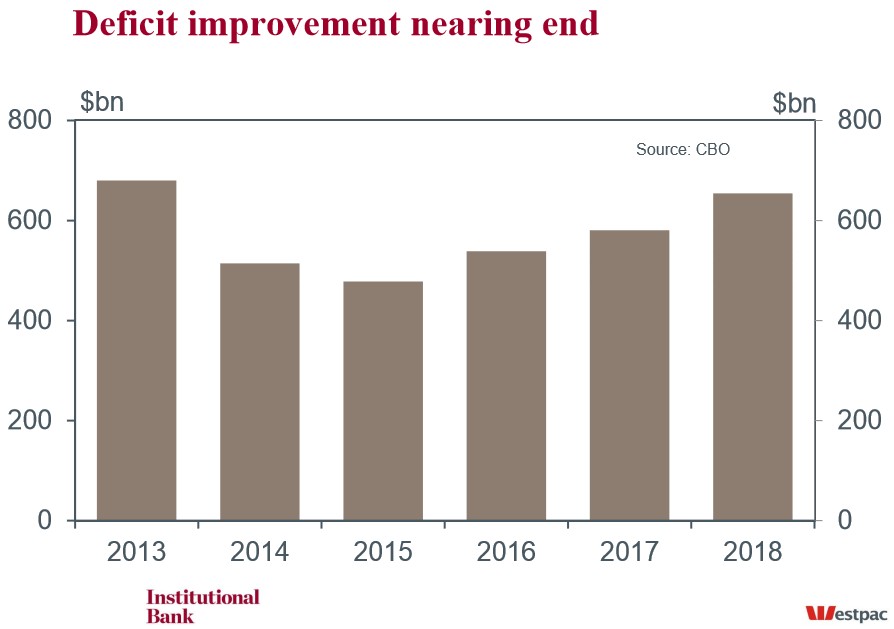

The CBO released its latest update on the US’ long-term fiscal position in early February. In the near-term, the CBO expects the deficit to decline by a further $166bn in FY2014 to $514bn, roughly a third of the $1.4trn deficit reported for 2009. A further $36bn reduction is expected in FY2015. However, even on the CBO’s optimistic forecasts, the deficit will begin a new upward trend in FY2016. By 2024, the Federal deficit is forecast to have risen back to almost $1.1trn – although, by that time, the CBO expects that figure will equate to only 4.0% of GDP.

While much could be said about these forecasts and their reliability, there is a key theme that demands our attention: the enduring burden placed on the household sector to keep the deficit and Federal debt under control, and the subsequent need for strong labour income growth to maintain the size of the tax base and limit the fiscal impact on households’ disposable income.

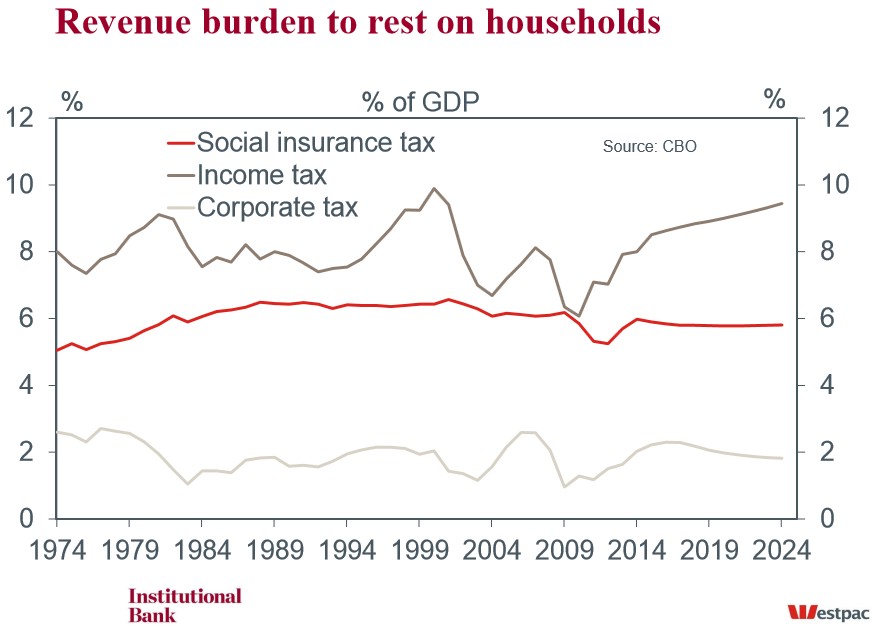

In 2013, around 80% of total Federal revenues were garnered directly from US households in the form of individual income and social insurance taxes. Despite an anticipated rebound in taxable corporate profits following the GFC, the Federal Government will remain dependent on US households for revenue. Indeed, between 2015 and 2024, the average proportion of total revenues expected to come from household-oriented taxes stands at almost 82%.

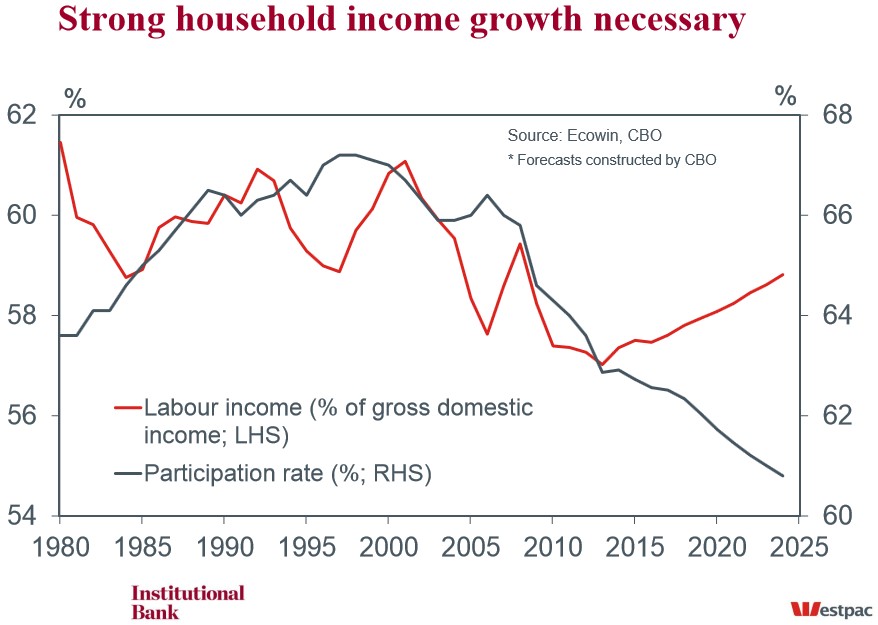

When we also recognise that households are the primary recipient of Federal expenditure, it becomes clear that this substantial burden actually rests with a particular subset of the household sector, namely those still in the labour force. Social security and health care programs (Medicare, Medicaid, etc) are set to average 10.8% of GDP through the forecast period to 2024; that equates to 81% of mandatory outlays and around 57% of total non-interest outlays. So as to balance receipts with these mandated expenditures, the CBO has assumed that, by 2024, labour income’s share of gross domestic income will trend back to a level last seen in 2005 (excluding the GFC-induced spike in 2008). This seems rather contentious given the lingering impact of the GFC and the ageing of the population which is becoming more apparent.

Relative to the 186k monthly gains for nonfarm payrolls over the past two years, the assumed monthly job growth of 147k through to the end of 2017 (and 67k per month from 2018 to 2024) does not seem that big an ask. But what does warrant attention is the assumption that this modest pace of job growth – together with a continuation of the trend decline in the participation rate – will bring about persistent wage growth strong enough to see labour incomes’ share of gross domestic income rise as forecast.

Through 2012 and 2013, the employment cost index has risen by around 2.0%yr. The CBO anticipates this will accelerate to 2.6% in 2014 and to 3.9% by 2017 after which it will average 3.7%yr through 2018 to 2024. While the CBO’s assumption is theoretically consistent with their expectation that the output gap will close, it seems out of touch with the reality that employment growth has only just outpaced population growth in the recovery to date and that (on the CBO’s forecasts) this trend is set to continue. The implication of wage growth failing to accelerate as hoped is that the size of the Federal income and social security tax base could remain stagnant or fall relative to the economy instead of grow.

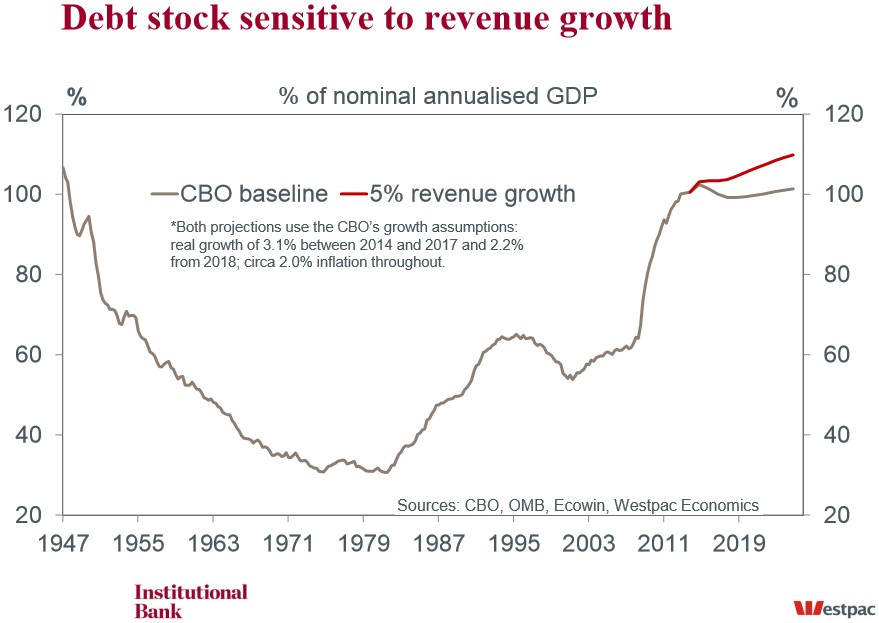

Given the apparent rigidity in Federal outlays highlighted above, if household income growth disappoints, then US Federal deficits and gross debt will rise at a more rapid clip than anticipated. A simple scenario based on 5% annual revenue growth (around the historic average) highlights the sensitivity of gross debt to revenue growth, with gross debt around 9ppts of GDP higher by the end of the forecast period than under the CBO’s baseline assumptions. Any change to taxation to counteract larger deficits would be targeted towards households, reducing their disposable income. There would be obvious flow-on impacts for activity as well as the state and local government authorities whose revenues are also dependent on households – property at the local level, and consumption for state authorities.

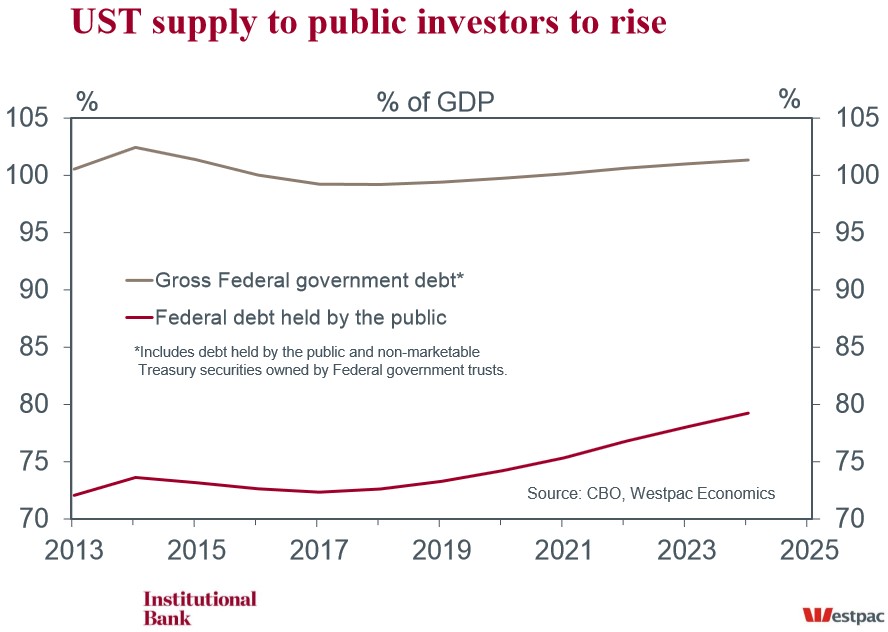

As a final point, it is worth noting that the ageing of the population will also impact demand for US Treasury debt, with the Federal investment trusts progressively buying less non-tradeable debt as they increasingly use inflows (and eventually the trust principal) to fund pension and health benefits. The consequence of this shift is that a greater proportion of gross Federal debt will have to be purchased by the public, i.e. non-government domestic parties and/or foreign investors. Any consequence for yields of greater public Treasury security supply will obviously depend on the strength of demand.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.