Following last year’s poor efforts (here and here), the Reserve Bank of Australia (RBA) has once again tried to pin Australia’s expensive housing on high construction costs, and in the process, played-down the role of inflated land prices and planning constraints.

FromThe AFR:

Officials at the RBA argue that while supply constraints including regulatory and zoning limits, and geography are placing upward pressure on house prices, the greatest impact is from the cost of construction.

“In many cases the bulk of the cost of a new dwelling is the cost of construction, not the government charges or land, though construction costs might be lower if some building regulations were changed”…

And here is the RBA’s chart supposedly breaking down the cost of new homes, taken from its submission to the Senate Inquiry into Housing Affordability:

This is nonsensical analysis by the RBA. The latest HIA-RP Data Residential Land Report showed that the weighted median fringe capital city land price was $226,448 as at September 2013, implying that land prices comprise the majority of the cost of newly constructed housing.

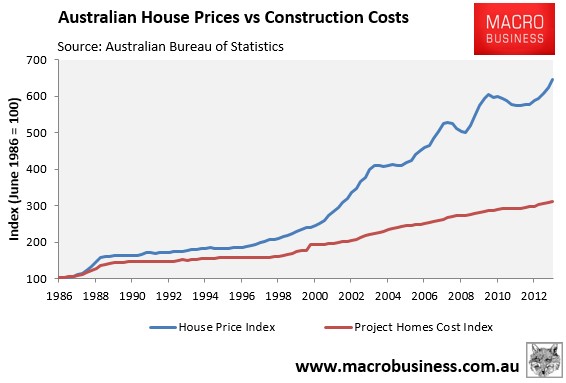

Further, according to the ABS, the cost of building new project homes (i.e. the cost of constructing the physical dwelling, excluding land costs) has been lacklustre when compared against the growth of house prices (which includes land costs), suggesting that the bulk of the cost escalation of new homes has been in lot prices, not dwelling construction costs (see next chart).

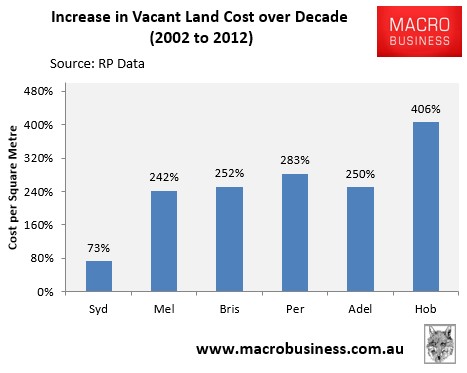

The RBA’s suggestion that land prices are not a major cost in greenfield developments is also not backed-up by data. As shown in the below table from RP Data, land prices in each and every capital city surged in the decade to 2012:

In fact, the land cost per square metre more than tripled in all capital cities, with the exception of Sydney, where vacant lot prices were already expensive (see next chart).

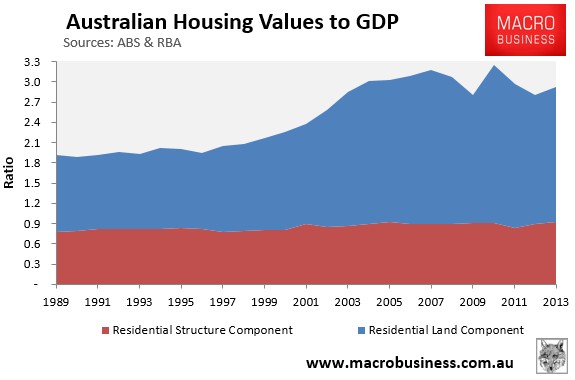

The above charts are also broadly supported by aggregate land and dwelling values data produced by the ABS and RBA, which shows land prices roughly doubling against GDP since the mid-1990s, whereas the value of physical structures has flat-lined (see below chart).

If the above data is not proof of rampant inflation in land costs, I don’t know what is.

Back to the RBA:

The RBA’s report points to evidence that cities with larger populations have more expensive housing, even relative to their higher incomes. It says that unlike many comparable countries, Australia lacks medium-sized cities of 500,000 to 1 million people which could provide better locations for more affordable housing, while still offering job opportunities usually missing in smaller towns.

Let’s not kid ourselves. Australia has a relatively small population of only 23 million people, or roughly 1/14th that of the United States. Moreover, none of Australia’s cities are large by global standards. Even Greater Sydney (population 4.4 million) would only just rank in the top 10 largest urban areas in the United States. Yet our residential land prices are absurd by global standards, running well above most other countries where land supply is genuinely scarce (rather than made scarce through regulation and lack of infrastructure provision).

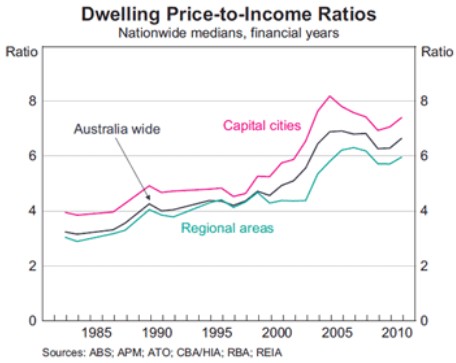

To add insult to injury, housing costs are inflated in regional areas as well, with house values there nearly six times incomes, according to the RBA:

Unaffordability is a problem right across the country, not just in the major cities.

Back to the RBA:

“While there are no doubt regulatory changes that can be made that would reduce the costs and time involved in housing construction projects, it is questionable whether this would reduce prices by enough to bring home purchase within reach of many additional households”…

While extra supply could dampen price growth, as has probably occurred in Melbourne and parts of Queensland, prices would still need to be “significantly lower” to match current household budgets for those who cannot pay. “History shows that this [price depreciation] would be difficult to achieve without also constraining demand – that is to say buyers’ capacity to pay. Such an outcome could not be described as an improvement in affordability.”

If one takes a wander beyond one’s desk at Martin Place to study markets where homes are affordable, despite rock bottom interest rates and/or rapid population growth, a few prominent examples become quickly obvious. Pittsburgh, Dallas, Houston, Atlanta, and a bunch of other North American cities with affordable housing would be a start, supplemented by an examination of Germany’s housing system.

Throwing your hands up in despair is hardly quality public policy.

Back to the RBA:

The RBA also warned the housing market was likely to experience more periods of falling prices than in the past, because “periods of price falls make development of new homes unattractive.

“This shift may also have the result that supply is weaker in downturns than was the case in the past, and takes longer to pick up”.

This is what happens when government policy puts a straightjacket on supply. As shown by the RBA’s own chart (below), the rate of dwelling supply contracted sharply from the mid-1990s, just as Australian house prices began their decade long run. If housing supply was responsive (‘elastic’), such an increase in price would have elicited a supply response, which would have mitigated further price rises. This clearly didn’t happen, hence the conclusion that Australian housing supply has become increasingly unresponsive (‘inelastic’), which highlights the dire need for supply-side reform.

Oddly, the RBA’s former head of economics, Anthony Richards, used to make these same arguments, during testimony in 2008:

…supply-side factors should have a much greater influence on prices towards the fringes of cities, where land is less scarce and accounts for a smaller proportion of the total dwelling price. In principle, the price of housing there should be close to its marginal cost, determined as the sum of the cost of new housing construction, land development costs, and the cost of raw land. And in the absence of any restrictions on supply, the price of raw land on the fringes should be tied reasonably closely to its value in alternative uses, such as agriculture. So unless there has been a marked increase in the value of this land when used for other purposes, the availability of additional land towards the edges of our cities should have limited increases in the cost of housing there…

So if we are looking for explanations why housing is not as affordable as we might like, it may be necessary to look at factors on the supply side as well. One obvious place to start is the cost of land for building new houses near the edges of our cities…

There are no doubt a number of factors that could be contributing to the observed level of land prices… One factor that has been widely mentioned is the existence of various constraints on land development, including growth corridors and boundaries. Another factor that has been mentioned is the existence of a range of government charges, including developer levies or infrastructure charges. More broadly, concerns have also been expressed that zoning policies and building approval processes have hampered in-fill development closer to the city centres.

Both economic theory and international evidence suggest that housing prices can be boosted by land usage policies (which can create artificial scarcity of residential-zoned land), problems with the complexity of the development process (which creates rents), and the fees and charges imposed on development. Accordingly, the fact that higher prices for housing have not resulted in a more significant supply response could be a reflection of various supply-side costs that have represented a wedge in the cost of bringing new housing to market.

…the fact is that real price increases in the outer suburbs have been quite large as well.

The RBA has also contradicted testimony by former Governor, Ian McFarlane, who in 2006 acknowledged that land supply and housing have become increasingly unresponsive to changes in demand, resulting in higher prices and declining affordability:

“Why has the price of an entry-level new home gone up as much as it has? Why is it not like it was in 1951 when my parents moved to East Bentleigh, which was the fringe of Melbourne at that stage, and where they were able to buy a block of land very cheaply and put a house on it very cheaply? Why is that not the case now? I think it is pretty apparent now that reluctance to release new land plus the new approach whereby the purchaser has to pay for all the services up front – the sewerage, the roads, the footpaths and all that sort of stuff, has enormously increased the price of the new, entry-level home”…

A more conspiracy-minded analyst than myself might conclude that the underlying reason for the RBA’s new found supply-side obtuseness is that it has become the Australia’s key defender of high house prices. Not only has the RBA changed tack on the supply-side, but it has offered cherry-picked analysis of other markets that concludes more responsive housing supply decreases financial stability.

What went wrong one wonders.