Business Spectator’s Rob Burgess made the following keen observation over the weekend on the hidden cost of Australia’s housing obsession, which has damaged Australia’s productivity:

Trying to pin Australia’s mediocre productivity on factory-floor wages is just not good enough.

…productivity problems lie just as much on the capital side of the equation.

For 15 years, the Australian media have celebrated the nation’s appetite for pouring domestic and foreign capital into non-productive assets – the housing stock – while many firms have failed to recapitalise to upgrade technology, management techniques or plant and equipment.

We have now reached something of an impasse. Younger Australians can’t afford to live on the wages IR consultants suggest, but if capital were directed back into businesses such as SPCA, and the infrastructure that connects such businesses to markets at home and abroad, productivity would soar. Wages could rise to match our spiraling cost of living.

It must be remembered that though CPI inflation is currently low, it does not capture the costs of home ownership. It captures rents, which have lagged house-price appreciation due to negative gearing and cultural factors.

We’ve been sanguine about inflation, while house-price inflation has hit workers very hard…

Excessive wage claims by unions will stop at the same time as the productivity debate starts to look at all the factor-inputs in businesses, rather than blaming workers already struggling to pay the bills.

Advertisement

Burgess’ observations follow similar sentiments expressed by Business Spectator’s Alan Kohler late last year:

The high price of land in Australia is one of the reasons businesses like Holden and Qantas are uncompetitive and the combination of several recent developments is making the situation much worse…

It is a combination of factors that will tend to make Australia even less competitive as housing costs rise and put upward pressure on wages, and put huge intergenerational pressures on families as first home buyers are priced out of the market…

The inevitable result is higher prices and less affordable housing, putting more upward pressure on wages and making Australian industry even less competitive than it currently is.

Both Burgess and Kohler are spot on in targeting Australia’s housing obsession, which has manifested in inflated land values.

Advertisement

Land is a key input cost for most businesses. So when costs are inflated, it reduces the competitiveness of industry, making it harder for Australia to compete abroad. The associated higher housing costs also places upward pressure on wages.

For decades, resource allocation has been channeled away from the tradable sector and infrastructure investment towards the financial sector, as home buyers have taken on ever-bigger mortgages as they chased house prices higher. It should be no surprise that the finance and insurance industries – which are dominated by mortgage lending – have grown at more than twice the pace of the rest of the economy since financial markets were deregulated in the mid-1980s, due in part to the housing quango operated by the various levels of government (see below charts).

Advertisement

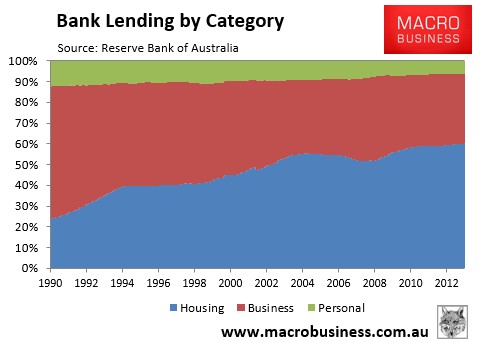

Australia’s housing obsession has also starved productive sectors of the economy of credit. In the early 1990s, Australia’s banks lent nearly two-thirds to businesses, with the balance split between housing and personal lending. However, after the mid-1990s explosion of housing values, these ratios have reversed, with housing lending dominating at the expense of businesses (see next chart).

Advertisement

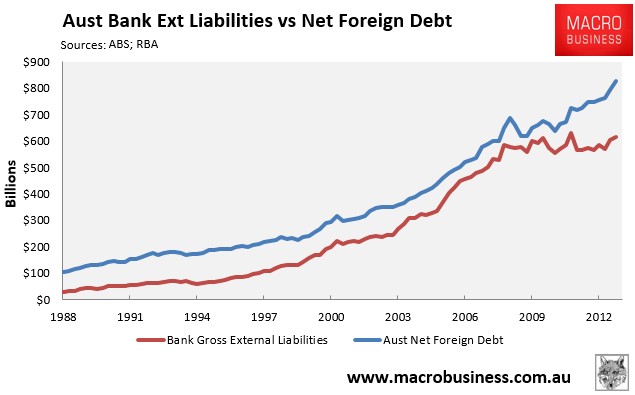

To add insult to injury, much of the boom in mortgage lending has been funded by heavy offshore borrowing by Australia’s banks, in turn driving-up Australia’s net foreign debt:

At the heart of the problem are Australia’s unique mix of tax concessions, such as negative gearing, and the constipated supply system. The former has increased the relative attractiveness of housing investment, boosting demand, whereas the latter has materially dampened the supply response. The end result is too much of the nation’s capital tied-up in housing, which has chocked-off productive areas of the economy.

Advertisement

Indeed, my fellow blogger, Cameron Murray, has estimated that a considerable slice of Australia’s declining multi-factor productivity has resulted from escalating land prices:

The ABS explains that they take the balance sheet value of land from the national accounts to include as the land component of capital stock. We can observe in the chart below the rise in the value of the land balance sheet value against the estimate of MFP, and indeed against an estimate of the land balance if land values simply tracked inflation. Quite clearly, from about 2002 onwards the abnormal increase in the value of land lead to a flattening and falling estimate of MFP. More telling is that fall in all land asset values in 2009 lead immediately to an increase in the MFP measure, only for the next wave of land price escalation, especially FHOB stimulated residential land, to cause a deterioration in MFP during 2011.

We can dig a little deeper into the ‘land balance sheet’ in the system of national accounts, and look closely at the type of increases in land value estimated. The chart below shows in blue the neutral holding gains – that is, the change in the value of land expected if prices tracked inflation. This measure is the result of In red we see the real holding gains, which are market-based increases in land values. As the ABS notes“Holding gains and losses accrue to the owners of assets and liabilities purely as a result of holding the assets or liabilities over time, without transforming them in any way”. In economic terms, they are pure rents.

When red is greater than blue, we find a significant downward bias in the MFP estimate. It is really that simple. And we are not alone in this either. Spain’s land price boom resulted similar pattern of declining MFP during their land price boom in the early 2000s.

One can only wonder how Australia would have looked if the billions of dollars of excess capital that had been poured into pre-existing housing had instead been funneled into businesses and infrastructure, as occurs in places like Germany. Instead, Australia has been left with non-mining companies that are struggling to compete and an infrastructure deficit that former Treasury secretary, Ken Henry, today claims is hindering Australia’s ability to provide goods to Asia.

Advertisement

Rather than merely denigrating workers pay, the long-term solution to Australia’s competitiveness requires changing the tax system so that it rewards productive investment, as well as liberalising the myriad of constraints on land supply and planning that have forced-up urban land prices, raising business costs and wages.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.