Earlier this month, I wrote an article questioning whether the Government should abolish the diesel fuel rebate, arguing that it seemed at odds for a Government that has taken a hard line on subsidies, corporate welfare and the end of the age of entitlement.

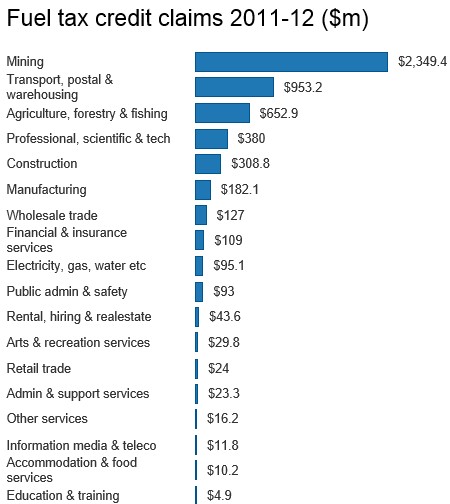

To recap, the diesel rebate, which allows eligible companies to claim a reduced rate of excise for fuels, costs the Budget around $6 billion annually, with the lion’s share of concessions – around $2.3 billion – going to the mining industry (see next chart).

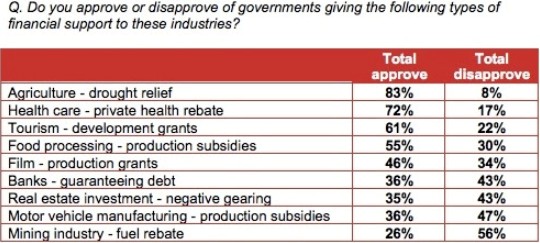

Public support for the rebate is also appears to be low, with a recent opinion poll conducted by Essential finding that it had only 26% support among respondents – the lowest support out of the “subsidies” canvassed (see below graphic).

After writing the article, I received a number of emails arguing that the diesel rebate is not a subsidy, since business input costs – be they electricity, wages, or GST – are always deductible by companies for tax purposes. Moreover, the purpose of diesel excise is as a public road user-charge, however, diesel is used off road by a number of sectors – not just in mining, but also farming and construction – for both power generation and heavy machinery.

Indeed, the Henry Tax Review argued that the diesel rebate is not a subsidy for the use of fuel:

The system is intended to remove or reduce the incidence of fuel tax from business in puts, so that its incidence falls primarily on certain private consumption of fuel. This limits the impact on production decisions. For example, fuel tax credits mean that all electricity generation using liquid fuels is effectively free of fuel tax, in the same way that coal or natural gas inputs to electricity generation are untaxed. [pg 288]

Similar arguments have been made by the Australian Treasury (see here and here):

Fuel tax credits are not a subsidy for fuel use, but a mechanism to reduce or remove the incidence of excise or duty levied on the fuel used by business off road or in heavy on-road vehicles. The incidence of fuel tax is intended to fall on fuel use in private vehicles or for other private purposes and in light on-road vehicles used by business.

Similar to goods and services tax input tax credits, fuel tax credits remove taxation from business inputs. Their purpose is to avoid distorting business investment decisions and behaviour that would occur through taxing business inputs

Given the above, I was wrong to suggest that the diesel rebate is a “subsidy”. Taxing a business input (fuel) other than as a road user charge (or to address an explicit externality) goes against the principles of good tax policy.

A better (less distortionary) option for raising additional tax revenue would to be to implement some kind of resources rents tax. Unfortunately, we stuffed that up.

unconventionaleconomist@hotmail.com