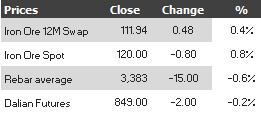

Here are the iron ore charts for February 12, 2014:

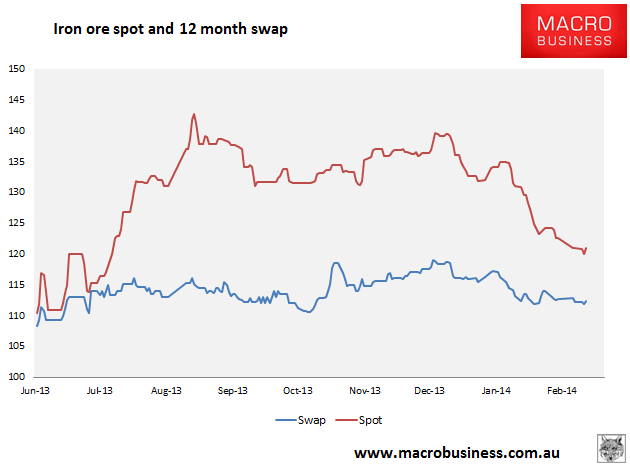

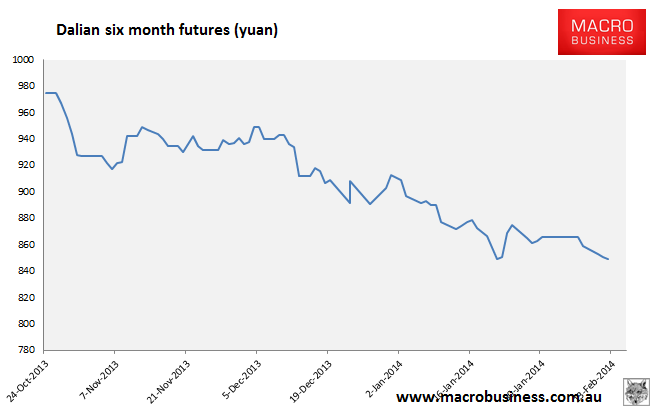

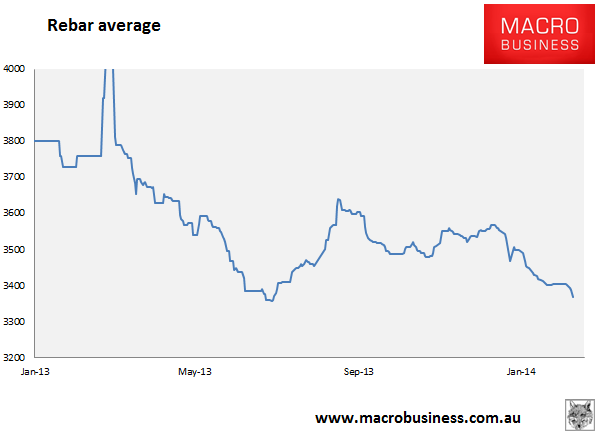

A little reprieve for ore but not steel. As I said yesterday, these markets are all approaching long term supports. They are now sitting right on them.

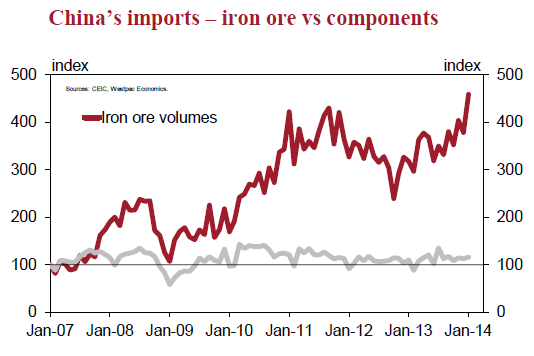

Today’s eye-popping statistic is yesterday’s revelation of January iron ore imports summarised beautifully by Phat Dragon:

• On the import side of the ledger, Phat Dragon was floored when this number launched off his spreadsheet and landed a jab-jab-hook combination: 86, 835. That is the completely absurd amount of iron ore, in thousands of tons, China imported in January. That is an enormous number. How enormous? The increase from December, 9mt, is not far short of the monthly import needs of the entire Japanese steel industry, and it added an additional $US2bn to the country’s import bill. It is also 11.6% higher than any previous monthly inflow. Imports had never exceeded 80 mt in a month before and their first venture above that threshold was almost 87!

• The obvious question is where did it all go? The first place to enquire is naturally at the port, and yes, the weekly data confirm a major accumulation of stock in January. Indeed, Phat Dragon has been questioned about precisely this build-up in recent days. A number of points are applicable here. The first is that imports are gaining market share in China’s total ore supply, and therefore they should be growing consistently faster than demand (steel output was running around 12% in Q4). Second, given credit is neither cheap nor abundant at present, it is most unlikely that there is a large speculative element to the rise in stocks, because holding ore for such purposes would be prohibitively expensive right now. The corollary to this point is that the ore is principally earmarked for real demand. Third, it is normal to stockpile raw materials ahead of the LNY, and arguably also to insure against both the wet season in northern Australia and frozen mines in China’s upper latitudes. None of these factors are unique to any given year, except that January 2014 did not lose any working days on which such activity could occur. On this point Phat Dragon ventures that in 2010, the LNY began on St Valentine’s Day, four days later than this year, and steel output was growing by 39%yr at the time. In January 2010, iron ore imports fell 25% from December 2009. The moral of that story? 86, 835 is at least as big as it looks, if not bigger.Fair enough. But I have a few issues with this analysis. Port Hedland shipments fell 3% in January from December and although they are still up a staggering figure year on year, one would not expect shipments at Australia’s largest iron ore port to be down in a blowout Chinese import month of such magnitude. Especially so since most of the new capacity in the market is channeling through Port Hedland via Fortescue’s massive ramp up.

Second, the tight credit argument applies just as strongly to sources of end-user demand, especially Chinese steel mills which are being slowly rationalised. There is no evidence either way who and what this iron ore is for. This is all the more mysterious given terribly weak steel prices and falling profitability at the mills.

Third, the price of iron ore itself has been falling fast throughout January. Either the market is so abundantly supplied that even a massive surge in demand can’t absorb it or the January import figure is exaggerated. There’s a nine day shipment time from the Pilbara to China, add a few more days for unloading and processing and it’s easy to conclude that some of December’s blowout in Australian trade and shipping figures are only now showing up in China’s January import data.

But we are splitting hairs. It is undeniable that China is now sitting on one God almighty stockpile of iron ore and the making of it has not pushed up the price terribly, meaning the downside of any destock, should it come, will be precipitous. I haven’t got firm data yet on mill ore inventories but a rough lead tells me that they had not destocked at all up until last week. With rebar average prices falling out of bed yesterday and now sitting right at last year’s lows, the risk of a large destock remains high as Q1 passes.