Back in September, just prior to the Federal Election, I explained why I believed that Family First had the best housing policy in Australia.

Thankfully, Family First’s chairman and former home builder, Bob Day, was elected as Senator for South Australia and will assume his seat on 1 July 2014.

Advertisement

Already, Bob Day has began making waves on housing policy, delivering an eye-opening submission to the current Senate standing committee on affordable housing. Below are some key extracts from Bob Day’s submission, which raise similar concerns about Australia’s constipated land supply system as I have raised many times on this site:

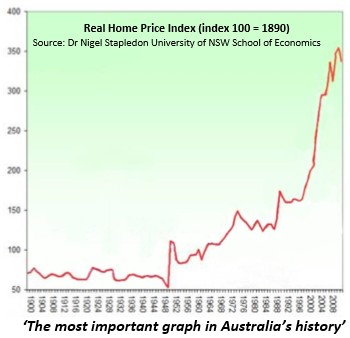

For more than 100 years the average Australian family was able to buy its first home on one wage. The median house price was around three times the median income allowing young home buyers easy entry into the housing market.

As can be seen from the graph, the median house price is now, in real terms ie relative to income, more than nine times what it was between 1900 and 2000. At nine times median household income a family will fork out approximately $600,000 more on mortgage payments than they would have had house prices remained at three times the median income. That’s $600,000 they are not able to spend on other things – clothes, cars, furniture, appliances, travel, movies, restaurants, the theatre, children’s education, charities and many other discretionary purchase options.

The economic consequences of this change have been devastating. The capital structure of our economy has been distorted to the tune of hundreds of billions of dollars and for those on middle and low incomes the prospect of ever becoming homeowners has now all but vanished. Housing starts have plummeted and so have all the jobs associated with it – civil construction, house construction, transport, appliances, soft furnishings, you name it. Not to mention billions of dollars in lost GST revenue to the States. And while the slump in business conditions over the past years have been blamed on everything from the GFC to the high Australian dollar the real culprit has been the massive redirection of capital into high mortgages. And looking to the Reserve Bank to fix the problem through monetary policy ie lowering interest rates, isn’t going to work.

The distortion in the housing market, this misallocation of resources resulting from the supply- demand imbalance is enormous by any measure and affects every other area of the economy. New home owners pay a much higher percentage of their income on house payments than they should. Similarly, renters are paying increased rental costs reflective of the higher capital and financing costs in turn paid by landlords.

The economic consequences of all that has happened over these past few years have been as profound as they have been damaging. The housing industry has been decimated as have industries supplying that sector. The capital structure of our economy has been distorted and getting it back into alignment is going to take some time. But it is a realignment that is necessary. A terrible mistake was made and it needs to be corrected.

HIGH HOUSE PRICES: AUSTRALIA’S URBAN DISASTER

…1995 to 2005 was a decade in which the traditional relativity between average household incomes and median house prices was shattered, putting home ownership beyond the reach of a vast number of Australian families. Where historically the median Australian house price had been three times median household incomes, by 2005 it had risen to more than six times that level in all Australian capital cities, and housing affordability went into serious decline.

Home ownership has long been a feature of Australian life. The level of home ownership rose sharply in the postwar period from 53 per cent in 1947 to 70 per cent in 1995…

In recent years however, a disturbing trend has emerged in the level of home ownership among young families. It is in substantial decline. We have witnessed, quarter by quarter, the erosion of housing affordability from 1995 onwards.

As the impact of rising house prices began to bite in the latter part of his tenure, Prime Minister John Howard often responded saying, “I don’t have people complaining to me about the increase in the value of their homes.” And this was true. Existing home owners were, for the most part, content with their new-found wealth as they reaped capital gains beyond their imagination and interest rates remained at historical lows. They used the equity they had in their homes to borrow big and their ambitious acquisition of investment properties caused, in the words of the Productivity Commission, “overshooting” in the housing market…

While existing home owners were big winners, first home buyers suffered. Home ownership was fast becoming the privilege of the few rather than the rightful expectation of the many, and the province of older Australians at the expense of the young. At the close of the Howard era affordability for first home buyers was the worst on record…

It is undeniable that demand factors played a role in stimulating the housing market and those factors were, for the most part, in the hands of the federal government. However, the real culprit, the real source of the problem, was the refusal of state governments and their land management agencies to provide an adequate and affordable supply of land for new housing stock to meet the demand.

The regulatory seeds of the housing affordability crisis were sown in the 1970s. Until then land was abundant and affordable, and the development of new suburbs was largely left to the private sector. These leafy pre-1970 suburbs with large allotments and wide streets are enduring testimony to the private sector’s ability and to the traditional approach to urban development.

Into this environment strode state and territory governments of all persuasions as they introduced agencies to manage urban growth. The aim of these government agencies seemed noble enough – to ensure a plentiful supply of land to meet future housing needs.

In South Australia for example, the South Australian Land Commission’s primary aim, embedded in the Land Commission Act of 1973, was “the provision of land to those members of the community who do not have large financial resources”. The Act further made it clear that the Commission “shall not conduct its business with a view to making a profit”. In 1981 these noble motives were deleted from the legislation as the Land Commission was reconstituted as the South Australian Urban Land Trust under a new Act.

But worse was to come. As land supply began to dwindle in the mid-1990s – the result of government planning regulation and zoning, a rationing effect came into play and land prices started to rise. These rises were more dramatic than most thought possible, and at a time when first home buyers most needed help, the noble intentions that were used to justify the formation of these land agencies simply vanished and another set of aims was imposed.

In South Australia, the relevant authority, by this time known as the Land Management Corporation, had a mandate to “maximize financial returns to government”. Note the blatant shift of emphasis from the original mandate – from the interests of the buyer – “those members of the community who do not have large financial resources” to the interests of the seller, the Land Management Corporation; from “maintaining land affordability” to “maximizing returns to government”.

In 2007/2008 the Land Management Corporation recorded a profit of $121m. This from a Government agency established with a mandate to “not conduct its business with a view to making a profit.”

Since its inception in 1973, the South Australian State Government’s land agency has seen land prices rise from $15,000 per block (in current dollars) to $160,000 per block, more than a tenfold increase. By comparison, the cost of building a 135 square metre house increased from $97,000 in current dollars to just $102,000 over the same period, virtually no increase at all. Think about that for a moment – a ten-fold increase for a commodity (land) controlled by government (with a so- called “price containment” policy), compared with virtually no increase at all for a commodity (the house) controlled by the private sector (with no price containment policy). One can only conclude that had the private sector been allowed to manage land supply, like it has managed housing supply, we’d be enjoying land prices significantly lower than they are today.

This massive escalation in the price of land carries with it a multitude of detrimental impacts. Establishing affordable rental accommodation for those in greatest need becomes even more difficult for social and public housing authorities as they seek to purchase land and houses in a greatly inflated market. Road widening and major infrastructure projects experience cost blow-outs as land acquisition costs skyrocket, and establishing schools, community centres, health services and business facilities becomes difficult, and at times impossible. The whole community suffers as a result of increased tax, transaction, finance and establishment costs.

It is important to remember that the “scarcity” that drove up land prices is wholly contrived – it is a matter of political choice, not geographic reality. It is the product of restrictions imposed through planning regulation and zoning.

While state governments embraced the opportunity to garner windfall profits by stifling the release of land, they were also responding to a wider ideological agenda driven by a powerful planning community that sought to curb the size of our cities. “Urban consolidation” became the new mantra…

Urban planners, by promoting urban consolidation and at the same time demonising urban sprawl, have inflicted enormous damage on the economy and society. Billions of dollars have been wasted and enormous pain inflicted on the community as a result. And all they ever say in defence of their ideology is, “It depends what you want our cities to look like.” Well, they’d look a whole lot better without the traffic congestion, air pollution, destruction of biodiversity and those high-density infill projects which destroy the character of some of our most beautiful suburbs – delightful suburbs which were developed before urban planners were even invented and were constructed by people advancing their own interests, rather than pursuing some social engineering agenda…

MPs receive donations from property developers keen to maintain the scarcity of the product (land), which results in higher property prices. The MPs then publicly support urban planners who rail against the so-called evils of urban sprawl, none of which stands up to scrutiny. The resulting urban growth boundaries, which force people into high density housing developments in the inner suburbs, are a classic example of the Baptists and the Bootleggers phenomenon at work.

The problem is, it is young home buyers, hit with the spiralling costs of home ownership who end up paying…

One need only look at the scenes below to recognise that the detractors of urban sprawl have it wrong with respect to bio-diversity [in-fill on left vs “sprawl” on right]…

The wholesale adoption of urban consolidation policy by those in the planning and legislative fraternities led to a rash of planning regulation responses that further stifled supply. Urban growth boundaries, zoning restrictions and a host of other planning and building instruments became the order of the day as governments, shire councils and their planning operatives sought to throw a corset around the body of our cities.

This policy of urban consolidation dramatically slowed land supply at a time when the market was demanding it. As happens when the supply of any valued commodity is constricted, the price went up. The land rush was on and land prices increased by astounding multiples…

The first, and major, step in restoring housing affordability lies in governments stepping aside from the land management role and allowing the natural forces of supply and demand to return to the market. It is only as adequate supply returns to the market that land prices will fall. Urban growth boundaries must be removed and the abandonment of the insane notion of “x” years supply of land available. The home buying public will decide how many years’ supply of land there is, not the government. The removal of urban growth boundaries and other restraints on land use is equally important for landowners. These boundaries and planning restraints effectively ‘nationalise’ their land preventing those with land outside the boundaries from obtaining a fair value for it. It further inflates the value of land within the boundaries resulting in wasteful lobbying to have land rezoned. Corruption of public officials in dealing with zoning changes is not uncommon.

Another factor that contributed to land price hikes during this period years was the way “up-front” infrastructure costs, fees, taxes and charges were applied by state and local governments. In some capital cities, these charges added more than $100,000 to the price of a finished allotment. The question of infrastructure costs of growing cities – in particular who should pay for new infrastructure on the urban fringe is often raised. The answer is obvious – home buyers. But this is the wrong question. The question is not “who should pay?” but “when should they pay?”

Local government believes home buyers should pay ‘up front’ for the cost of their infrastructure. Others, like myself, believe home buyers should not have to pay for their infrastructure “before” they use it but should be allowed to pay for it “as” they use it as was the case in previous generations. It is simply not equitable to expect young homebuyers – those least able to afford it, to pay for the cost of infrastructure before they’ve used it when existing home owners who live in established suburbs (many of whom do not even have mortgages) were not asked to pay for their infrastructure before they used it but were able to pay for it “as they used it” through their rates. First home buyers on the urban fringe are now subsidizing, through their electricity, water, sewer and council rates, the massive repair and upgrading of existing, older infrastructure in the inner suburbs in order to accommodate wealthier ‘in- fill’ homebuyers.

Leaving aside the fact that infrastructure developed to accommodate 1,000 to 2,000 people per square kilometre simply cannot now withstand housing densities double that number, the cost of upgrading existing inner suburban infrastructure is significantly greater than the cost of providing brand new infrastructure on the urban fringe…

One of the more pernicious aspects of high land prices ie high mortgages, is the forced misallocation of capital and family income into mortgage payments instead of higher standards of living, assets, goods, travel, children’s education, appliances or even foregone income to spend more time at home…

In creating the conditions for home ownership to become the privilege of the few rather the rightful expectation of the many, state governments have produced intergenerational inequity and breached the moral contract between generations…

To fix the problem for good and ensure that future generations do not suffer the same fate we need to do five things:

1. Where they have been applied, urban growth boundaries or zoning restrictions on the urban fringes of our cities need to be removed. Residential development on the urban fringe needs to be made a “permitted use.” In other words, there should be no zoning restrictions in turning rural fringe land into residential land.

2. Small players need to be encouraged back into the market by abolishing compulsory ‘Master Planning.’ If large developers wish to initiate Master Planned Communities, that’s fine, but don’t make them compulsory.

3. Allow the development of basic serviced allotments ie water, sewer, electricity, stormwater, bitumen road, street lighting and street signage. Additional services and amenities (lakes, entrance walls, childcare centres, bike trails, etc can be optional extras if the developer wishes to provide them and the buyers are willing to pay for them).

4. Privatise planning approvals. Any qualified Town Planner should be able to certify that a development application complies with a Local Government’s Development Plan.

5. No up-front infrastructure charges. All services should be allowed to be paid for through the rates system ie pay ‘as’ you use, not ‘before’ you use.

Given the vast social and economic benefits that flow from homeownership, restoring housing affordability should once again become one of our nation’s most important priorities.

Regardless of whether you agree fully with Bob Day’s submission, it is reassuring to have someone entering parliament that genuinely cares about housing policy and the issue of housing affordability. I wish him well.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.