By Bullion Baron

A few years ago I wrote a post with a list of reasons that First Home Buyers (FHBs) might consider putting off a purchase, it included the following:

You may quickly outgrow your first home

One idea that I seem to hear repeated often is that you should just ‘buy whatever you can afford’ when it comes to your first home, just ‘get your foot in the door’ they say and work your way up the property ladder. What the older generations might be failing to remember is that you may outgrow your first home very quickly.

Imagine the situation where you’ve bought a 2 bedroom unit as your first home. Two years down the track and the casual relationship with your partner has taken a serious turn and you are looking to start a family (have kids). You may then be in a situation where you have to sell the existing property to fund the larger one. That likely means real estate commission costs (usually around 2% of sales price), stamp duty on the new home, possibly LMI (Lenders Mortgage Insurance) on the new loan if you will be borrowing on a LVR greater than 80% again. Not only that, but as per reason 1, you’ve possibly been paying a great deal more than renting to buy.

Do the sums. Make sure you consider all possibilities that arise. You may be a lot better off by renting until you can afford a home that will last years no matter what life throws at you.

The general consensus is that FHBs should purchase their first home as a stepping stone. Just buy what you can afford for your first home and the capital growth will get you into your next (long term) home is a common meme thrown around in the mainstream media and by those who have benefited from unsustainable price growth in the past.

The meme continues in this blog post from RP Data’s Cameron Kusher in which he uses his own personal example to show what is possible:

“Given this, the prospective first home buyer is, in most instances, going to have to make a sacrifice in order to enter into home ownership. As I see it, first home buyers need to make one of two major sacrifices; either move away from their local area to an area where home values are more affordable in order to enter the market or buy something which is at the lower end of the local market (which will often be a unit rather than a house). The strategy for someone buying their first home should rarely be to buy at the suburbs median selling price; it should be to buy an entry level property. Of course varying levels of deposit and income will dictate what the purchaser can reasonably afford to borrow and repay. Over time, the first home buyer should see some capital growth and it would also be reasonable to expect that they should also experience an improvement in their employment conditions (more pay/promotion/new role) which would eventually help in assisting them to upgrade.

Looking at my first home buying experience, the above scenario parallels my own experience. I have to admit, the home was pretty horrible but it was in the inner city location I wanted.

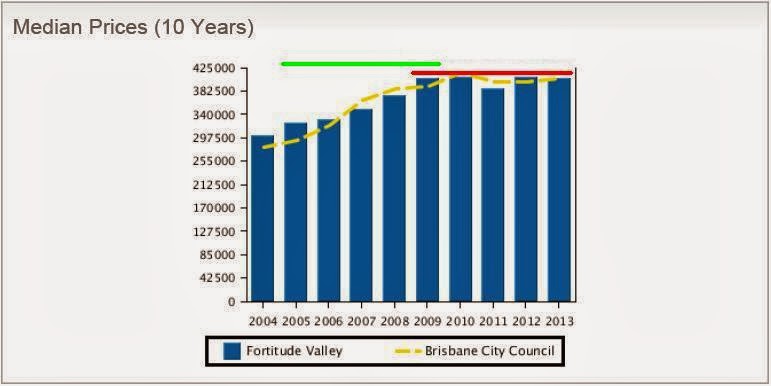

My first purchase was a two bedroom, one bathroom unit in Fortitude Valley in Brisbane. The location was great but the unit was not so great. The complex was largely utilised for short term accommodation and although the unit had two bedrooms and one bathroom, outside of those three rooms it had one further room which functioned as a kitchenette, lounge and dining room. I purchased the property for $248k in July 2005 and sold the property in April 2010 for $334k effectively five years later. At the time of purchase, the median unit price within the suburb was $309,240 and by the time of sale the median unit price in the suburb was $400,000.

The unit was purchased at a price well below the suburb median and upon sale the price had increased by 35%. In comparison the median sale price across Fortitude Valley had increased by a lower 29%. At the time I was single so I also had a friend come and live with me which assisted in making the mortgage repayments.

By the time I sold the property I had purchased a subsequent property which was a house, once again it was purchased at a price below the suburb’s median. I had managed to make a profit on the sale of my first home and purchased a more expensive property, I had also benefited from an increase in salary over the time which made repayments easier.”

In Cameron’s example his home increased 35% over a 5 year period, well exceeding median wage growth even if his own personal situation resulted in a stronger increase. Price growth can’t exceed wages forever, so of course there will be low (or negative) price growth periods while wages catch-up. For example the period following Cameron Kusher’s ownership in Fortitude Valley.

|

| RP Data Price Chart for Fortitude Valley Units – Click Image To Enlarge |

See above a 5 year period starting in 2005 has treated the owner to a strong period of growth, but a FHB starting in 2009 for a 5 year period is probably lucky to have broken even (on price alone) in the Fortitude Valley unit market, so from a financial perspective (once buying & selling costs are taken into account), they probably would have been better off renting and saving to buy a long term & more suitable home.

While renting is suitable and preferable in my situation, I would never discourage others who want the stability of ownership and are prepared to treat housing as a consumable (rather than an investment) from buying. If you have a healthy deposit (preferably one that will help you avoid LMI), fixed interest rate (or able to service higher interest rates), protect yourself (income protection, cash buffer, etc) and expect to stay in the property you purchase for the long term (until mortgage paid off), then it shouldn’t matter what prices do (rise, fall or stagnate).

Some people are happy to pay a premium for the stability and enjoyment they get from home ownership, perhaps down the track when starting a family my priorities will change and I will make the same decision. For now I will continue renting, it is far cheaper than the interest repayments would be for a mortgage if buying the equivalent, it provides more flexibility and there is a good chance that my housing requirements will change at some point in the next few years (so it’s pointless buying now if I will only be looking to upgrade in a few years).

When I queried Cameron on Twitter about his decision to purchase a first home with a short term view, he said:

“I purchased assuming I would get some capital growth, build some equity and my financial position would improve.”

The bottom line is that we shouldn’t be encouraging First Homer Buyers to speculate. They shouldn’t purchase a home with a 5 year view that they will see capital growth and be able to flip the home for a profit as a stepping stone to a more suitable house in the future.

Even if they see a little capital growth, it needs to exceed both the significant buying & selling costs along with the difference between the cost of renting vs buying to have been financially worthwhile doing so. They are the most vulnerable (financially) in the housing market, using high leverage and often have a poor understanding of financial products in general. We should be careful not to coerce them into taking unnecessary risks.