The ABC’s Michael Janda has written a solid article today questioning the common claim that Australian homes are at their most affordable level in a decade. From The Drum:

The most recent Housing Industry Association-Commonwealth Bank quarterly Housing Affordability Index for September showed times had not been better for buying a home since June 2002.

With home prices on the rise, deposits losing their relative value, and affordability at a decade high, surely it must be time to jump into the market?

So why then do the most recent ABS housing finance figures for November show first home buyers making up the smallest proportion of new mortgages on record? Why are new home buyers accounting for just 7.6 per cent of real estate purchases?…

The obvious question then is, how can housing simultaneously be … overvalued and the most affordable it has been in more than a decade?

The answer lies in what the HIA-CBA Housing Affordability Index measures, and how it measures it.

It compares the level of monthly mortgage repayments on a median-priced property purchased now with average weekly earnings. The index does so at current interest rates, which happen to now be sitting around record lows…

Over the life of a 25-year loan, it is pretty fair to assume that you will end up paying, on average, the average interest rate, not the lowest rates in decades as we have at the moment…

So, housing affordability over the life of a loan is likely to be pretty average at the moment, relative to very recent history…

What is certain is that Australian housing isn’t affordable unless you’re betting the house on rates staying at record lows for decades, and that’s a very risky financial move – just ask the now homeless honeymoon rate buyers in the US.

…housing affordability (i.e. the cost of the home relative to incomes) and mortgage serviceability (the immediate cost of servicing the loan) are not the same thing. The former has only improved modestly in recent years, whereas the latter has improved significantly thanks to the reduction in interest rates, which are unlikely to always remain so low. In this regard, the HIA’s index should really be labelled a “mortgage affordability index”, since it measures the current cost of obtaining a mortgage on a median priced home, not the structural cost of housing per se.

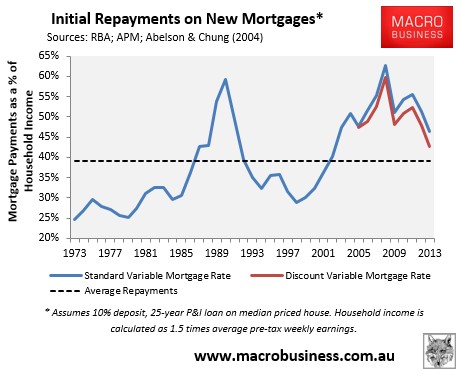

For what it’s worth, below is my own mortgage affordability index, with median house prices derived from Abelson & Chung (2004) and APM, variable mortgage rates from the RBA, and household income measured as 1.5 times average pre-tax weekly earnings. As you can see, mortgage affordability has certainly improved in recent times, although it remains below the long-term average.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.