In sadly his last article for The Age, Tim Colebatch has published a typically well-reasoned piece on why the Australian Government should fight to keep automotive manufacturing alive in Australia:

In 2011-12, the industry employed more than 45,000 people, and produced $5.4 billion of net output: $2.2 billion from making cars, and $3.2 billion from making parts and components. Its reach through the economy is huge, with thousands of suppliers…

Holden, like Qantas, is a victim of the high dollar. In 2002, the Australian dollar averaged 54 US cents. For businesses in the global market, such as car makers, Australia was almost as competitive as South Korea.

But by 2012, Australia’s dollar had risen 91 per cent, to average $US1.035. In global markets, that made it 91 per cent more expensive to produce goods and services here.

It is not the only reason the car industry is in trouble, but it is the main reason… Australia’s currency has risen more than that of any other developed country. Our economic culture allowed our currency to escalate so high as to make our producers uncompetitive, and neither the government nor the Reserve Bank did anything about it. An anonymous minister tells us the next generation of Holdens will be built in South Korea, and shipped here duty-free under the new free trade agreement. That makes sense: former Holden chief Mike Devereux told us a Commodore could be produced for $3750 less there than here. Korea takes manufacturing seriously...

While our dollar soared 91 per cent, the Koreans let the won edge up just 6 per cent. While Australia’s cost base more than doubled between 2002 and 2012, Korea’s cost base held its ground. Is it any wonder that by 2012, manufacturing production had almost doubled in Korea, yet was back to 2002 levels in Australia?

…while the case for pulling the plug on industry support after 2016 is compelling, I urge Abbott and Joe Hockey to think again. First, car programs cost $400 million a year, nothing like the $3 billion a year for diesel fuel rebates to mining companies, or the $5 billion to subsidise negative gearing. The budgetary cost of losing this industry will dwarf the cost of keeping it.

Second, if the car industry sinks along with mining investment, that will create huge risks for the economy…

Advertisement

As I keep saying, even if abandoning the car industry makes sense on allocative efficiency grounds, it makes absolutely no sense to do so as the once-in-a-century mining investment boom is unwinding – when there is already likely to be extreme pressure on growth and jobs. Moreover, to do so would unlikely to be supportive of the Federal Budget, which is likely to see the saving of $400 million annual subsidies more than offset by increased welfare payments to displaced workers and/or the need for additional economic stimulus.

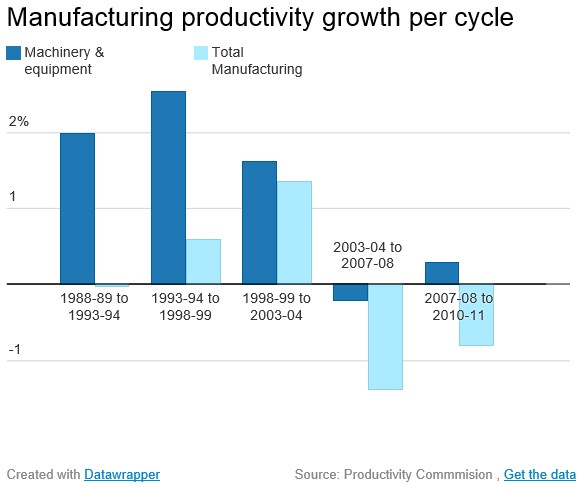

As argued by Greg Jericho (aka “Grogs Gamut”) yesterday, the automotive industry is also not the sloth that everyone assumes, with automotive productivity outperforming the rest of the manufacturing industry:

The productivity commission’s working paper on productivity in the manufacturing industry found that the machinery and equipment sub-section – a large part of which represents car manufacture – has continually outperformed the rest of the manufacturing industry over the past 25 years:

…None of this will be likely to save the car industry. That will in the end come down to General Motors maximising its global profits. But if it does go, it won’t be because of below par labour productivity. It will also be somewhat ironic for a government which places such store on improving productivity, that should the car industry depart under its watch, it will likely hurt the manufacturing industry’s overall productivity growth.

Advertisement

What the above suggests is that the demise of the Australian automotive sector is primarily because of the high Australian dollar, rather than inefficiency per se. It also suggests that shuttering automotive manufacturing could be a short-sighted move, particularly given the currency is likely to fall significantly in the years ahead.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.