John Kehoe of the AFR has a reassuring take on foreign debt holders of Australian housing today:

Henry Cooke, an investment manager at Threadneedle Asset Management in Britain, said the biggest local issue that it spent time analysing was whether Australia was in a housing bubble.

“That’s the sector everyone outside Australia wants to know about,” Mr Cooke said in Sydney on Monday.

“My concern is if you start to see a downturn in the economy . . . foreign investors start to get nervous.”

Francisco Paez, head of international structured finance at insurer Metlife, said a significant rise in unemployment would probably cause house prices to fall.

However, he did not envisage a repeat of the US crash where prices fell by between 20 and 30 per cent in most major cities after from around 2008.

…Mr Paez said the high house prices in Australia appeared to be driven chiefly by a lack of new supply.

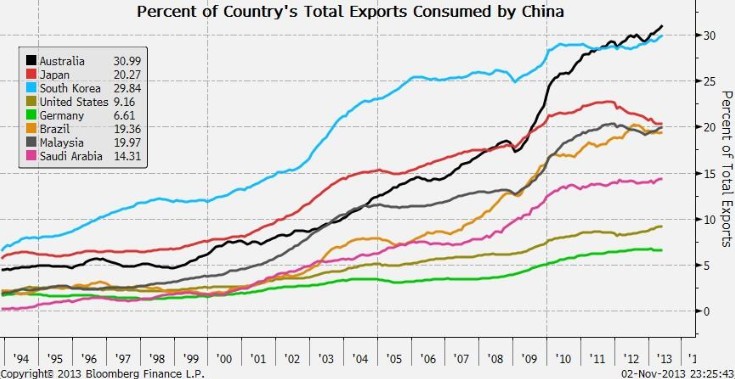

Just two points. China is the big risk so I hope these chaps spend more time looking at it than they do Australian RMBS. Australia’s exposure to China is now the largest of any country on earth:

Second, overvaluation based on apparent housing shortages should not reassure these gents. As UE has explained at length supply restricted markets are not a one way bet upwards. They are a one way bet to volatility:

…unresponsive housing supply results in greater house price volatility – both on the way up and the way down. Such a situation can be explained using basic supply and demand analysis, as shown in Figure 1.

Q0 and P0 represent the initial equilibrium situation in the housing market. Initial demand is provided by D0, whereas supply is shown as either SR (restricted) or SU (unrestricted), depending on whether land supply constraints exist.

Following an increase in demand, such as a surge of investors following changes to tax rules (e.g. Australia’s CGT reduction in 1999), the demand curve shifts outwards from D0 to D1. When land supply is restricted, house prices rise sharply from P0 to PR. By contrast, when supply is unrestricted, prices rise more gradually from P0to PU.

The situation works the same way in reverse. For example, if there was a sharp fall in demand following a contraction in credit availability or a sharp decrease in Australia’s Terms of Trade, causing demand to fall from D1 to D0, then prices fall much further when land supply is constrained.

In short it’s not the US that these chaps should be looking at, it’s the UK, with its similar planning system. And they should be asking themselves can a small, open and externally funded economy do what the UK has done to sustain the unsustainable if the rubber hits the road?